COVID-19 Doesn’t Shake Reinforced Optimism of 3D Printing Businesses

Recent announcements regarding earnings and financial performance through the first quarter of 2020, have given some insight into the impact COVID-19 has had on major 3D Printing businesses worldwide.

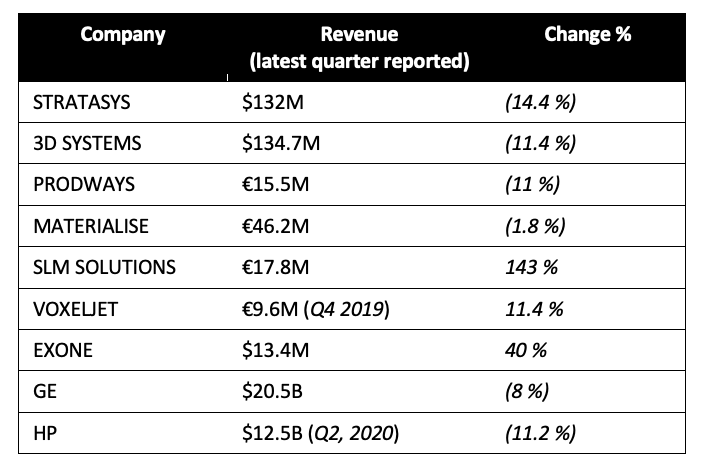

Earnings Results Comparison (by Revenue, M-millions, B-billions).

While ensuring employee safety and business continuity remained paramount, public companies were simultaneously challenged by a sudden decline in consumer demand, a continuing halt or reduction in onsite activities, and global supply chain issues, which began in China shortly before impacting Europe and the Americas.

Revenues for Stratasys and 3D Systems declined by 14% and 11% respectively, whereas strong order backlogs from 2019 led to significantly higher revenues realized for SLM and ExOne. SLM had the best first quarter performance in the company’s history with a 143% increase compared to 2019.

ExOne’s latest system is the 160Pro metal binder jetting 3D printer. Image courtesy of ExOne.

3D Systems saw revenues decline across segments, except materials, which stayed flat. The company faced a drop in consumer demand in automotive, aerospace, healthcare and dental, as well as disruptions in production facilities and on-site services. Despite sustained cost reduction measures and improving operating expenses by 13%, its shares depreciated 5% with 0.04 loss per share for 2020, compared to 0.09 loss per share for 2019.

In addition to the decline in Q1, Stratasys expects a sequential decline in Q2 of 5-10%. Yet the company believes its balance sheet with $325M in cash, coupled with its ability to generate cash and control costs, will help it manage the short-term hit in revenues, and strongly expects margins to recover.

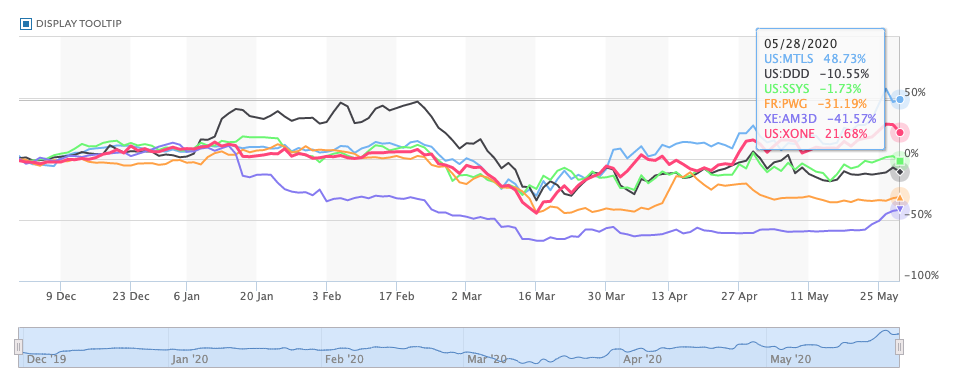

Change in stock prices for several of the major 3D printing stocks, excluding GE, HP and voxeljet.

Across businesses, revenue decline has primarily been attributed to short-term impact of reduced manufacturing activity and industrial production due to COVID-19, resulting in a fall in consumer demand across segments. In addition, a pause and postponement of investment has seen lower capex spend across key industries such as automotive, aerospace, healthcare and oil & gas. Demand for new hardware and software licenses has declined, partly offset by recurring revenues from materials, consumables, or after-sales services. In some sectors, such as dental, material consumption has slowed as elective procedures are delayed or cancelled. In general, machine and software segment revenues have seen a decline, but recurring revenues from the installed base of 3D printers has seen revenues from the materials segment increase or stay flat. For instance, Prodways saw a decrease of 6.3% in machines and software, but a 25% increase in materials revenues.

This change in demand is seen as more of a ‘pushing-out’ of capex spend, than a cancellation. Order intakes stayed flat or reduced overall, as customers in key industries postponed capital expenditure and investment due to COVID-19 uncertainty and impact.

The impact in operations differed, as businesses with localized supply chains were less impacted—such as SLM who also kept safety stocks for high-risk and long-lead time items—as compared to 3D Systems or HP, who faced production and capacity disruptions in their global supply chains.

The NIP mask, developed by Materialise to help treat COVID-19 patients. Image courtesy of Materialise.

Materialise saw a slight revenue decrease of 1.8% with gross profits decreasing 3.7% compared to last year’s quarter. Though their software and medical segments grew, there was a steeper decline in their manufacturing segment revenues, which account for 45% of total revenue. The company delivered higher than expected revenues this quarter with a gross profit of $109M, and despite varied market performance recently, has seen its shares up 25.4% year to date.

ExOne, sold 14 of its metal and sand binder jetting machines in the quarter, with a 40% increase in revenues and a 19% improvement in net loss with $3.6M in Q1 2020, resulting in a $0.22 loss per share for 2020 compared to $0.28 in 2019.

Revenues at GE Group fell 8% to $20.5B, with is power and aviation division significantly impacted by its exposure to the decline in the commercial aerospace sector. However, GE’s Healthcare and Lifesciences segment saw demand surge 6% due to COVID-19. Yet the company has seen its shares lose more than 40% of their value this year and expects the second quarter results to decline sequentially, showing the first full quarter impact from COVID-19.

HP Inc has reported second quarter results with net revenues were down 11.2% to $12.5B compared to 2019, with personal systems declining 7% and printing 19%. In Printing, the company has set long term margin targets of 16-18%. In 3D Printing, HP has recently partnered with New Balance and Superfeet to grow its end-user solutions in scanning and printing, and is counting on key verticals such as healthcare for continued growth. The company is continuing its focus on structural cost optimization and productivity gains, hoping to generate over $2B in savings. It has also provided guidance of $2.33-2.43 per share for 2020 and $3.25-3.65 per share for 2022.

Superfeet secures New Balance license agreement for insoles 3D printed using HP technology.

Voxeljet’s share price has reduced dramatically over the last five years, despite steadily growing revenues. It has until December, 29, 2020 to regain compliance with NYSE after its average closing share price had fallen below $1.00 standard and the $50M market capitalization standard. Yet the company has reported Q4 2019 revenues with an 11.4% increase over 2018, and a record order backlog. While it does expect disruptions in operations and supply chain due to COVID-19, it anticipates demand for its large-scale printers to continue, expecting annual revenue for 2020 to be between €25-30M.

Companies have also been proactive within their organization to manage the impact of the crisis to their employees, customer base and business operations. From introducing remote working, reduced work week or shifts, and other employee-facing policies, to implementing safety and health protocols, freezing non-essential hiring and travel, and short-term optimization measures to ensure business continuity and avoid large-scale layoffs. For instance, salaries for all Stratasys employees and executives was reduced by 20%. Executives and board members at 3D Systems took a 10% pay cut with a majority of employees on limited furloughs, and partial activity measures were introduced for almost 50% of Prodways employees worldwide. Businesses have also taken measures to optimize operational costs, revaluate their supply chain and production costs, and increase focus and spend in digital, particularly in sales and marketing, for the long-term.

Overall, while Q1 earnings do show some signs of business impact, businesses are pointing towards Q2 as to where the full impact will be seen, since the pandemic peaked largely in the latter half of the first quarter, through March and April. In this regard, businesses have trended toward withdrawing guidance for the rest of the year, as uncertainties due to COVID-19 continue, while stating that second quarter results are expected to show a more considerable impact. Although there is a near-term focus on cost reduction, optimization and ensuring liquidity, 3D printing businesses are positive in their long-term outlook. Key industries are expected to remain structurally unaffected, with markets returning to the new normal in the second half of this year, and AM’s increased relevance has reinforced optimism in the industry’s long-term growth. No major shifts in long-term strategy or investment have been made yet due to COVID-19, with investments in on-going R&D continuing.

With their real-time response and contribution during COVID-19, 3D Printing businesses have led the way and impacted the front-line pandemic response, providing rapid, direct support for personnel safety and in essential medical devices and equipment. The response also proved AM’s capability in high-volume and bridge production, its potential in localizing and distributing manufacturing, flexibly and at speed, whether to retool or expand existing production, or to develop new, improved products faster, especially in healthcare. If anything, the pandemic response has only underlined the critical and long-term value of AM in addressing real-world gaps and needs, in ways that traditional manufacturing and supply chains just cannot.

Subscribe to Our Email Newsletter

Stay up-to-date on all the latest news from the 3D printing industry and receive information and offers from third party vendors.

Print Services

Upload your 3D Models and get them printed quickly and efficiently.

You May Also Like

China Becomes Latest Space Power to Demonstrate Metal 3D Printing in Orbit

China has demonstrated metal 3D printing in space as part of its plan to develop manufacturing technologies for future space missions, including Moon construction. The experiment took place aboard the Qingzhou...

AMPulse Asia: APAC 3D Printing Market Roundup

Key Takeaways Coverage window: April 27 to May 10, 2026. Roughly 30 additive manufacturing (AM)-relevant announcements were tracked across eight Asia-Pacific countries. Largest disclosures: Farsoon Technologies (688433.SH) filing a RMB...

3D Printing Financials: Stratasys Bets on Defense and Drones as Printer Sales Slow

Stratasys (Nasdaq: SSYS) started 2026 with lower revenue and a larger loss as customers continued to slow down spending on new 3D printers. Still, the company pointed to stable recurring...

3D Printing Financials: Xometry Surges After Record Quarter and Siemens Deal

Shares of Xometry (Nasdaq: XMTR) surged on Thursday, May 7, after the company reported record first-quarter 2026 results and announced a major partnership with Siemens. The stock climbed as much...