Dream Mergers and Acquisitions: Who Merges Next in 3D Printing?

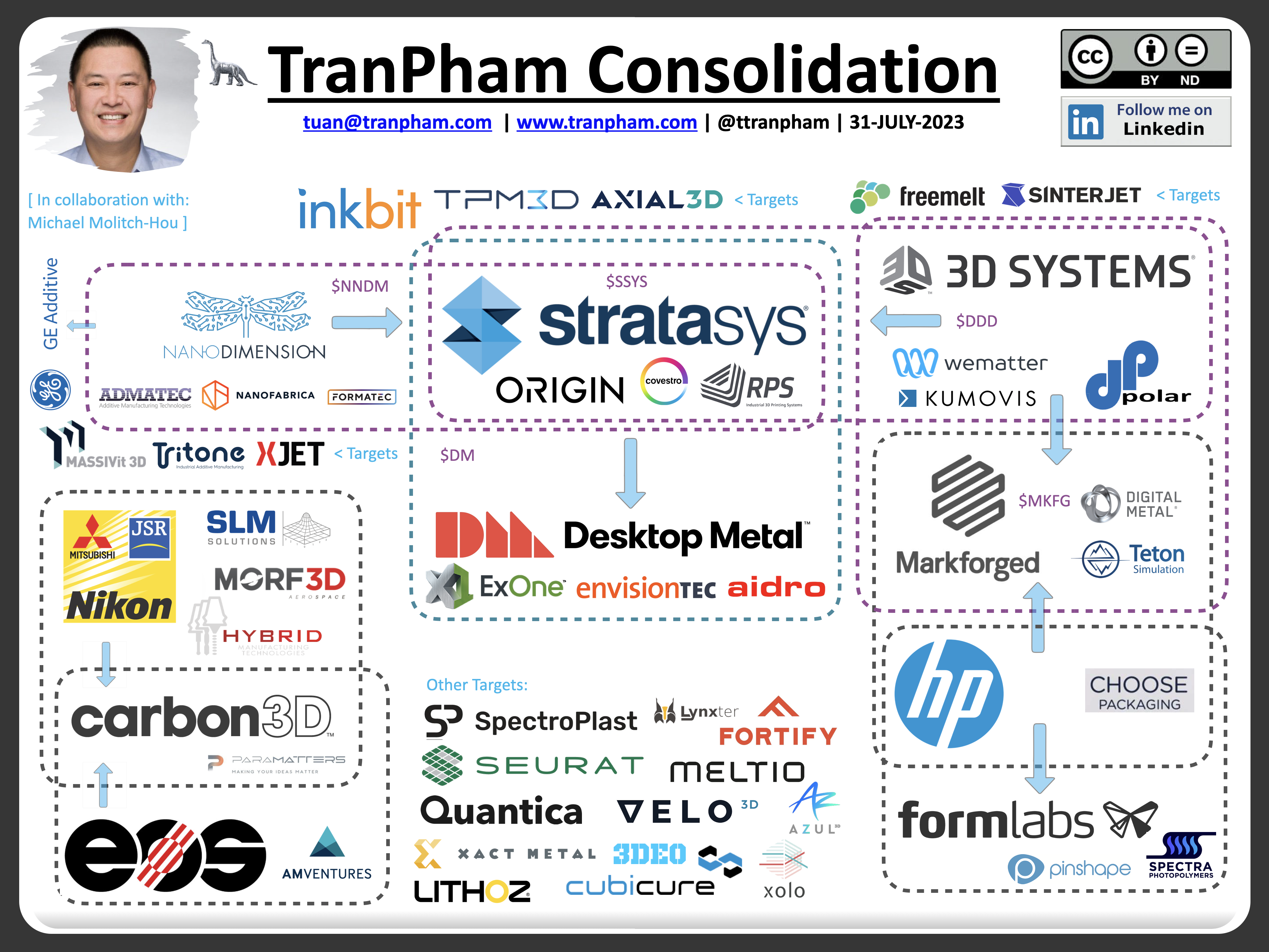

3D printing stalwart Stratasys (Nasdaq: SSYS) signaled the next stage of consolidation in the additive manufacturing (AM) market when it announced its intention to acquire newcomer Desktop Metal (NYSE: DM). Since then, it has entered talks with 3D Systems (NYSE: DDD) to determine if a signed offer from its long-time competitor fits the definition of a “superior proposal,” as outlined in its deal with Desktop.

At the same time, Nano Dimension (Nasdaq: NNDM) has over $1.2 billion in cash and 14.1 percent of Stratasys shares with which to wield influence. Nano previously expressed interest in possibly combining with Stratasys and 3D Systems, yielding the possibility that all four firms could merge. However, in its most recent press release, Nano instead said that it would likely sell all of its shares in Stratasys and pursue other acquisition targets.

Depending on what happens, there are a number of possible scenarios that could emerge. Working together, 3D printing’s most followed professional on LinkedIn, Tuan TranPham and 3DPrint.com Editor-in-Chief Michael Molitch-Hou outlined what they envision may take place.

Markforged

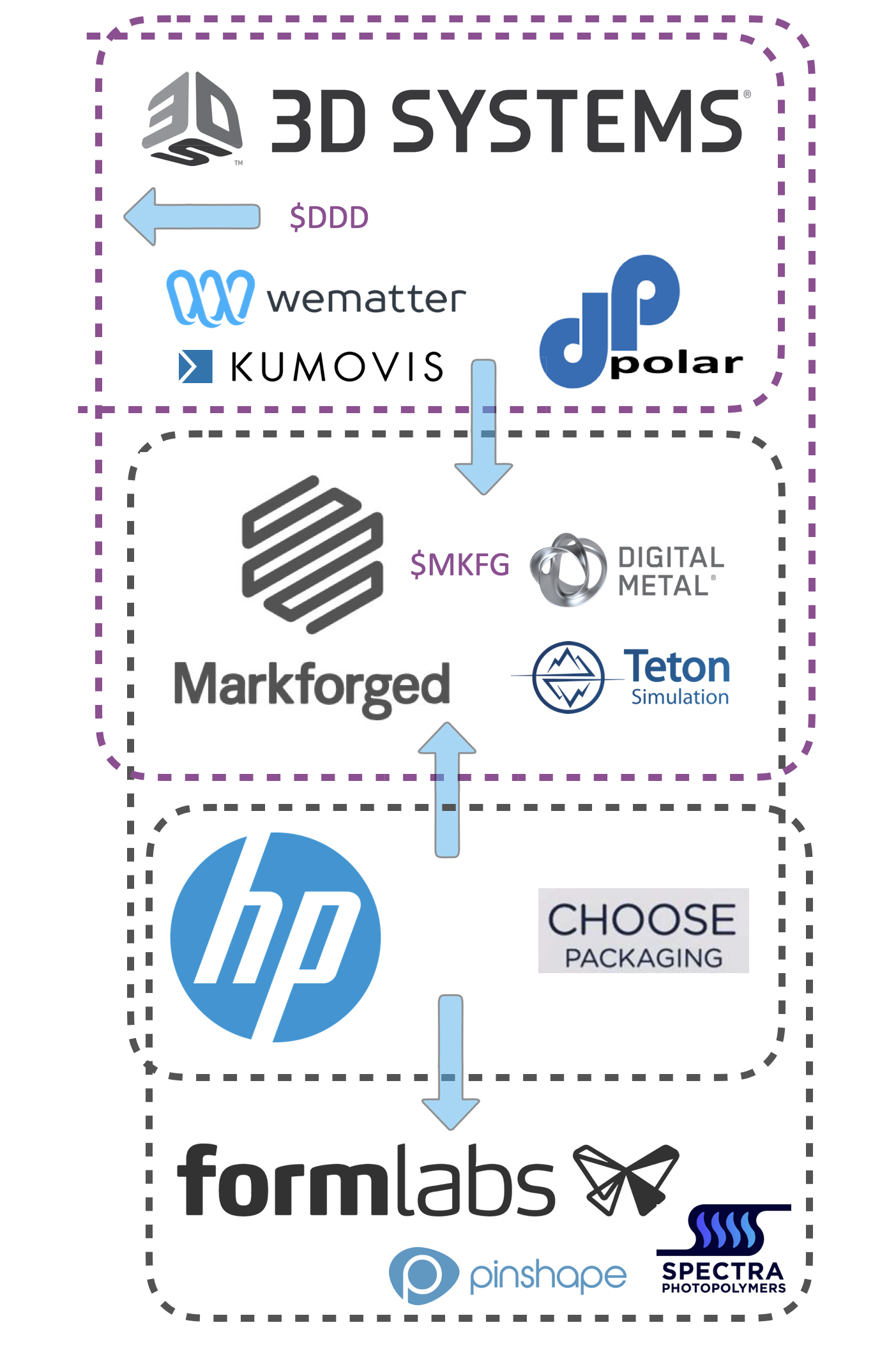

If all four companies already in talks were to merge, the market would likely need a counterbalance to the resulting entity in order to propel forward. There are plenty of options there. The first that comes to mind is Markforged (NYSE: MKFG), which was able to instantly capture about 15 percent of the metal binder jetting market (according to the Data Services from SmarTech Analysis) with the acquisition of Sweden’s Digital Metal. With the addition of its flagship composite 3D printing technology and low-cost bound metal extrusion, the company offers a strong portfolio.

Despite facing share prices that almost drove it off of the NYSE, Markforged stock recently experienced a high of $2.10 when it was promoted by ARK Investment Management Founder Cathie Wood alongside Rocket Lab. Wood similarly boosted Nano Dimension before a large sell-off that triggered a buy-in by activist investors and the current merger activity surrounding Stratasys. If ARK follows a similar pattern and pull out of Markforged later on, other investors could be left holding the bag in a quarter or two, leaving management in a precarious position. In turn, it might sell to a larger company.

Who that company could be is likely dependent on what happens with the Stratasys negotiations. If Desktop and Stratasys do merge, it will likely be necessary for 3D Systems to purchase a firm like Markforged to stay competitive with its long-time rival. If, instead, all or many of the players in that negotiation merge, a different party will have the opportunity to scoop up what is a potentially valuable commodity, even if it isn’t profitable at the moment.

One possibly interested party is HP, which offers binder jetting for polymers and metals. If the HP “mothership” has the faith in seeing through its long-term investment into AM, it could build a very hearty division by adding Markforged. HP has already established itself as a leader in 3D printing through the widespread adoption of its high-throughput Multi Jet Fusion technology for polymers.

Formlabs

HP leap frogged other polymer PBF companies nearly instantly, but to compete on other fronts, it could also add a name brand like Formlabs. This pioneer of low-cost vat photopolymerization has proven itself to be a strong, independent company capable of in-house development of numerous powerful machines and materials. However, it is Formlabs’ independence that makes an acquisition unlikely.

Carbon

Alternatively, HP could acquire Carbon, which has remained stagnant for some time, despite proving itself with Adidas and other consumer goods manufacturers. This may be, in part, due to the small build size of its machines and the limited variety of materials that can be printed with the company’s technology. HP and Carbon share a materials partner in German chemical giant BASF, so there is some synergy there.

Alternatively, HP could acquire Carbon, which has remained stagnant for some time, despite proving itself with Adidas and other consumer goods manufacturers. This may be, in part, due to the small build size of its machines and the limited variety of materials that can be printed with the company’s technology. HP and Carbon share a materials partner in German chemical giant BASF, so there is some synergy there.

However, another potentially more likely candidate would be Nikon (TYO: 7731), the independent Mitsubishi company that recently acquired metal 3D printer manufacturer SLM Solutions, after buying advanced 3D printing bureau Morf3D. This was followed by investments in Optisys and Hybrid Manufacturing Technologies.

The groundwork for such a purchase may have been laid bare earlier this year, when JSR Corporation, a Mitsubishi-owned materials company, ended its business operations with Carbon. JSR had invested in Carbon alongside Nikon, GE, and BMW in 2016, with a goal of 3D printing microelectronics.

With JSR out of the way to eliminate conflict of interest and a newly created U.S. headquarters for advanced manufacturing, Nikon may be in a good position to purchase Carbon and breathe new life into the company.

Alternatively, German 3D printing leader EOS could do so. What often isn’t discussed is just how powerful and rich the laser powder bed fusion (LPBF) leader is. Through AM Ventures, a venture capital portfolio launched by, but independent of, EOS, the company has access to numerous innovative technologies. While this includes adjacent technologies, including ceramic and metal vat photopolymerization, EOS lacks a pure digital light processing (DLP) tech, which Carbon could provide.

EOS is not known for making many purchases and it does have some purported distance from the AM Ventures portfolio, but the current wave of market consolidation could push it to make a big move. For its part, Carbon has not been able to establish the European traction it has craved and an acquisition by EOS would give it the foothold it needs to penetrate that market.

Further Acquisitions

As the economy recovers and investment in 3D printing stocks increases, consolidation will likely ramp up. Depending on how mergeracolpyse plays out, the parties involved may or may not need to augment their portfolios to continue competing against the resulting entity or entities. 3D Systems, for instance, could purchase Freemelt as a means of adding electron beam melting to its metal 3D printing line-up. Meanwhile, the acquisition of a firm like Sinterjet would bring low-cost metal binder jetting into its portfolio.

Stratasys could also continue to build on its increasingly large set of offerings with the acquisition of Inkbit, of whom it was an early investor. Inkbit would mean that Stratasys could build out a more intelligent and functional array of inkjetting technologies. Another firm it partnered with is TPM3D, a manufacturer of polymer PBF machines. There’s also Axial3D, which recently teamed with Stratasys and Ricoh to incorporate its technology for processing CT files to create 3D printable medical models.

We’ll also definitely see some action from Nano Dimension, which has more than $1 billion with which to make some acquisitions. Notably, it needs to bring in revenue, as it did with several of its previous purchases. As an Israeli company, it may make the most sense for it to buy firms within its national borders. For these reasons, it might look to large-format 3D printing firm Massivit3D, sintered metal 3D printer manufacturer Tritone, and metal and ceramic inkjetting company XJet. While Tritone is comparatively new, XJet is in the process of considering an IPO. If history repeats itself in the manner of the proposed Objet IPO a decade ago, XJet might instead consider a merger, as Objet did with Stratasys.

Perhaps the most interesting play we theorized was the acquisition of GE Additive by Nano Dimension. Right now, GE stock nearly doubled from a year ago, as it splits into three separate corporations. It uses AM across all three of these businesses, but its 3D printer manufacturing, under GE Additive, occurs within GE Aerospace. This is a potentially powerful unit, making laser and electron beam powder bed fusion machines under Concept Laser and Arcam, respectively, as well as a home-grown, large format metal binder jet system.

However, GE’s interests with AM lay mostly with servicing its own aerospace production operations, namely making fuel nozzles and turbine blades. As a result, GE Additive may not be flourishing as much as it could if it pursued other applications outside of the parent company. With Nano Dimension rebounding from a failed takeover of Stratasys, it could look to buy something just as prestigious, if not more so. Bought for $1 billion, GE Additive would instantly convert Nano Dimension into a 3D printing powerhouse.

Given that most of its customers are in defense already, Nano Dimension would be able to further penetrate this market with its new fleet of GE metal AM technologies. At the same time, though, it may need to sign a complex agreement with GE not to supply its competitors, such as Rolls-Royce and Pratt-Whitney.

Grab-bag Purchases

While Fortify has primarily focused on 3D printed dialectic electronics components and tools for injection molding, its DLP technology could prove valuable as a standalone vat photopolymerization offering. Because it has received investments from Lockheed Martin, Raytheon, and In-Q-Tel, it seems to be important to the military and intelligence industries, likely for 3D printing antennas and related items. The separate investments by Lockheed and Raytheon might mean that it can’t be bought by either one of them to bring production in house.

In contrast, Velo3D might be purchased by its leading customer, SpaceX, to be brought in-house. Other possible acquisition targets include Meltio, for its affordable directed energy deposition; Spectroplast, for its unique silicone 3D printing; Quantica, which manufactures inkjet printheads; Xolo, a developer of volumetric 3D printers; and Xact Metal, which makes low-cost metal PBF machines.

Exactly what happens next, however, is not set in stone. Whether or not any of the plays suggested actually occur is another story altogether. We will be happy if we get even one of these projections right.

Subscribe to Our Email Newsletter

Stay up-to-date on all the latest news from the 3D printing industry and receive information and offers from third party vendors.

Print Services

Upload your 3D Models and get them printed quickly and efficiently.

You May Also Like

Asia AM Watch: China’s 5 Million-Printer Export Year Signals Desktop AM at Scale

For years, a lot of the discussion around China and additive manufacturing has focused on industrial competition. Can Chinese companies move into higher-end markets? Can they challenge Western machine makers...

Creality Launches Filament Maker M1 & Shredder R1, Letting Makers Reuse Waste, Cut Costs, and Create Their Own Filament

From Printing Objects to Shaping Materials Desktop 3D printing has made on-demand creation more accessible than ever. Yet one critical part of the process remains fixed: the material itself. Most...

Bambu Lab 3D Prints Miniature Playground City for Kids in China

Bambu Lab has partnered with meland to open what they describe as China’s first 3D printing creativity center for children. The new space, officially named “meland x Bambu Lab,” launched...

Bambu Lab Says 2025 Was a Breakout Year: 10 Million Monthly Users and Real Business Growth

Chinese 3D printer maker Bambu Lab reported strong results for 2025, showing that the company’s push into community and small-business 3D printing is working. The numbers suggest consumer 3D printing...