AM Investment Strategies 2023: Industry Leaders Discuss Growth, Consolidation, and Future of 3D Printing

A week ahead of Formnext 2023, Additive Manufacturing Research (AMR, formerly SmarTech Analysis) hosted another enlightening AM Investment Strategies roundtable, this time in association with Cantor Fitzgerald. Moderated by Troy Jensen, Managing Director at Cantor Fitzgerald, the event provided a sweeping view of the 3D printing industry’s current state and future prospects, with participation from Yoav Zeif, CEO of Stratasys (Nasdaq: SSYS); Jeff Graves, President and CEO of 3D Systems (NYSE: DDD); Arno Held, Managing Partner at AM Ventures; Scott Dunham, Executive Vice President of Research at AMR; and Max Lobovsky, CEO of Formlabs.

The show kicked off with an introduction by Vice President of Formnext Sascha Wenzler, who highlighted the rapid progress in additive manufacturing (AM), underscoring its profound influence on the automotive, medical, aerospace, and mechanical engineering domains. He also pointed out the lucrative investment opportunities it presents, along with its potential to radically transform traditional manufacturing by boosting efficiency and enabling intricate designs across diverse fields.

The Macroeconomic Situation

Once Jensen launched into the panel itself, much of the discussion focused on the state of the industry. Despite continued rapid growth, the 3D printing sector now finds itself in a slump, thanks to the macroeconomic environment. At the same time, consolidation is taking hold, with a potential merger of several candidates with AM stalwart Stratasys occupying much of the industry’s attention over the past year. The panelists were able to address much of these issues with key insights.

Yoav Zeif delineated the resilience of the industry despite low stocks, while Jeff Graves remained sanguine about the industry’s trajectory, particularly in the medical device sector, as AM continues to establish its footing in production facilities globally. Max Lobovsky stressed the criticality of making potent 3D printing technologies accessible and affordable to a wider user base to foster market growth.

“The industry is strong, but the stocks are low,” Zeif told the panel. “The nice thing is that we are on the other side of overshooting. We’re not in IPO-2014 [era]. We’re not in the hype of the SPAC [era], but it’s kind of a floor, because of the macroenvironment and long-lasting promises in the capital market. It’s a good place to be.”

Arno Held underscored the importance of not only introducing new technological principles but also stabilizing the technology and ameliorating the quality output of these machines to cater to the burgeoning production volumes, particularly in electro mobility and cleantech applications. He urged the industry to focus on delivering tangible value by evolving 3D printing into a bona fide manufacturing technology.

3D Printing Market Data

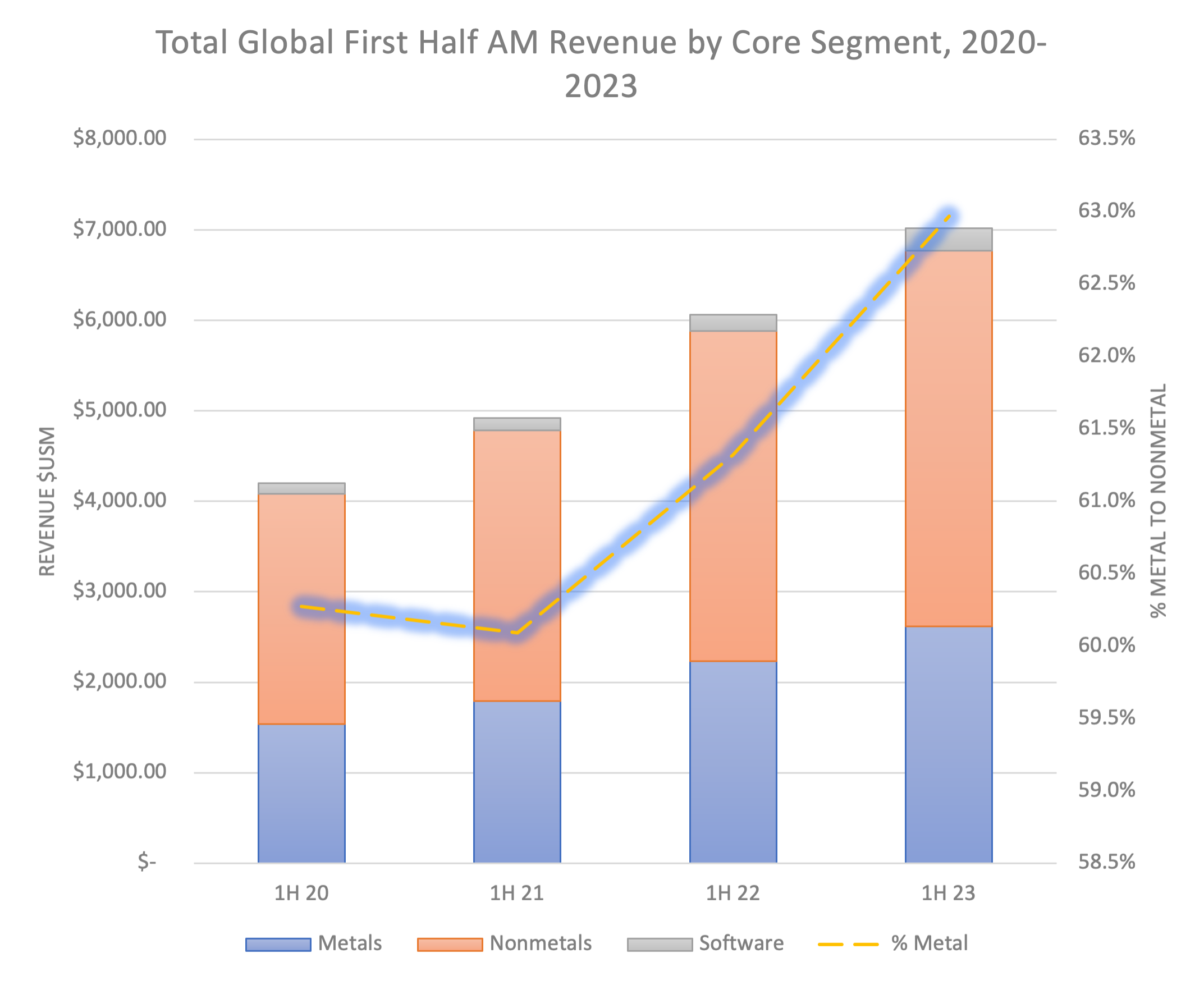

Scott Dunham delved into market trends and shared data on the growth in hardware, materials, and print services sectors in Q2. He acknowledged the hurdles posed by the current macroeconomic landscape but remained optimistic about the industry’s long-term outlook. He also noted the potential rise in solutions from companies developing high-quality yet cost-effective solutions as a trend for the upcoming 12 to 18 months.

“Established service bureaus probably will benefit [from decreased capital expenditure from manufacturers], but it might be challenging for relatively newer service bureaus. We do expect some increase in the activity of service bureaus because companies are unwilling to accept the current financial terms for getting new equipment in house—or maybe it’s just not viable for them and they want to move to a service bureau instead,” said Dunham. “This may be better for Materialize, Stratasys Direct Manufacturing, and those types of companies where they have more capital equipment that’s probably amortized now and can run more profitably and try to deflect some of the the overall price increases that we’re going to see due to inflation. Whereas, for new service bureaus, it might be more challenging if they need to add equipment to account for influx of growth… I think overall the outlook [for service bureaus] is good, but it’s not perfect for everybody.”

The discussion then transitioned to the remarkable 23% YoY growth in materials in Q2, with a notable contribution from the metal powder sector. Held emphasized the pivotal role of materials in unlocking new applications and verticals in 3D printing. He also highlighted the investment potential in privately-held material and polymer powder companies, marking materials as a fundamental element in advancing the 3D printing industry.

3D Printing Industry consolidation

Given that both Zeif and Graves were in attendance and 3D Systems had made multiple attempts to merge with Stratasys, the topic on everyone’s minds was consolidation. Zeif emphasized that consolidation is essential to cope with delayed adoption rates and to attain scale. Scale, he explained, would help companies to leverage infrastructure across all expense items and enable synergy across different technologies, given the diverse customer needs in additive manufacturing. Graves echoed the necessity for consolidation as the industry evolves towards more sophisticated customer needs in production environments.

“There’s a real need and a real opportunity for consolidation in our industry. Several things have changed that are really pulling on that. As customers move more to factory environments, production environments, their needs are more sophisticated, including their needs for sales support and upfront application support as they expand their usage of 3D printing and services. So, it does put a lot of strain on those parts of the business,” Graves said. “Then, from an R&D standpoint, customers increasingly want, a range of applications addressed. Often, that needs to come from different hardware platforms, certainly different materials, sometimes different software suites. As you expand with a customer, you need to bring to bear a broader range of technologies, which drives your R&D expense. As the industry matures now, and it’s ready for adoption, there’s a need for greater offerings, greater presence with your customers, and all of that drives costs. And, certainly, scale brings a lot more efficiencies to that whole ballgame.”

3D Systems acquired dp polar, which developed a unique system for large batch 3D printing. Image courtesy of dp polar.

3D Systems acquired dp polar, which developed a unique system for large batch 3D printing. Image courtesy of dp polar.Troy Jensen pointed out the revenue versus profitability dilemma in the AM sector, wondering why companies with substantial revenues like Stratasys and 3D Systems aren’t profitable. Graves attributed the struggle for profitability to high R&D and SG&A costs necessary to support a broad technology offering and global customer base. He suggested that achieving a greater scale via consolidation could bring about more efficiencies and propel companies towards profitability.

Max Lobovsky expressed a slightly different perspective, stressing the importance of leading in specific print engine technologies rather than cobbling together different product lines through consolidation.

“I definitely agree that clearly empirically the industry is not profitable as a whole. I think there needs to be consolidation to get there. There needs to be some larger leading players, too,” Lobovsky said. “A lot of the attempts at consolidation so far have been cobbling together different product lines that maybe achieve sort of leverage, but Jeff mentioned each of these product lines need their own R&D investment if they’re going to continue to be leading. We look at scale, not just total revenue in our company, because, if you get that by cobbling together 10 different print engines that you’re not really leading in and not investing in sufficiently, then it’s not going to be profitable. You’re not going to be growing… When you look at leading tech companies in other spaces, you’ll see that companies like Apple and Tesla have very focused product lines. They have fewer SKUs than some of their smaller competitors with more revenue behind each one. I think that is that’s key.”

Scott Dunham also weighed in, adding that a more focused approach, rather than spreading thin over numerous technological concepts, might be beneficial. He mentioned the challenge posed by the vast price range in product portfolios and suggesting that a deeper focus on specific applications and the right machines for those applications could be a better strategy moving forward.

AM Investment Strategies 2023 perfectly set the stage for what to anticipate at Formnext 2023, showcasing new technologies and solutions aimed at propelling the AM industry forward. The conversation will continue there and beyond, including at the upcoming Additive Manufacturing Strategies event in New York, February 6-8, 2024, where many of the same players here will be in attendance alongside many of the other luminaries of 3D printing.

Subscribe to Our Email Newsletter

Stay up-to-date on all the latest news from the 3D printing industry and receive information and offers from third party vendors.

Print Services

Upload your 3D Models and get them printed quickly and efficiently.

You May Also Like

Divergent Declares that German 3D Printers are Superior, And Plans Massive LPBF Expansion

Divergent has announced a new version of its Laser Powder Bed Fusion (LPBF) printer and a new site. The company aims to do nothing short of “further accelerating its mission...

Inside Haddy: Jay Rogers Wants 3D Printing to Build Real Products, Not Just Prototypes

A warehouse from the outside, but step inside Haddy and it shifts quickly: finished pieces up front, clean and minimal, furniture you can touch and sit on. Walking through the...

SpaceX IPO Puts a Major 3D Printing Powerhouse on Wall Street

SpaceX officially began trading on the Nasdaq today under the ticker symbol SPCX, marking one of the most anticipated and largest public offerings in Wall Street history. The company priced...

DEEP Manufacturing Collaborating with Fortius Metals to Demonstrate WAAM at Scale

DEEP Manufacturing is trying to build pressure vessels and marine habitats at scale with DED technology. Using commercial robot arms and wire arc additive manufacturing (WAAM), the company is hoping...