3D Printing’s Real Money

A few weeks ago, I spoke at the National Retail Federation’s Shop.org Digital Summit on the topic of 3D printing at retail. I really hope I made the case for 3D printing’s disruptive potential.

A few weeks ago, I spoke at the National Retail Federation’s Shop.org Digital Summit on the topic of 3D printing at retail. I really hope I made the case for 3D printing’s disruptive potential.

3D printing and other digital manufacturing technologies are getting better, faster and cheaper, and soon this is going to have a big impact on the way consumer products are manufactured and sold.

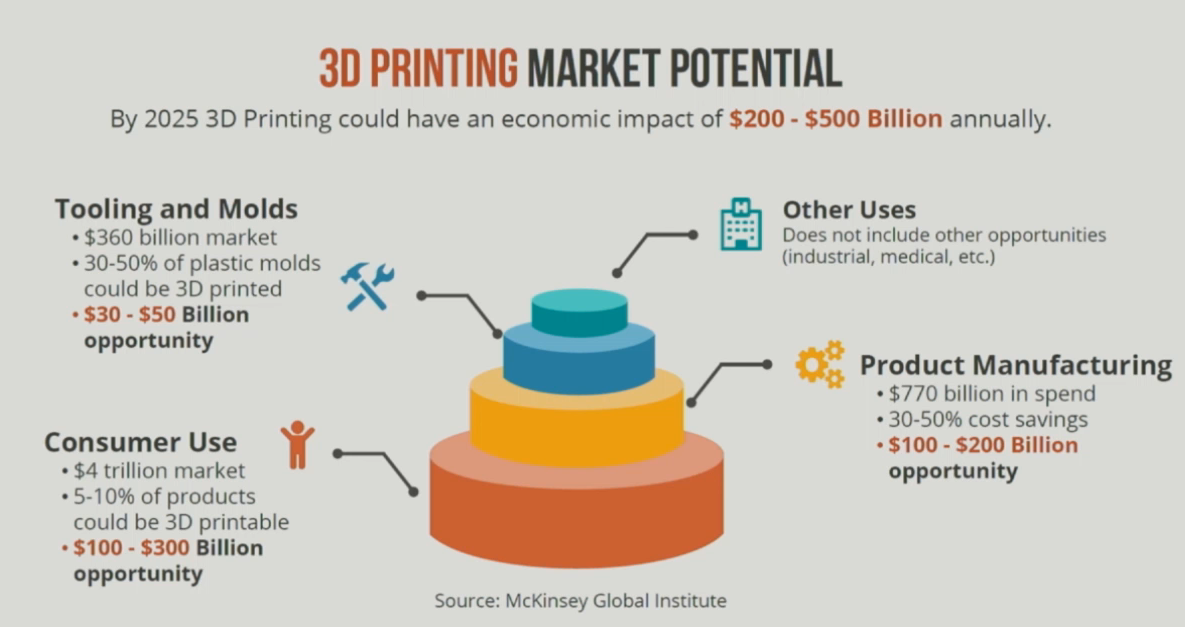

McKinsey recently published a report which predicted that 3D printing could have an economic impact of up to $550 billion by 2025. The majority of that was attributed to digital manufacturing and consumer use of 3D printing. In fact, they suggested that as much as 5-10% of consumer products could be “printable” by then.

The author during his presentation at the Digital Summit

As I said in my presentation, if you believe that 3D printing will have a significant impact on how things are invented, made and sold, the next questions you have to ask are “where” and “by whom?”

I also said that I don’t believe the majority of 3D printing will happen in the home. If it turns out like 2D printing has, less than 10% will happen there. The vast majority of 3D printed things will be made by someone else – for pay.

Who better to support that need than retailers? They’ve got product expertise. They stock and sell the mass produced products we all use every day. And in most cases, they also own the relationship with the customer…for now.

One of the questions during our panel session asked for a prediction both in 2016 and 2020. Here’s my answer. I said that 2016 would be the year of 3D printing equipment. A lot of well known companies are entering the market. HP, Mimaki, and Mutoh have all thrown their hat in the ring. A few weeks ago, Canon announced its new 3D printer concept and just last week, Ricoh pulled the sheet off theirs – stating in their press release that order taking would begin nearly immediately.

By the way, last year I wrote two articles offering predictions for 2015. One was a satirical “top 10” list. I’m frankly shocked at how many of those have come at least partially true. The other was more serious. In it, I said 2015 would be the year of workflow. We’ve still got a couple months left, but the 3MF Consortium launched by HP, Autodesk, Microsoft and others has to be one of the biggest stories of 2015. The consortium’s goal is to create a universal file format for 3D printing. It’s a workflow play. Call me Nostradamus.

What about 2020? I said it would be the year of “real money.” The year when 3D printing has a big enough economic impact to become visible to the bean counters. In retail, that could either be cause for celebration or serious anxiety.

Big Opportunity

If McKinsey is right, by 2025 a giant, mature ecosystem will need to be in place. It’s fertile ground for retailers and their suppliers, but not for long. Upstarts and outsiders are at the gates. Even the United States Postal Service seems poised to play.

Right now, companies should be thinking about what parts of the 3D printing ecosystem they need to own. The customer? The products? The network?

Who Owns the Customer?

Today, it’s undoubtedly retail. Something like 75% of all consumer goods are still purchased in-store. But that’s changing. eCommerce is growing at 15%+ every year. That new channel has allowed brands to sell direct, in addition to creating opportunities with online-only retailers.

But, even eCommerce is ripe for innovation. A recent AdAge article discussed the rise of retail digital exchanges. Several large retailers are building their own digital advertising networks. Their value is in the information they collect about our purchasing behavior, which allows ads to be more targeted and thus, more effective. And they have the data to prove it.

This creates some challenges for brands. First, they’re giving more of their advertising budget to specific retailers. That’s more eggs in fewer baskets. But accounting for it is an even bigger problem. Brands have two piles of money. Marketing, which pays for mass and other digital advertising, and trade promotions, which pays for retailer specific stuff. Which bucket should these new investments come from?

Trade promotions is the likely answer. And if so, that means those brands will have less to spend on in-store activities. Who fills the gap? Smaller brands? Private label? Do stores just become “white space?”

Certain locations of The UPS Store offer 3D printing services [Photo: John Hauer]

Who Owns the Content?

You could make an argument that brands are losing this battle. Private labeling is big business. Brands spend upwards of 25% of their revenue marketing their product. Private labels succeed because they pass some of those savings on.

But, what if a brand didn’t have to supply and stock product at all of those retail stores? What if products were like songs or movies – stored on a server and only delivered once a purchase was made?

It’s a SWOT analysis waiting to happen for nearly everyone in the consumer products value chain. Brand value is certainly a strength. Which would you be more likely to trust, a 3D printed product from a well-known brand, or a generic version?

Who Owns the Network?

What happens when manufacturing goes digital? It’s not that hard to imagine a world with a 3D printer in every store…or one in every aisle for that matter.

Who owns that infrastructure? The knee-jerk is to say the retailer. But here’s why that’s unlikely. Very few are willing to make the investment on their own, especially in physical stores.

You’ve heard of the store-within-a-store (SWAS) concept, right? It’s when a brand sets up a dedicated space within a big box store. Consumer products companies like Samsung and Adidas, and even retailers like The Finish Line, have used this tactic successfully.

Who paid to develop out Samsung’s SWAS concept? I’m guessing it wasn’t Best Buy.

3D printing is different. Most stores-within-stores are brand-specific, or offer a very niche selection of product. But what if the store offered thousands of products in nearly every product category? Wouldn’t that be a bit more strategic? You’d think.

Content + Network = Customer

In a digital model, the companies that own the content and own the network can also own the customer. They have the data, and paraphrasing the pitch used by retail exchange networks, “they that own the data, own the customer.”

Future Success is Being Determined Now

Future Success is Being Determined Now

If I’m right and 2020 is the year of “real money” in 3D printing and if McKinsey is right and that by 2025, 5-10% all consumer products are 3D printable, a bunch of work needs to be done.

Someone will need to invest in developing the content and developing the network. And it will cost millions.

But, someone will do it. Too many big players are flooding into the market. Google just invested $100 million in Carbon3D. GE, Bosch, Alcoa and Michelin, just to name a few, have also made big investments in 3D printing.

None of them have their eyes set on retail, right? Wrong. The lines between manufacturing and retail are quickly blurring. Just recently, Bridgestone announced the acquisition of Pep Boys for $835 million.

Imagine 10 years from now. Would you really be surprised if by then, Bridgestone was the leader in 3D printed consumer products? They have product expertise in multiple categories (automotive, sporting goods, etc.), and with Pep Boys, they now have a network of over 3,000 stores. They definitely own their customer.

But would they make the investment? I’m guessing that depends on the return. Let’s say the market for 3D printed consumer products is worth $50 billion by 2025. Automotive will account for a significant piece of the pie. I know it’s cliche, but if Bridgestone captured just 1% of the total market, they could generate an incremental $500 million in annual sales.

No matter how you look at it, that’s “real money.”

John Hauer is the co-Founder and CEO of 3DLT, a platform for 3D Printing As-a-Service. The company works with retailers and their suppliers, helping them leverage 3D printing online and in-store. John also recently founded and manages Get3DSmart, a consulting practice which works with large companies, helping them understand and capitalize on opportunities with 3D printing.

John’s original content has been featured on TechCrunch, QZ.com, Techfaster.com, 3DPrint.com and Inside3DP.com, among others. Follow him on Twitter at @3DLTJohn

Subscribe to Our Email Newsletter

Stay up-to-date on all the latest news from the 3D printing industry and receive information and offers from third party vendors.

Print Services

Upload your 3D Models and get them printed quickly and efficiently.

You May Also Like

AM Asia Watch: Chinese Company Claims Advances in Titanium Powder Beyond 700C

They’re a familiar sight at trade shows: Chinese powder companies with barren stands lacking parts. There’s maybe some glass vessel with powder in it and a semi-complete data sheet, but...

Aires Tide Designed with AI, Supercomputers, and 3D Printing

The Department of Energy‘s National Nuclear Security Administration (DOE/NNSA) is part of the US government that manages the US nuclear stockpile, helping to upgrade, improve, and maintain nuclear weapons, and...

Largest Publicly Announced, Single Order in EOS History: Beehive Industries Spends $50M on M4 ONYX 3D Printers

Earlier this year, Beehive Industries received a $29.7 million contract to produce its Frenzy 6 and Frenzy 8 engines for the US Air Force. The metal additive manufacturing (AM) user...

Blue Origin’s New Glenn Explosion Comes During Major Manufacturing Push

Blue Origin‘s orbital New Glenn rocket exploded during a hot-fire test at Launch Complex 36 in Cape Canaveral on May 29, setting back the company’s launch ambitions at a time...