GE’s $1.4 Billion Metal AM Acquisitions Falter as Elliott Management Rejects Terms

Last month, GE made an acquisition announcement that was sure to shake up the additive manufacturing industry, with its $1.4 billion investment proposal to acquire both SLM Solutions and Arcam. With support coming from the involved companies’ management teams, the massive proposal seemed set to reshape the makeup of the metal AM industry; however, recent hiccups are showing that the deal is by no means a slam dunk for GE, as shareholders are not demonstrating unanimous inclination to agree to the terms set out. On the date of the announcement, September 6, Arcam and SLM Solutions both issued statements of support encouraging acceptance of the takeovers:

Last month, GE made an acquisition announcement that was sure to shake up the additive manufacturing industry, with its $1.4 billion investment proposal to acquire both SLM Solutions and Arcam. With support coming from the involved companies’ management teams, the massive proposal seemed set to reshape the makeup of the metal AM industry; however, recent hiccups are showing that the deal is by no means a slam dunk for GE, as shareholders are not demonstrating unanimous inclination to agree to the terms set out. On the date of the announcement, September 6, Arcam and SLM Solutions both issued statements of support encouraging acceptance of the takeovers:

“Based on the above, the Board believes that the Offers recognizes Arcam’s growth prospects, as well as the risks associated with those prospects. Accordingly, the Board unanimously recommends the Arcam shareholders to accept the Offer,” the Arcam Board concluded of their review of GE’s offer.

SLM’s statement at the time was also toward a positive response, pending review, with the board explaining:

“After receiving the offer document that GE Aviation is going to publish, the Executive and Supervisory boards of SLM Solutions Group AG will issue a detailed opinion on the offer in accordance with their statutory obligations. Subject to the review of the offer document, the Executive and Supervisory boards currently intend to support the envisaged takeover offer. The opinion of the Executive and Supervisory boards will be published on the company’s website at www.slm-solutions.com/investor-relations.

If the takeover offer is successful, 31.5 % of the company’s shares, which are currently held by existing shareholders, will be transferred to GE Aviation: The Chairman of the Supervisory Board Hans-Joachim Ihde currently holds around 24.1 % of the 17,980,867 SLM Solutions shares via Ceresio GmbH. Executive Board member Henner Schöneborn and his family currently hold shares of approximately 2.0 %. Further, Parcom Deutschland I GmbH & Co. KG holds approximately 5.4 % of the shares in SLM Solutions Group AG.

The implementation of the takeover offer will be subject to a few market standard conditions, in particular a minimum acceptance threshold of 75 % and the approval by the competent anti-trust authorities.”

As October rolled around, SLM’s Management and Supervisory Boards had reviewed the offer and its implications for the company. On October 5th, the Boards issued a statement signifying their unanimous recommendation of approval for the takeover.

As October rolled around, SLM’s Management and Supervisory Boards had reviewed the offer and its implications for the company. On October 5th, the Boards issued a statement signifying their unanimous recommendation of approval for the takeover.

“Following a process of detailed analysis and consultation, the Management Board and the Supervisory Board are both of the opinion that the takeover offer serves the interests and objectives of SLM Solutions, our shareholders, our customers and our employees. We therefore welcome the offer of GE Germany Holdings and support it wholeheartedly,” stated Dr. Markus Rechlin, CEO of the SLM Solutions Group AG, on behalf of the Group’s boards.

With the companies themselves agreeing that GE held their best interests in close consideration, the takeover seemed set to go forward — however, nothing is ever quite so simple in high-stakes business moves such as these major acquisitions. Last night, Thursday the 20th, American hedge fund Elliott Management Corporation, founded by billionaire Paul Singer, issued a statement of its intention to reject the current tender offer:

With the companies themselves agreeing that GE held their best interests in close consideration, the takeover seemed set to go forward — however, nothing is ever quite so simple in high-stakes business moves such as these major acquisitions. Last night, Thursday the 20th, American hedge fund Elliott Management Corporation, founded by billionaire Paul Singer, issued a statement of its intention to reject the current tender offer:

“Elliott believes that GE’s offer is not in the best interests of SLM shareholders. As a result, we will reject GE Germany Holdings AG’s tender offer for the outstanding shares of SLM on its current terms.”

Paul Singer [Image via Wikipedia: copyright World Economic Forum/swiss-image.ch/Photo: Remy Steinegger]

For its part, GE announced that it has no intention of sweetening the term from the initial proposal, nor will it extend the deadline. Without an adjustment to the deadline or offer, the tender is set to end on Monday. The offer to SLM shareholders has been set well above SLM’s stock price as of the day before GE made its announcement, with the €38 offered per share representing a 38% premium over prices on September 5. Today, SLM stocks dipped 11% as investors perhaps demonstrated unease with the offer succeeding; shares were trading early Friday afternoon in Europe at €35.22.

While both GE and the management of SLM Solutions are today encouraging shareholders to accept the tender offer, as the Wall Street Journal notes, the lack of change to the terms as well as the significant stake represented makes the “Elliott refusal a formidable stumbling block that will likely upend the deal” for GE. This stumbling block is illustrative of Singer’s push to, as he says, “exert influence” through Elliott Management.

“Singer has been boosting the stake since GE’s offer and has said that he intended to ‘exert influence’ over matters such as the company’s capital structure and the makeup of managing and supervisory bodies,” notes Industry Week of Elliott’s investment in SLM.

Furthering its influence in the entire acquisition proposal, Elliott additionally owns a 10.14% stake in Arcam. GE’s acquisition of Arcam is contingent upon a 90% tendering of shares, proving Elliott again to be potentially disruptive in the deal. An Elliott spokesperson declined comment to the WSJ about their stance on the Arcam takeover along with the news about their intention to reject the SLM proposal. However, GE has already had to extend their offer period in the Arcam transaction; NASDAQ reports that “GE had to extend the offer period after failing to draw a sufficient percentage of Arcam shareholders to accept its offer for their shares. GE said it had acquired a little more than 40% of the company’s shares when the offer period expired Oct. 14. The extension goes to Nov. 1.” (Industry Week noted that Investors owning about 24% of outstanding shares had accepted the deal” when GE extended this offer.) The management of Arcam remains positive about the proposed takeover, continuing to issue unanimous Board support for acceptance.

Furthering its influence in the entire acquisition proposal, Elliott additionally owns a 10.14% stake in Arcam. GE’s acquisition of Arcam is contingent upon a 90% tendering of shares, proving Elliott again to be potentially disruptive in the deal. An Elliott spokesperson declined comment to the WSJ about their stance on the Arcam takeover along with the news about their intention to reject the SLM proposal. However, GE has already had to extend their offer period in the Arcam transaction; NASDAQ reports that “GE had to extend the offer period after failing to draw a sufficient percentage of Arcam shareholders to accept its offer for their shares. GE said it had acquired a little more than 40% of the company’s shares when the offer period expired Oct. 14. The extension goes to Nov. 1.” (Industry Week noted that Investors owning about 24% of outstanding shares had accepted the deal” when GE extended this offer.) The management of Arcam remains positive about the proposed takeover, continuing to issue unanimous Board support for acceptance.

![]() In its interim report for January-September 2016 issued today, Arcam notes of the deal:

In its interim report for January-September 2016 issued today, Arcam notes of the deal:

“As announced on September 6, GE made a public tender to acquire all shares in Arcam. The initial acceptance period of the Offer expired on October 14. GE has extended the acceptance period until November 1, 2016.

For us at Arcam the tender from GE is a strong confirmation that the company we have built, our team together with you and other partners, is a major player in the additive manufacturing industry and an attractive partner to GE.

We share with GE the belief that Additive Manufacturing is a fast growing, strategically important industry. GE plans to retain and expand Arcam’s current customer base, in aerospace as well as in orthopedics. GE also intends to keep current locations of Arcam’s operations and to retain current management and employees. The Board of Arcam has unanimously recommended the shareholders to accept the offer and the statement by the Board can be found as a press release on the company website. Information about the public tender from GE can be found on our website and can be ordered from GE or from Handelsbanken.”

Industry experts are keeping a close eye on this activity, as the potential billion-dollar acquisition would bring together three powerhouses in metal additive manufacturing, offering a profound effect on and reshaping of the AM industry as we currently know it. Among these experts is Tasha Keeney, ARK Analyst with PRNT, the 3D printing ETF launched earlier this year, who tells 3DPrint.com:

“Elliott Management clearly sees the huge opportunity ahead for 3D printing. We estimate the market will grow from $5B today to $40B by 2020. To this extent, we can understand their logic.

On the other hand, GE/Arcam/SLM would be a great combination as GE would be able to use its industrial prowess to refine the technology and most likely needed the acquisitions just to fulfill its internal needs for 3D printed parts. GE likely produces hundreds of millions of parts per year, and we think less than 1% are currently 3D printed, so this is a massive opportunity.”

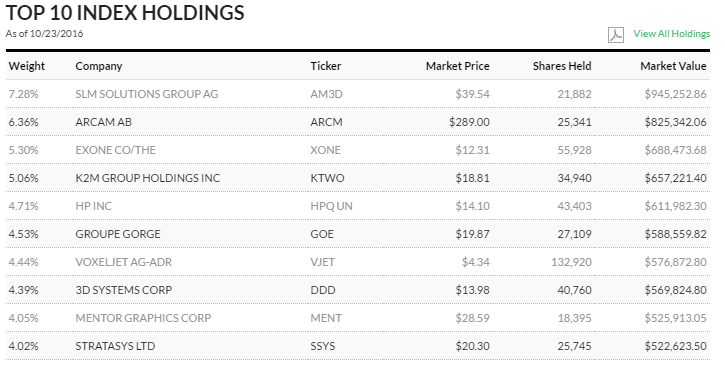

SLM Solutions and Arcam are both listed in PRNT’s top 10 index holdings, and certainly the ETF is keeping a very close watch on these proceedings. The metal additive manufacturing arena is a dynamic and extremely promising area for innovators and investors alike.

PRNT’s Top 10 Index Holdings today

Additionally sharing his thoughts with 3DPrint.com, John Meckler, former mutual fund portfolio manager of 3D Printing and Technology Fund, offers his expert insights in what the current status of the GE proposed acquisitions mean for the market as a whole, telling us:

“Activist fund interest in GE’s proposed 3D printing acquisitions has been a concern as both AM3D and ARCM stocks have traded significantly higher than their deal prices since the announcement in early September. Moreover Elliott Management has been amassing significant stakes in both companies for some time now. Elliott appears keenly aware of the significant value add both companies bring in IP, expertise, and existing market share in their respective 3D metal printing methods.

That said, Arcam and SLM operate capital intensive businesses with ferocious competition from larger existing 3D printing companies and looming from a number of other big tech multinationals. Elliott’s position is understandable but so is Arcam’s and SLM’s intention to sell. Overall this news is extremely bullish for the industry (specifically metal 3DP) even if the stock values are taking a hit.”

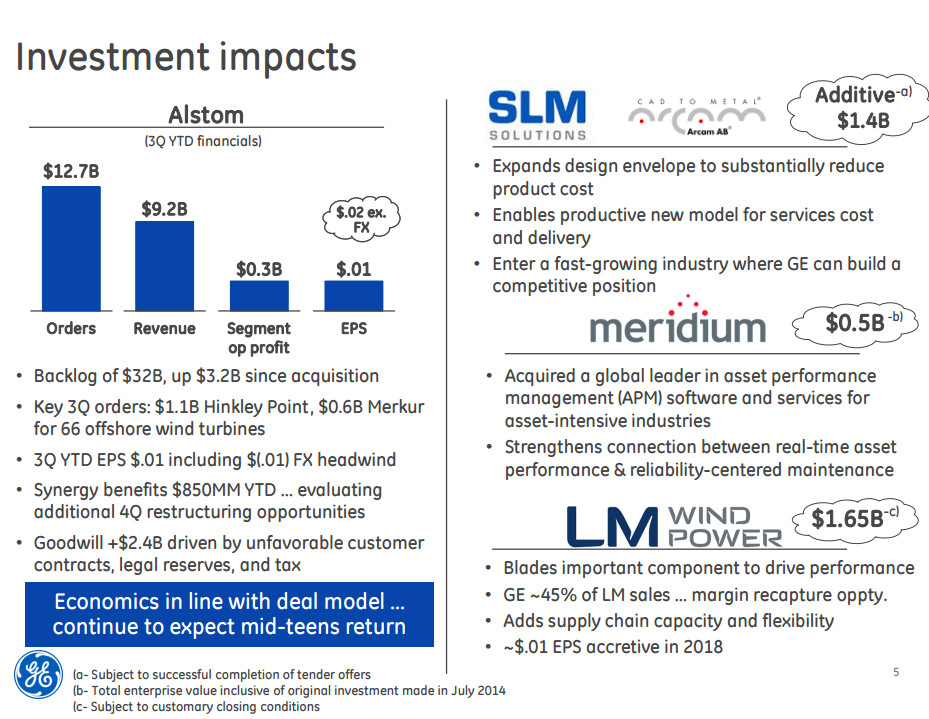

GE also announced its third quarter 2016 results today, highlighting some difficulties due to “slow growth and volatile environment” for much of its operations. The company highlighted the positive impact that the SLM Solutions and Arcam acquisitions would offer to operations, noting that investment impacts include (subject to successful completion of tender offers):

- Expands design envelope to substantially reduce product cost

- Enables productive new model for services cost and delivery

- Enter a fast-growing industry where GE can build a competitive position

These impacts were listed alongside other major investments by the company, including the recently announced $1.65 billion move to acquire LM Wind Power.

Slide from GE’s 2016 third quarter webcast presentation

Elliott has previously issued refusals in other European merger and acquisition deals in which Singer held out for higher offers, demonstrating the effectiveness of the hedge fund’s influence on M&A activity. Industry Week explains some of this established precedent:

“Elliott has a track record of investing in European acquisition targets and holding out for a better price. It also has shown a willingness to remain a minority holder to benefit from the offers while preventing complete takeovers.

The hedge fund recently refused to tender its stake in Axis Communications AB, keeping Canon Inc. from owning more than 87% of the company. Elliott held out when EQT Partners AB acquired Swedish software maker Industrial & Financial Systems IFS AB, eventually selling for about 9% more than other shareholders.

When U.S. drug distributor McKesson Corp. sought to acquire German counterpart Celesio AG, Elliott and other minority shareholders initially rejected the price. A deal was salvaged, with Elliott earning bigger profits from convertible bonds it had amassed.”

While GE works to settle the matter of its major acquisitions and where they fit into recent financial results, which has seen profits falling with slower-than-expected revenue growth, the AM industry will be keeping a keen eye on the latest in the conglomerate’s move to entrench itself more deeply into the metal additive manufacturing field. Stay tuned to 3DPrint.com as we closely follow this developing story. Discuss in the GE Acquisitions forum at 3DPB.com.

Subscribe to Our Email Newsletter

Stay up-to-date on all the latest news from the 3D printing industry and receive information and offers from third party vendors.

Print Services

Upload your 3D Models and get them printed quickly and efficiently.

You May Also Like

How One Artist Is Using 3D Printing to Tell Stories About the Ocean

Artist Kimberly Callas sees something different when she looks at a 3D printer. Where others see a machine for making parts, she sees a way to tell stories about the...

Bambu Lab Wants Home 3D Printing to Feel Less Like a Workshop with PLA Pure

As desktop 3D printers become increasingly common in homes, Bambu Lab is focusing attention on something beyond print speed and hardware features. This week, the company launched a new filament,...

AM Asia Watch: China Exported 2.46 Million 3D Printers in Four Months

China’s consumer 3D printer industry seems to be reaching a new level of global dominance. According to Chinese state media outlet China Global Television Network (CGTN), China exported 2.46 million...

Bambu Launches A2L: What the New Printer Reveals About Its Strategy

Bambu Lab continues its relentless march for 3D printing domination with the launch of the A2L. The 330 × 320 × 325 mm printer will have a nozzle temperature of...