Over 20B Aerospace Parts to Be 3D Printed by 2030 – AM Data Slice

“AM Data Slice” from Additive Manufacturing Research (“AMR”, formerly SmarTech Analysis) is a weekly segment that offers readers a dive into the additive manufacturing (AM) landscape, showcasing pivotal statistics and trends derived from AMR’s exhaustive research. In our most recent chart, we can see a significant growth trend in the production of 3D printed aerospace components from 2014 to 2030.

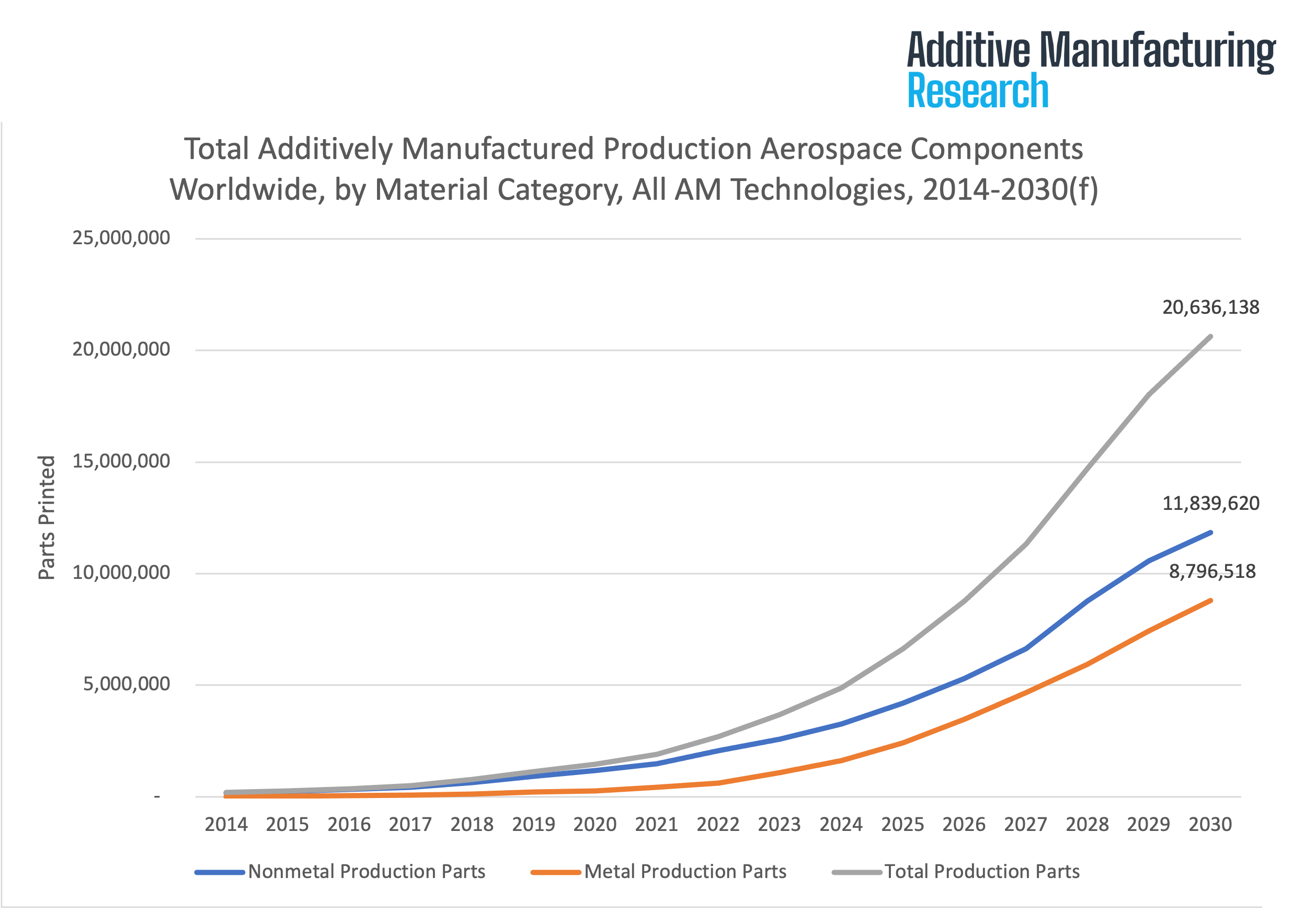

Nonmetal production parts have been the backbone of the additive manufacturing revolution in aerospace, with a forecasted increase from 181,168 parts in 2014 to a staggering 11,839,620 by 2030. As explosive as this growth would be, it also wouldn’t be entirely surprising given the materials that have expanded the applications of 3D printing in aerospace, making them a staple in the production line.

Most notably, PEKK-related thermoplastics have grown from a niche AM material from a single 3D printing company, Stratasys, to one offered by a plethora of next-generation material extrusion firms, including Roboze, Intamsys, and 3DXTECH, among others. Offering impressive strength, durability, and resistance to heat and chemicals, PEEK 3D printed parts offer cost reductions and quicker production times, which can be crucial in the highly competitive aerospace industry.

However, as the sector continues to grow, metal production parts display an even more dramatic surge. Starting at 17,766 parts in 2014, the forecast suggests an exponential rise to 8,796,518 by 2030. The significant uptick is attributable to advancements in metal 3D printing technologies, which are increasingly capable of producing high-strength, durable components that meet the stringent safety standards of the aerospace sector.

In total, the combined production of metal and nonmetal additive parts is projected to reach a staggering 20,636,138 by the end of the forecast period. This growth signifies a paradigm shift in aerospace manufacturing, moving away from traditional subtractive methods toward a future where digital designs and additive processes dominate.

Whereas key drivers for the adoption of AM in the earlier years were dedicated to speed and cost of traditional compared to additive production, there is an even more profound sea change taking place in the sector related to supply chain resilience. Now that supply chain weaknesses have been exposed by global events like the COVID-19 pandemic and military conflict, national governments and international corporations have dictated a fast march toward reshoring and digitization, detailed in the recent AMR report, “Additive Manufacturing for Military and Defense: Market Analysis and Forecast.”

Subscribe to Our Email Newsletter

Stay up-to-date on all the latest news from the 3D printing industry and receive information and offers from third party vendors.

Print Services

Upload your 3D Models and get them printed quickly and efficiently.

You May Also Like

The Seminal Moment: Creality’s IPO Analysis & Possible Effects

Something super important happened just a few days ago, and too few people paid attention. Creality, a pioneer in low-cost desktop material extrusion printers, went public. Creality is now listed...

As Longevity Gains Momentum, Rem3dy Health Raises £14 Million for 3D Printed Nutrition

Longevity hack or healthcare trend? The answer may depend on who you ask, but investor interest in personalized nutrition is growing as consumers search for the next longevity hack. Now,...

3Dnatives to Present ADDITIV Metals 2026: Resolving Key Barriers to Scaling Metal Additive Manufacturing

As the metal additive manufacturing sector prepares for a massive leap—with market valuations expected to climb from $6.02 billion to $7.02 billion this year—the industry is shifting its focus from...

Stratasys Dental’s Negar Movahed Says They’re “Open for Partnerships”

According to “3D Printing for Dentistry 2025: Market Study and Forecast” by AM Research, the dental 3D printing market generated $5.2 billion in revenue in 2024—that’s nearly one third of...