Defense 3D Printing to Reach $2.2B by 2032 in North America – AM Data Slice

“AM Data Slice” from Additive Manufacturing Research (“AMR”, formerly SmarTech Analysis) is a weekly segment that offers readers an insightful dive into the additive manufacturing (AM) landscape, showcasing pivotal statistics and trends derived from AMR’s exhaustive research. This week’s focus is on investments into 3D printing for government defense projects in North America from 2020 to 2032.

For a number of reasons, military use of 3D printing has long been one of the industry’s primary drivers. This has mostly been at the behest of the aerospace segment. However, more recently, additive manufacturing (AM) has seen more widespread deployment across various areas of the globe-enveloping military-industrial complex. In large part, this is due to the fact that, particularly since COVID and the war in Ukraine, manufacturing has become a national security issue, with ensuring consistent access to key parts being necessary for military affairs.

So, now, we’re seeing 3D printing adopted as a form of supply chain insurance for the entire military apparatus. At the same time, the cutting edge capabilities that AM allows are being used to push military manufacturing in a variety of ways, including the ability to deploy improvisational production capabilities on the front lines. As a result, we’re seeing the following trends.

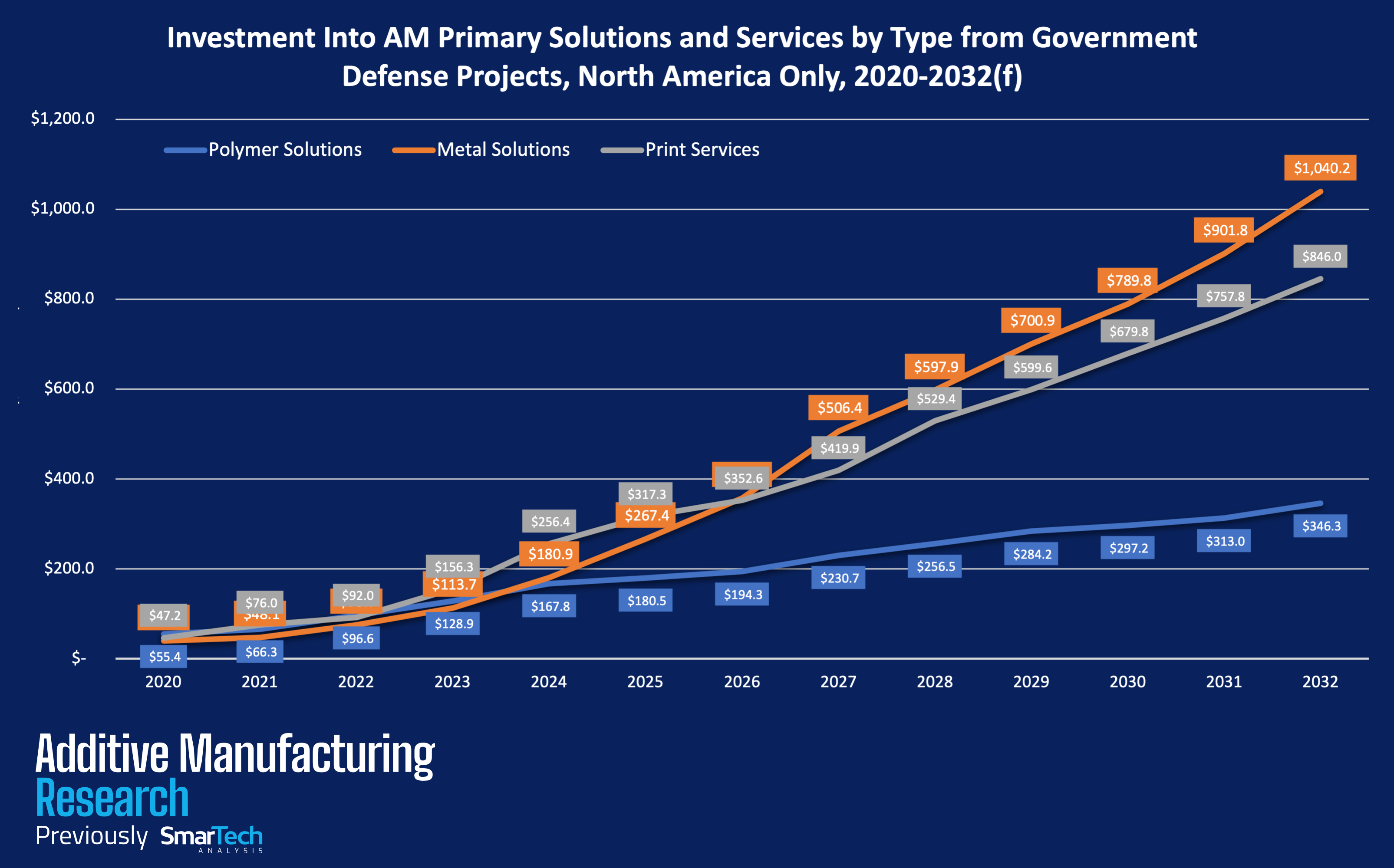

Starting in 2020 with an investment of $55.4 million, the polymer AM revenue for defense applications is growing steadily. By 2024, it is estimated to reach $167.8 million, and by 2032, it’s projected to reach $346.3 million. Investments in metal solutions began at $39.6 million in 2020, but is expected to experience a significant surge, especially from 2024 to 2026, where the value will jump from $180.9 million to $357.6 million. By 2032, the projected value stands at a whopping $1.04 billion. Whereas polymers demonstrate a compound annual growth rate (CAGR) of 17.1% across the entire period, the CAGR of metals is nearly double at 32.4%. This is to be expected given the comparative maturity of the two technologies and the greater utility of metal AM in military applications.

Starting from $47.2 million in 2020, print services will see a consistent increase in investment over the entire period. By 2024, the value is expected to reach $256.4 million, while projections for 2032 indicate an investment of $846 million. Notably, there’s a considerable increase in investment from 2027 to 2028, jumping from $419.9 million to $529.4 million. The CAGR is anticipated to be at 28.8% across the period.

Combining all the categories, the total investment in AM started at $142.2 million in 2020. It will see a dramatic rise, crossing the billion-dollar mark by 2027 with $1,157 billion. The trend continues upwards, with 2032 projected to have an investment of $2.233 billion. The CAGR of the entire defense sector for 3D printing in North America is expected to be about 26.5 percent.

All of this is to say that North American defense spending on AM is growing at a very rapid pace. What’s particularly interesting is if you look at the exact periods of extreme growth. Whereas polymers have already seen the most growth AMR expects them to experience in 2022, metal AM is thought to hit its peak expansion rate in 2024, where it will hit 59.1%.

This year is the print services sector’s biggest year-over-year growth at 69.9 percent. This is understandable given the fact that services are typically required to onboard the uninitiated into a new production method to ease their adoption. It may also be the primary reason that companies like ADDMAN Group, Morf3D, and Sintavia, which are focused on high-performance and high-value areas in the defense and space sectors, are experiencing such growth.

Finally, it’s worth noting that 2024 is estimated to be the year with the highest expansion rate, 51.7 percent. Right now, we are in the midst of a rapid adoption program by national governments, particularly that of the U.S. Through Biden’s “Made in America” executive order, Inflation Reduction Act, Bipartisan Infrastructure Law, AM Forward, and the CHIPS Act, the U.S. defense supply chain has had plenty of opportunities to push 3D printing integration. With this in mind, it’s worth considering that, if this is how North America is spending on military 3D printing over the next decade, what will AM adoption look like in the rest of the world during the same time?

Subscribe to Our Email Newsletter

Stay up-to-date on all the latest news from the 3D printing industry and receive information and offers from third party vendors.

Print Services

Upload your 3D Models and get them printed quickly and efficiently.

You May Also Like

First Containerized System from AML3D Now Operational at US Navy AM CoE

Shipbuilding giant Austal USA recently announced the launch of the Digital SEA (Secure Exchange for Additive) platform, which should play a major role in expanding accessibility to the sorts of...

3D Printing Financials: Materialise Improves Margins Despite Flat Revenue

Materialise (Euronext and NASDAQ: MTLS) started 2026 with stable revenue, stronger margins, and better operating profit, helped by growth in medical and improved profitability in software. The Belgian 3D printing...

3D Printing News Briefs: May 7, 2026: Metal Powder Bed Fusion, Surgical Plates, & More

In today’s 3D Printing News Briefs, we’ll start with a strategic collaboration to advance next-generation metal additive manufacturing (AM), before moving on to funding for surgical research. We’ll end with...

3D Printing News Briefs, May 2, 2026: Soft Robots, Agricultural Waste, & More

In this weekend’s 3D Printing News Briefs, we’ll start off with a multi-laser metal powder bed fusion 3D printer and post-processing news. We’ll end with research into soft robotics and...