The 2024 3D Printing Macro Outlook: IDTechEx’s Senior Tech Analyst Sona Dadhania on the Complex Financial Environment

It can often seem like there’s very little upside to trying to make sense of the trajectory of the global business environment, especially in the 2020s. One of the biggest challenges involved lies in the simple fact that the macroeconomic conditions currently prevailing across the globe are themselves so difficult in every sense of the word.

They’re difficult to experience, difficult (and frequently, unpleasant) to observe and keep track of, and even if you work at keeping track of those conditions, they are — above all — difficult to come away from with a satisfying interpretation. In turn, this leads most to shy away from even trying to follow the emergence of a “big picture.”

When that happens, the difficulties involved tend to combine, and the overarching challenge becomes something of a self-fulfilling prophecy: since people begin to generally avoid all attempts to form views of the grand scheme of things, the exercise itself starts to seem entirely impossible, and counterproductive, and so forth. The problem with that is that no industry exists in a vacuum, and this is particularly true about any industry comprising the manufacturing sector.

Manufacturing is one of a handful of strategic sectors that is most responsible for shaping, as well as most shaped by, the global macroeconomic trajectory. Despite the inherent difficulties, then, if you can force yourself to diligently follow the daily unfolding of the global economic narrative, it can be an indispensable tool for additive manufacturing (AM) companies in planning their business operations.

With that in mind, I reached out to Sona Dadhania, senior technology analyst at consultancy IDTechEx, and asked her to help me make sense of some of the trickiest areas of the additive manufacturing (AM) industry to get a handle on: the state of mergers & acquisitions (M&As) and the prospect for inflow of investment dollars into the industry. As you can see from her responses, the seemingly chaotic nature of those issues in 2023 becomes much clearer when contextualized within the economy at-large:

“In the broader economy, M&As have dropped as economic uncertainty related to inflation and interest rates has fueled more caution in deal-making. Additionally, financing for potential buyers has become more difficult and expensive to access. It is unlikely for M&As, both in other industries and in the AM industry, to pick back up again until this economic uncertainty resolves to some extent. In the meantime, the deals that we do see will need to emphasize strategic value and growth opportunities to make them worth pursuing in such macroeconomic conditions.”

Along those lines, it is perhaps unsurprising that the largest AM financing rounds in 2023 went to companies whose operations revolve around advanced manufacturing techniques including AM, but otherwise function like contract manufacturers rather than as original equipment manufacturers (OEMs). AM industry stakeholders are clearly being cautious in general about investments that they still view as too risky.

Nonetheless, the investments those stakeholders are still making seem driven by an overall effort towards supply chain stabilization, a motivation also driven by the economic uncertainty related to persistent inflation, high interest rates, etc.:

“The vast majority of companies that received the biggest funding rounds in 2023 do not adhere to the traditional 3D printer OEM business model, where a company sells printers with their proprietary printing technology to end users,” Dadhania noted. “Instead, three of the biggest funding rounds in 2023 were awarded to companies that are fundamentally end-users themselves: Divergent Technologies, Lightforce Orthodontics, and Zeda. While each of them undoubtedly possesses their own intellectual property and innovations supporting their business, none are primarily focused on pioneering new or incremental innovations in 3D printing technology. Rather, their focus is on using AM to address specific verticals: automotive, dental, and aerospace/medicine, respectively. This indicates a broader shift in the industry towards focusing more on applications rather than on 3D printers. It also signifies a change in investor focus, who, in a more cautious macroeconomic environment, are less inclined to invest in just any new technology; they are seeking to invest more in startups with a clear path to revenue generation and profitability. AM startups concentrated on using AM to provide specific products to particular verticals are likely more attractive for financing from this perspective.”

Thus, even in cases where investors are taking a risk on new technologies, it is notable that, again, those technologies tend to form the basis for manufacturing service providers rather than a basis for selling 3D printers:

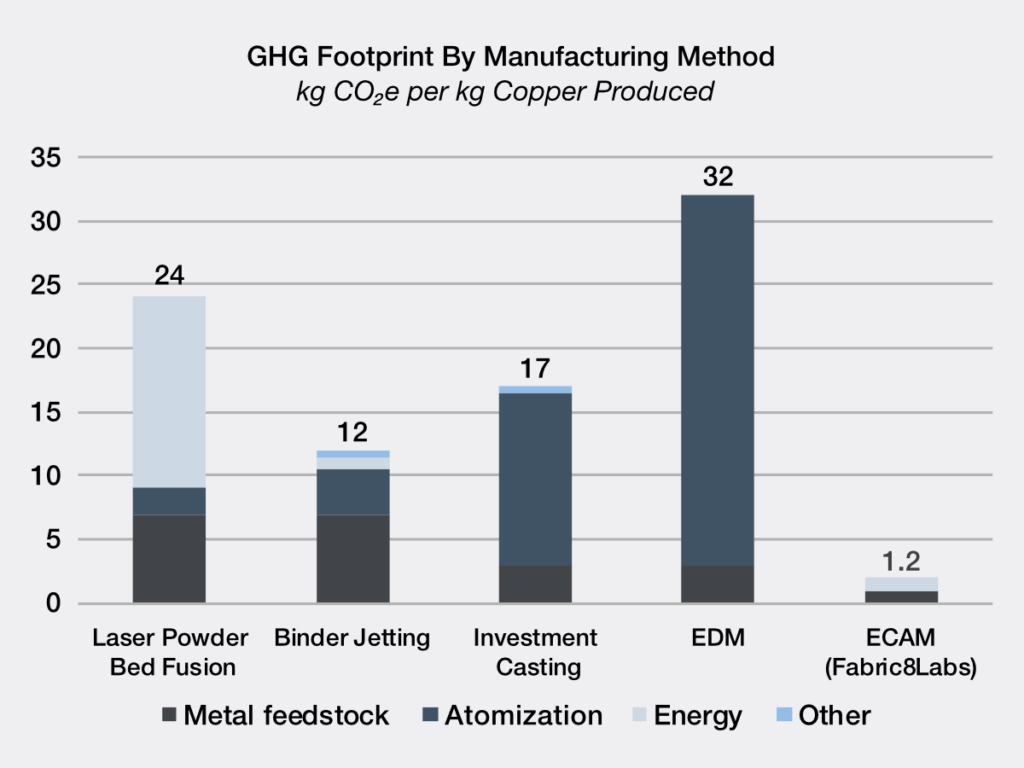

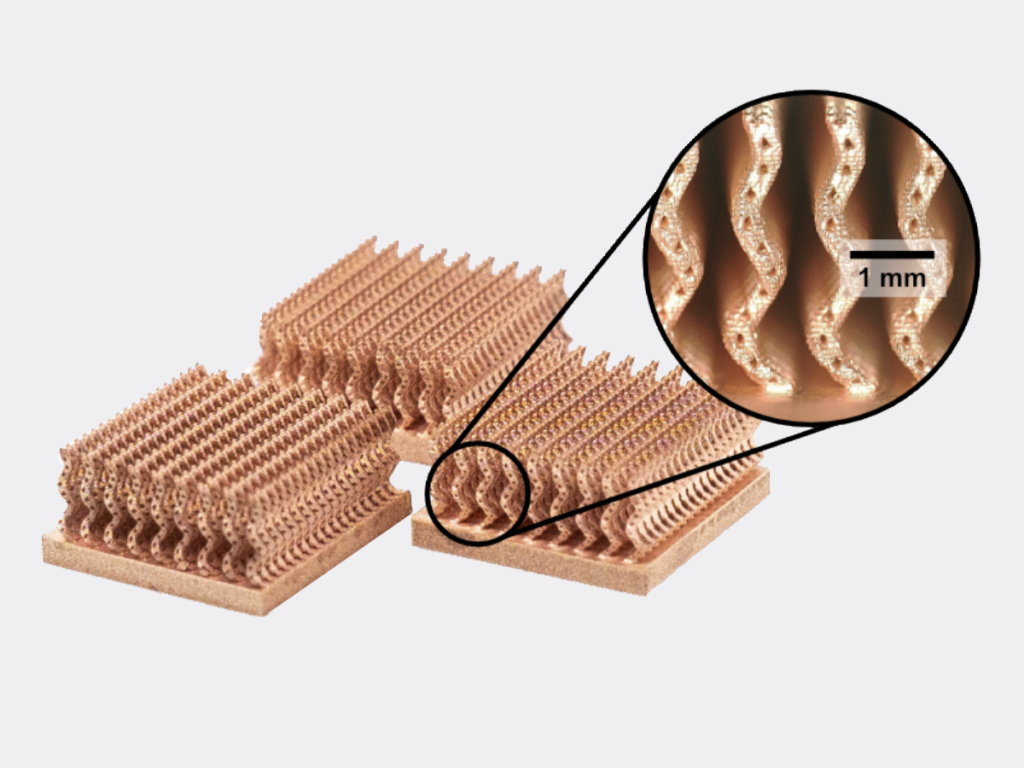

“That said,” Dadhania added, “it’s not that new AM technologies are not receiving large funding rounds. In 2023, two of the top five biggest funding rounds went to companies developing new print technologies: Seurat Technologies and Fabric8Labs, both specializing in metal 3D printing. However, what’s notable is that neither of these companies are following the traditional printer OEM business model. Instead of selling printers equipped with their metal 3D printing technology, both are planning to use them in their own manufacturing facilities to produce final parts for customers. The major benefit of this business model is that it removes the capital and operational expenses required for customers to invest in new manufacturing technologies, theoretically lowering the barrier to adoption. Investors likely find this model attractive for the same reasons mentioned earlier, which is that such a business model may offer a quicker, clearer path to revenue generation and profitability compared to traditional printer OEMs.”

Even though the most-watched hypothetical M&A deals from 2023 didn’t pan out, the expectation remains that M&As will inevitably pick back up. And, in November 2023, two significant purchases did go through: Nexa3D acquired Essentium, and BigRep acquired HAGE3D. (Shortly after the latter was announced, BigRep announced a SPAC deal to go public on the Frankfurt Stock Exchange.)

The nature of the successful mergers may confirm, to some extent, the validity of something you’ll hear frequently from AM industry insiders, which is that the market is simply “too fragmented.” Dadhania shed light on this as well, pointing out that while it’s certainly true about the OEM space, M&As aren’t the only way that problem will be sorted out:

“While there are genuinely many unique printing technologies, each with their own applications base, there are hundreds, potentially thousands of printer OEMs in the AM industry. Many of these printer OEMs do not have significant, tangible differences that distinguish them from the 100s-1000s of competitors in 3D printing. So, when I hear people express that the industry is “too fragmented”, I think they’re referencing this surplus of OEMs who may often lack key differentiating factors from their competitors. From an end-user perspective, this likely presents a lot of confusion — for example, how does one decide between the 50+ companies offering laser powder bed fusion printers?

To reduce the confusion for new adopters and to lower the barrier of entry to AM, it would likely be beneficial for the industry have fewer OEMs with so much overlap. However, M&As are not the only route to achieving that. Given the money required to keep a manufacturing equipment business afloat, it would not be surprising for many printer OEMs to simply not find enough business to keep their doors open. That will naturally happen as the industry matures, which will steadily reduce its fragmentation. Still, M&As that maximize synergies between companies will be an important aspect of reducing fragmentation in the industry.”

The other factors that should help determine the way the hardware market consolidates lie in the growth trajectories of all the areas of the industry aside from hardware. In other words, the more that materials portfolios and software platforms standardize, the clearer it will become, which machines are most compatible with the feedstock and software markets in their more mature state. Dadhania concluded by emphasizing that effective analysis of the dynamics of the AM industry will, more and more, depend on giving equal focus to each segment of the overall industry:

“There’s no doubt that materials will play an increasingly central role in driving the AM market; in fact, IDTechEx predicts that the revenue generated from materials sales will surpass that of printer sales within this decade. This is as users find applications that increase their printer utilization and, subsequently, material consumption. Many surveys have also indicated that a small or unsuitable materials portfolio is a key barrier to adoption in AM. Therefore, there is definitely room for innovation and expansion in this area to fuel AM’s growth. Software will also act as an important driver, as the right software can lower the barrier to adoption for end-users and enable them to maximize the potential and productivity of AM.”

And, to reiterate a final time, how critical it is to keep track of the big picture, the dynamics of the materials and software markets can be expected to be particularly affected by the macro outlook. Public policy issues related to international markets for critical minerals are already directly impacting the shape of the metal powders space, and AI and cybersecurity will continue to center the focus of firms on the software side of the AM industry.

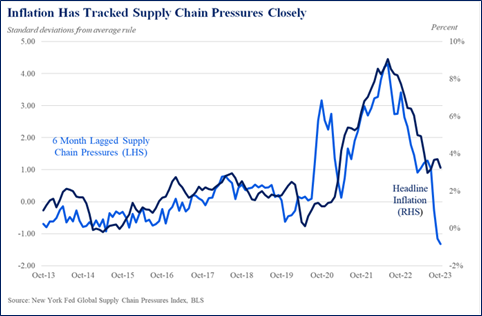

So, pay attention to all business news, not just AM news; pay attention to what the Fed is doing, pay attention to supply chains. It’s overwhelming, but if you can wrap your head around microstructures and lasers and rocket engines, you can understand the global business environment — even in the 2020s.

Featured image courtesy of IDTechEX

Subscribe to Our Email Newsletter

Stay up-to-date on all the latest news from the 3D printing industry and receive information and offers from third party vendors.

Print Services

Upload your 3D Models and get them printed quickly and efficiently.

You May Also Like

Australia’s AMCRC Funds Titanium 3D Printing R&D

In terms of the global economy’s presently existing state, there is no realistic path to economic resilience that doesn’t start with critical minerals security. This is a problem for pretty...

3DPOD 305: Automating AM with Grenzebach’s Oliver Elbert

Oliver Elbert‘s over ten years in additive manufacturing have been spent automating LPBF. For large, high-volume, or critical parts, Grenzebach has provided custom automation solutions. Depowdering, powder handling, sieving, heat...

AMPulse Asia: Chinese IPOs, Defense Deals, and Dental 3D Printing Lead APAC Roundup

The second half of June brought a wave of additive manufacturing activity across China, Japan, South Korea, India, and Australia. From Chinese IPOs and funding rounds to defense, aerospace, construction,...

Austal, Curtin University and AMCRC Work on R&D Together

Australia’s Additive Manufacturing Cooperative Research Centre (AMCRC) works with 70 industry partners to deliver collaborative R&D projects. They also work on workforce development and technology transfer. It’s kind of analogous...