The Current State of Metal 3D Printing in 2020

As a subset of 3D printing, metal printing has been growing over the last couple of years. The technology has made great strides in speed and versatility of materials, with a number of companies trying out many different technologies. While plastics are still the most prominent materials used by companies and external services, metal printed components are a close second tying with resins, while both are surpassing ceramics. Needless to say, a lot has changed from a mere 5 years ago, so this article will look at the specifics of how the metal printing industry is fairing in 2020.

Here are our key takeaways:

Industry Overview & Crucial Cases

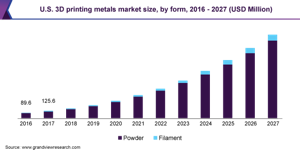

Metal printing has seen some increase in usage, market size and interest from manufacturers. The rise in these statistics has been due to decreasing costs overall, along with an increase in awareness about the unique elements 3D printing brings to the table. The metal printing market was valued at USD 772.1 million in 2019, with a CAGR of 27.8% from 2020 to 2027 according to Grandview Research. Similarly, market research from Technavio into the global suggests the industry will be growing by $1.59 billion between 2020 and 2024, at a CAGR of over 26%. Either way, the industry looks to be fairly healthy by both estimates.

Greater design flexibility, low waste and cost effectiveness have all been contributing factors in this growth as well. With multiple crucial deals across many manufacturing industries, there has been a shift towards more end-use production causing more firms to take note of the technology. Laser systems and powders, in particular, have become quite a bit cheaper, yet still quite expensive (as we’ll get into later in the materials section).

Image via Grandview Research

Adoption has been increasing, though most of it has been through external parties and services rather than in-house systems. In a survey of 1000 respondents, 36% of firms used metal components for 3D printing in 2018 compared to the 28% in 2017. This trend continues in Sculpteo’s State of 3D Printing study, indicating 45% of companies using metal as a 3D printing material, with an additional 10% considering adding it in some capacity to their own business, whether as external or internal.

The overall 3D printing industry is evolving rapidly, with 3D printers becoming faster, more reliable and production capable, and this has also been true of metal printers. In terms of types of industries, the most prominent are automotive, medical, defense and aerospace. All of these industries tend to metal printing for rapid prototyping, end-use products, tooling and research and development. For example, rapid prototyping in the aerospace segment is expected to cross a valuation of USD 105 million by 2026 for all materials combined. Mainly, aerospace firms are using 3D printing and metal printing technologies to minimize costs for developing models and prototypes.

Most notably, NASA intends to 3D print over 80% of its future rocket engines using metal systems. Before the end of the year, there is poised to be a $3.5billion investment in a production plant to make 100,000 fuel nozzles per annum for the aerospace giant’s engines. Companies are procuring major deals with big-name aerospace firms: case in point, Velo3D are giving their machines over to SpaceX and have also announced that they raised $28 million in funding back in April this year.

The defense sector is another major player that is seeing some interest from crucial 3D printing giants. The US Army commissioned 3D Systems to develop a prototype printer for them, mainly for producing durable steel components and weapons. The commission was budgeted for 15 million USD, requesting the company to create objects up to a volume of 1×1 by 0.6 metres. The massive laser printer can process alloys intended to develop bunker busting bombs, so it is surely going to be a crucial manufacturing system for the military.

The medical industry is applying a lot of metal printing in recent years as well. Notable examples include Stryker’s 3D-printed implants, including the 3D-printed Tritanium TL Curved Posterior Lumbar Cage, which received FDA approval in March 2018. Similarly, Slice Mfg. Studios says that each of its Arcam Q10 EBM machines can produce around 70 acetabular hip cups every five days. Methods like EBM and SLM have also been crucial in developing specialized tooling very quickly, allowing hospitals to generate parts in-house without extensive wait times.

The automotive industry has also produced some ground-breaking use cases. BMW is a power player in terms of scale and size of their 3D printing operation. Since 2010, the renowned car company has exceeded the one million 3D printed parts mark (in terms of all materials, not just metal). As for mass production, BMW is aiming for production of 50,000 components per year and 10,000 individual spare parts. These parts include the i8 Roadster’s roof bracket and window guide rail, and the M850i Coupe Night Sky Edition’s entire brake caliper.

Ford has also been working with 3D printing to great effect. Just earlier this year, Ford Performance printed what they claim is the largest 3D printed metal automotive part of all time. This aluminium manifold inlet forms a complex web‑like structure which would have been impossible manufacture using traditional manufacturing systems. The printers, on the other hand, developed the part within five days. Overall, Ford’s entire 3D printing operation saves them roughly half a million dollars per month.

Volkswagen has been using HP metal jet systems for thousands of parts and has announced intentions to increase their additive manufacturing operations for functional parts. Volvo, Volkswagen and Bugatti have all been major implementors of the technology in recent years. All of them are using it for tooling, prototyping and fixtures, but metal parts are particularly prominent in the end-use applications.

Technologies & Materials

Image via HP

With a growing number of technologies in this sector, there are quite a few standouts. DMLS/SLM are currently the most heavily utilized, with a majority of usage stemming from external services. Binder Jetting and Electron Beam Manufacturing are also crucial metal production technologies with significant market shares (usage stats stand at 40% and 28% of companies respectively). 50% of Sculpteo’s respondents who use metal printing tend to employ Selective Laser Sintering, Jet Fusion, SLM/DMLS and Binder Jetting through external services. They mainly use the technologies to counter machine/ maintenance costs.

DMLS or SLM are probably the most prominently used technologies as of now. Its use of steel, aluminum and titanium make it ideal for aerospace and medical sectors, along with dentistry and automotive. The main advantages companies find in SLM that boosts it above other manufacturing methods is the ability to produce lightweight complex, functional metal structures at relatively low costs.

Binder jetting is another popular technology but it still has a few materials availability hurdles. The most commonly available alloys are stainless steels and tools steels such as 1.4404/316L or 1.4542/17-4 PH. Furthermore, titanium alloys are available for Binder Jetting from companies such as DIGITAL METAL but they are not extensively available. Nickel-based alloys, copper and bronze materials and carbides are currently under development. Aluminum alloys are fairly common other forms of 3D printing, but due to general difficulties associated with sintering it, they are still in the development phase when it comes to binder jetting.

Metal powders and resins have gotten cheaper, which has boosted up the demand for technologies that use them. Metals used in 3D printing include aluminum, bronze, cobalt alloys, copper, gold, nickel alloys, palladium, platinum, silver, steel, titanium alloys and tungsten. While steel and aluminum along with their variations still dominate the metal printing scene, there has been a notable increase for other metals (including precious metals). The growth in precious metals usage may possibly be attributed to the jewelry industry’s increasing adoption of metal printing systems.

The differences between the plastics and metals arena is also notable. Plastics are still the dominant materials but metal parts are on the rise. From 2017 to 2018, the portion of 3D printers that use plastic declined from 88% to 65%, but within the same period, metal use rose 28% to 36%. The systems are also getting more powerful, with new technologies like metal jetting and Binder jetting speeding up production.

Future Projections & Obstacles to Adoption

IDTechEx forecasts that the majority of the annual revenue will come from material demand rather than printer sales and installation. In their IDTechEx Research forecasts, they also predict that the global market for metal 3D printing will reach a value of $19 billion by the year 2029.

Increasing interest in the aerospace and defense industries is leading to more mission-critical parts being developed with metal systems. Many organizations like NASA and the US Army have indicated an interest in increasing their 3D printing output as they go forward. Many experts, including Digital Metal CEO Christian Lönne, have their eyes on Binder Jetting as a potential rising star in the future. Metal printing will become more popular due to their ability to employ new geometries, weight reducing designs, fewer production steps and higher production flexibility.

Automotive applications are anticipated to reach over USD 240 million by 2026. Europe in particular is estimated to witness significant gains (over 20%) going onward to that period. The EU directive 2015/719 passed by the EU commission pledges companies for minimizing vehicular weight to improve fuel efficiency and emission control. This should theoretically drive the additive manufacturing and metal powders market. The EU automotive sector also accounts for over 4% of their GDP. As a major automobile production region, this will have positive impact for 3D printing and additive manufacturing demand.

As usual, the main obstacles to further implementation are reliance on existing systems, production times and money. Aside from the cost of materials, metals require a substantial time to manufacture into the end products that companies desire. The high lead times restrict most of the manufacturers from switching to additive manufacturing, rather opting for their conventional manufacturing process. Lead times are a major issue in the adoption of 3D printing for major industries and firms within them, including many aerospace & defense companies, automotive companies and electrical & electronics manufacturers. Although these industries are using 3D printing, there are still skeptics, particularly in firms which need rapid, mass production. Yet, there is a lot of growing interest, so maybe many of these companies will be swayed in the coming years.

Feature image courtesy of Velo3D.

Subscribe to Our Email Newsletter

Stay up-to-date on all the latest news from the 3D printing industry and receive information and offers from third party vendors.

Print Services

Upload your 3D Models and get them printed quickly and efficiently.

You May Also Like

3D Printing Financials: XTPL Adds New Semiconductor and Defense Customers in Q1 2026

Polish microprinting company XTPL (WSE: XTP) reported first-quarter 2026 revenue of PLN 1.6 million (roughly $441,000) as the company expands into the semiconductor and advanced electronics markets, while also launching...

3D Printing News Briefs, May 30, 2026: RIMPAC 2026, Acquisition, Ceramic Implants, & More

We’re kicking things off with materials news in this weekend’s 3D Printing News Briefs. Then it’s on to a hybrid manufacturing system for a maritime exercise, an expansion of industrial...

The University of Utrecht: “3D Printing Could Change Who Gets to Become a Manufacturing Power”

For decades, manufacturing has mostly been controlled by countries with huge factories, lower labor costs, and industrial systems that took years, sometimes decades, to build. But Utrecht University human geographers...

3D Printing News Briefs, May 28, 2026: Continuous Fiber Reinforcement, Bioprinted Trachea, & More

In today’s 3D Printing News Briefs, America Makes announced the winners of its JAQS-SQ Project Call. Axtra3D is partnering with Keystone Industries to expand its dental material ecosystem, while BigRep...