There Is a Surprising Threat to 3D Printing R&D in the U.S.

Additive manufacturing (AM) is a young and flourishing technology and there is a great deal of ongoing research and development (R&D) being performed. AM patents are growing at a 36% annual rate, or about ten times faster than for all other patents, according to a paper by the European Patent Office.

Much of that R&D is funded by government agencies like the Defense Department, NASA, NIH, DOE and others because they recognize that AM can serve their goals in powerful and unique ways that were unimaginable even a decade ago. Yet, the future of that R&D work is now threatened for a surprising reason: the U.S. tax code.

R&D Becomes Taxable

In 2017, Congress passed a law called the Tax Cut and Jobs Act (TCJA). While some taxes were cut by $120 billion, the bill was passed in a way that required the bill to be “revenue neutral” (i.e., would not increase the national deficit) over a 10-year period. To accomplish this, $120 billion of additional revenue (read “new tax”) was needed. Unfortunately, Congress decided these additional taxes would be derived from R&D performed by industry.

For the past 70 years, U.S. tax policy was to encourage R&D investment and innovation by allowing companies to expense (or “write off”) 100% of their R&D expenses in the year incurred. The U.S. is not alone in this regard; all but two countries in the world allow this, for the same reason. In fact, China allows its businesses to deduct 200% of their R&D expense for tax purposes.

Under the TCJA law, however, this was changed. Now, U.S. companies can only write off 10% of their R&D expenses in that year and must amortize the balance over the next five years. The other 90% of those expenses now appear as taxable income in that year. The resulting effect on income tax due is enormous.

Firms Caught by Surprise

Although the law was passed in 2017 and the tax cuts in it went into effect immediately, the increased tax on R&D only went into effect in 2022. Therefore, many affected firms did not even realize this until April 2023, when they filed their 2022 tax returns. For many, it was an extremely unpleasant surprise, to say the least.

This affects any company performing R&D, large or small, whether on its own behalf or for a customer. For example, Raytheon has reported its tax bill increased by $1.5 billion for a nine-month period because of this provision, the annual tax increase for Northrop Grumman was $1 billion and Lockheed Martin’s taxes increased by $450 million for just a single quarter. For smaller firms, while the tax bill is for smaller amounts, the effects can be much more devastating.

Illustrating the Impact

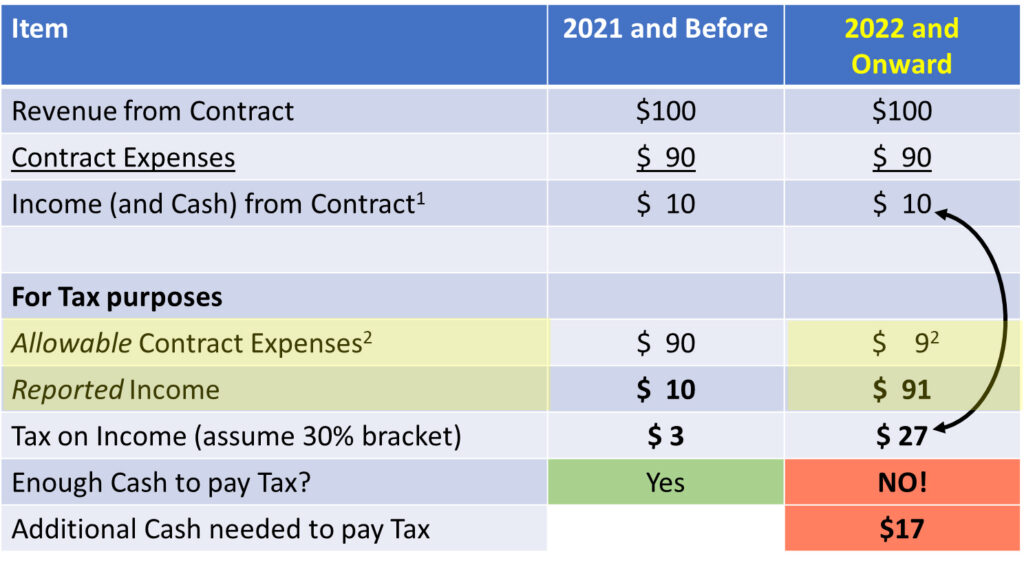

Consider a hypothetical $100 R&D contract shown below for illustration. Previously, this contract would generate income of no more than 10% of the contract value, or $10. The tax on that income depends on the company’s tax bracket; in this example we assume a 30% tax bracket. That means the Tax due is $3 which is paid from the profit or income generated by the contract.

Comparison of Tax due generated from a hypothetical $100 R&D contract before and after present Tax law went into effect in 2022. Note 1: Government R&D contracts typically allow a profit or fee of up to 10%. Note 2: Under current Tax law, firms can only deduct 10% of their R&D expenses in the year incurred.

This changed dramatically in 2022 because of the new tax law. That same $100 R&D contract now creates an apparent income of $91 for tax purposes. Using the same tax bracket, the firm now owes $27 in Taxes. And yet, their real income from the contract is still only $10 because those $90 in expenses are real and have already been paid.

If the tax is $27 but the cash income from the contract is only $10, where does the company find the cash to pay its tax due?

For large, well-established companies with other revenue and income streams (like Raytheon) there is cash to pay the tax obligation from the R&D contract. But if the firm is smaller or less mature, those sources (or cash reserves) often do not exist. That is the case for many small businesses that participate in the federal Small Business Innovation Research (SBIR) program. For many of these firms, the tax change is an existential crisis.

A Real-world Example

Laser Fusions Solutions in Dayton, OH is a one-person metal AM service bureau that also performs novel AM research. Part of CEO Chris Barrett’s strategy is to use federal small business, SBIR and Small Business Technology Transfer (STTR), contracts to cover salaries on R&D projects while expanding the installed base of machines for the service business.

Before learning about the new tax consequences of R&D work, Laser Fusions Solutions submitted an STTR proposal to the Navy to develop novel machine control capabilities and was then notified they were selected for the award. While excited to perform the work, Barrett had since learned about the new R&D tax law. He now needed to make a tough choice: accept the contract or pass on it? And, if he took the contract, how would he pay the large tax due?

Ultimately, after meeting with his accountant, he decided to accept the contract. He plans to save for the much higher taxes due by continuing to forego a paycheck for the foreseeable future and deferring plans to expand his service business.

“We seriously considered not accepting the award, even after having invested time and effort to win it. We’d much rather invest our cash to capitalize our own business, rather than effectively subsidizing the government’s R&D needs,” says Barrett.

Shrinking R&D Supplier Base

This situation is equally difficult for the government agencies for whom the R&D was performed. Previously government-funded R&D awards like SBIR were highly sought and competitive, with about 10 proposals submitted for every one contract awarded. However, today it is very likely that almost no firm, especially newer ones, will find it attractive to bid for the opportunity to significantly subsidize the government’s R&D out of their own limited funds. The government will likely receive far fewer R&D proposals going forward and the value and quality of work they receive for whatever awards they make are likely to suffer.

Laser Fusions Solutions, like virtually all U.S. industry organizations, is hopeful that Congress will retroactively reverse current tax law on R&D expenses. While several bills have been introduced in the current Congress to do just that (see LinkedIn post below), their outcome is very much unknown at this time. Similar bills have been introduced in the six years since the TCJA law was passed, and all such efforts failed to become law.

This author and other organizations are actively working with Congress to change the law so that industry can once again be encouraged to invest in R&D and innovation, not only for AM but in all other fields.

David Maass is President of Flightware, a firm that provides R&D and other services to both industrial and Government clients. He has been active in AM R&D, funded through the SBIR program in which he has participated for more than four decades.

Subscribe to Our Email Newsletter

Stay up-to-date on all the latest news from the 3D printing industry and receive information and offers from third party vendors.

Print Services

Upload your 3D Models and get them printed quickly and efficiently.

You May Also Like

3D Printing Markets Totaled $4.35 Billion in Q1 2026, AM Research Report Shows

According to the latest data from Additive Manufacturing Research (AM Research or AMR), the 3D printing markets totaled $4.35 billion in the first quarter of 2026. The leading industry analyst...

The Next Phase of EB-PBF Will Be Defined by Beam Control

The bar for metal additive manufacturing has moved. Early on, the question was often simple: Can the machine print the material and produce a dense part? That still matters, but...

UAS Additive Strategies Shows How Fast Drone Manufacturing Is Changing

The recent UAS Additive Strategies online event, hosted by 3DPrint.com and Additive Manufacturing Research (AM Research), brought together leaders from across the additive manufacturing (AM) and drone industries to discuss...

The Drone Industry is Showing Where 3D Printing Delivers Real Value, AM Research Report Finds

The rapid rise of drones is creating one of the biggest opportunities for additive manufacturing (AM). Whether they’re used on battlefields, inspecting bridges or crops, or delivering supplies, drones need...