Providing CONTEXT to the 3D Printing Market

At TCT Show, the floor was undoubtedly buzzing with activity — but beyond the booths there was more yet to see. With presentations from industry experts, analysts, academics, and more, the conference aspect of this show offered insights into various aspects of the goings-on in additive manufacturing today. Interviews on the show floor kept me busy, but there was one talk I had marked as a definite to attend: Chris Connery, Vice President of Global Analysis and Research of CONTEXT, would be presenting a 3D printing market briefing offering facts, figures, forecasts, and insightful analysis. Having met Connery weeks before at IMTS, I was certainly eager to hear a broader perspective on his and CONTEXT’s view of the overall market.

At TCT Show, the floor was undoubtedly buzzing with activity — but beyond the booths there was more yet to see. With presentations from industry experts, analysts, academics, and more, the conference aspect of this show offered insights into various aspects of the goings-on in additive manufacturing today. Interviews on the show floor kept me busy, but there was one talk I had marked as a definite to attend: Chris Connery, Vice President of Global Analysis and Research of CONTEXT, would be presenting a 3D printing market briefing offering facts, figures, forecasts, and insightful analysis. Having met Connery weeks before at IMTS, I was certainly eager to hear a broader perspective on his and CONTEXT’s view of the overall market.

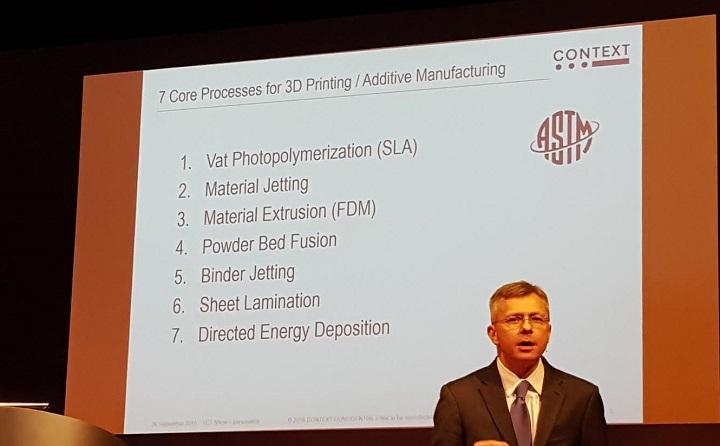

Connery began by noting that a look at the 3D printing market overall is nearly impossible, as it must be segmented. The two primary distinctive niches in the market are the desktop/personal (defined in the marketplace as sub-$5K machines) and industrial/professional. From there, another distinction that must be made follows designation by ASTM into the seven main technologies in 3D printing:

- Vat Photopolymerization (SLA

- Material Jetting

- Material Extrusion (FDM)

- Powder Bed Fusion

- Binder Jetting

- Sheet Lamination

- Directed Energy Deposition

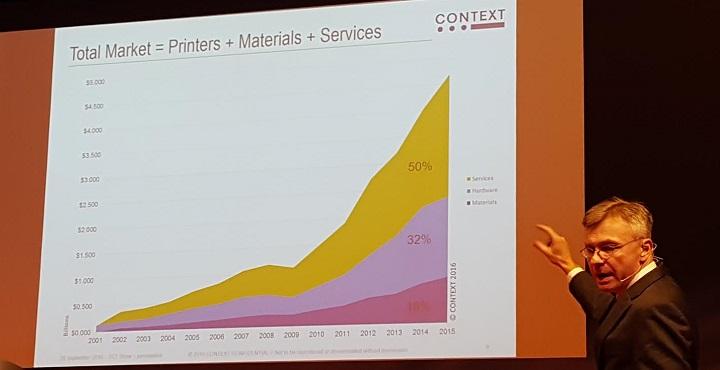

Having defined the parameters of the discussion, Connery took off into a quick recap of 2016 to date, noting that while volume shipments of 3D printers are huge in the desktop segment, obviously the higher-value industrial segment is retaining significantly higher revenues. A view of the whole 3D printing market additionally includes not only hardware, but also materials and services. Services currently account for about half of the total market value, while hardware accounts for a bit less than one-third, and materials the remaining 18% in the approximately $5-6 billion industry as it stands.

Among the major factors recently impacting the shape of the industry are management changes at some of the top companies (as we’ve seen at Stratasys and 3D Systems in particular lately); new entrances to the market (HP’s forthcoming entry) and new machines shipping (e.g., from RICOH in Q2); new materials and new technologies (e.g., RICOH, Carbon). Additionally included in the executive summary of the presentation was a note that while the total market is up (3% in revenue terms), this is due largely to desktop (up 14% in volume terms) and metal 3D printing technologies, while the industrial market overall has been a bit down (12% in volume terms).

Among the major factors recently impacting the shape of the industry are management changes at some of the top companies (as we’ve seen at Stratasys and 3D Systems in particular lately); new entrances to the market (HP’s forthcoming entry) and new machines shipping (e.g., from RICOH in Q2); new materials and new technologies (e.g., RICOH, Carbon). Additionally included in the executive summary of the presentation was a note that while the total market is up (3% in revenue terms), this is due largely to desktop (up 14% in volume terms) and metal 3D printing technologies, while the industrial market overall has been a bit down (12% in volume terms).

One of the interesting aspects of Connery’s talk boiled down to one point that he made while discussing the desktop/personal 3D printer segment of the market:

One of the interesting aspects of Connery’s talk boiled down to one point that he made while discussing the desktop/personal 3D printer segment of the market:

“People have to learn [3D printing] somewhere, they’re going to learn on a $500 machine, not a $50,000 machine. We’re very bullish on the desktop market.”

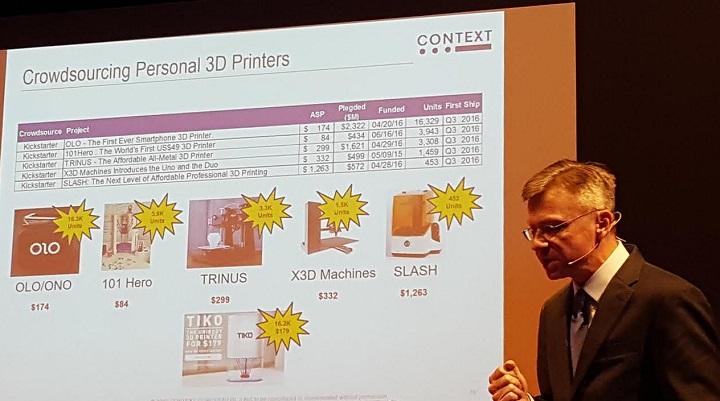

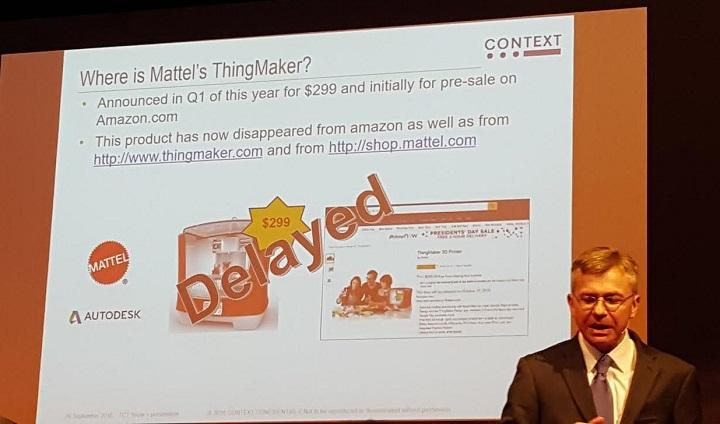

Hearing a positive forecast for the potential in desktop 3D printing is an interesting take on an industry that has overall seemed to be stepping away from smaller machines — though certainly not entirely. With 3DS’ exit of the desktop market last year and MakerBot’s recent move away from consumer-focused 3D printing, some of the biggest names established so far have been signaling an end to the consumer-focused desktop era. Still, there is certainly a huge potential market for desktop machines, even if it doesn’t come from home users. Classrooms, small businesses, medical offices, and more are still leaning heavily on these smaller, entry-level machines. Additionally, Kickstarter remains a major point of entry for new businesses — and, as Connery pointed out, as a portal for established businesses as well to introduce new products. The community aspect of 3D printing remains a primary factor in its growth, as much of the desktop industry has indeed been crowdsourced, via both crowdfunding platforms and open source movements like RepRap. There remain certain curiosities of course, like the delayed release of Mattel’s low-cost ThingMaker 3D printer for kids. So far as market share goes, XYZprinting remains the leader by unit sales in the desktop space.

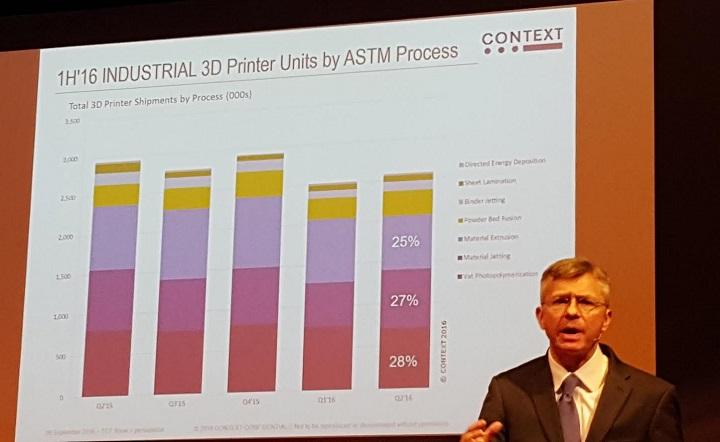

On the industrial side of the market, Connery noted that segmentation via ASTM process is much more apparent. We are seeing a rise lately in powder bed technologies as metal additive manufacturing raises its profile in the industry, offering a growing impact in revenue terms. Leadership in the industrial market is also somewhat more apparent in value terms, with Stratasys holding a 36% market share with $208 million in revenues. GE’s recent high-profile move to acquire two major 3D printing companies additionally highlights an important note on this market, as Connery stated of GE’s $1.4 billion investment:

“They’re bullish. We’re bullish.”

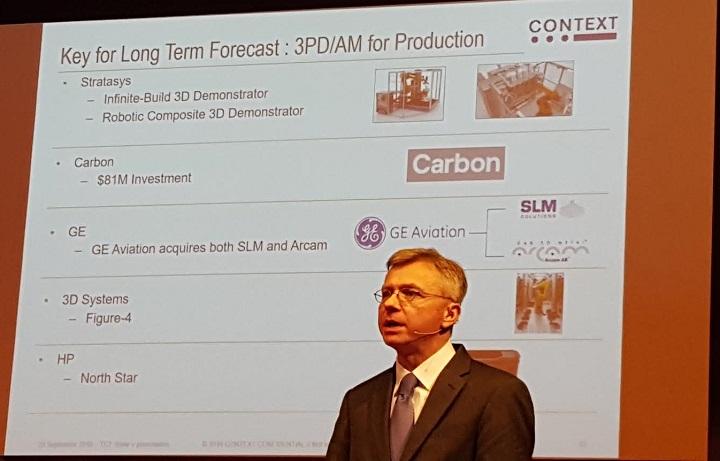

A major trend we’ve seen reverberating lately additionally provides more fuel to this bullish flame, as more companies move toward actual production-quality techniques and away from using AM only prototyping. While prototyping will of course remain a huge application for additive manufacturing, Connery noted as key to the fast-rising market forecast:

“Finally having that ‘M’ in ‘AM’, the manufacturing, is coming in to play.”

This production-quality AM reflects not only the leaps in metals, but is especially apparent, Connery noted, in plastics. With companies like 3D Systems, Stratasys and Carbon looking toward actual manufacturing with plastics, this growing trend serves to underscore CONTEXT’s findings and provide a solid basis from which to see impressive annual gains.

Overall, the 3D printing market remains a bastion of incredible potential — and more than that, we’re beginning to truly see some of this potential realized as more companies enter the scene with the latest in materials, applications, and successful funding rounds (and acquisitions) representing the future course of additive technologies. Discuss further over in the CONTEXT 3D Printing Projections forum at 3DPB.com.

[Images: Sarah Goehrke for 3DPrint.com — all data from CONTEXT as presented at TCT Show]

[Images: Sarah Goehrke for 3DPrint.com — all data from CONTEXT as presented at TCT Show]

Subscribe to Our Email Newsletter

Stay up-to-date on all the latest news from the 3D printing industry and receive information and offers from third party vendors.

Print Services

Upload your 3D Models and get them printed quickly and efficiently.

You May Also Like

3D Printing Financials: 3D Systems Returns to Growth in Q1 2026

3D Systems (NYSE: DDD) reported one of its strongest quarters in recent years, showing signs that the company may finally be moving past the tough slowdown that has weighed on...

3D People Case Study Details Development of 3D Printed POV Camera Rig

A POV, or Point of View, camera rig, is a wearable support system that helps filmographers capture first-person footage, making the images more immersive. Some good examples of movies shot...

3D Printing News Briefs, May 2, 2026: Soft Robots, Agricultural Waste, & More

In this weekend’s 3D Printing News Briefs, we’ll start off with a multi-laser metal powder bed fusion 3D printer and post-processing news. We’ll end with research into soft robotics and...

Industrial Applications on Display at RAPID 2026: CERATIZIT & 3D Systems

Applications are where it’s at in the additive manufacturing (AM) industry. At the recent RAPID+TCT in Boston, I met with a few companies to learn about some of their very...