Venture Capital in Additive Manufacturing

Can AM companies be true venture cases? (What) have we learned?

In the context of VC, companies are evaluated based on their “venture case” potential. Take, for instance, a EUR 100 m VC fund focused on early-stage investments. To achieve top tier performance, funds in the upper quartile target an annualized return of 20%. Over the typical 10-year lifecycle of a fund, this translates to generating a 200% profit on top of the original EUR 100 m investment. Put simply, the goal of a VC firm is to return “3x the fund”. In our example, EUR 300 m.

VC returns are not normally distributed, they follow a Power Law distribution

Illustrative example of the Power Law – Source: AM Ventures

Unlike traditional investments, VC returns follow a Power Law distribution, where a small number of investments generate the majority of returns:

- About one-third of portfolio companies fail completely. They are written off.

- Approximately 60% of companies manage only to break even. These companies return the fund once.

- A crucial less than 10% of companies achieve extraordinary returns, delivering profits exceeding 200%. These home runs drive the fund’s overall performance.

VCs that lead a funding round usually start with a 20% equity ownership. Assuming they have reserves to maintain this stake through future funding rounds, dilution typically reduces their ownership to around 10% by the time of the exit. For simplicity, we assume that early-stage venture capitalists typically build portfolios consisting of around 20 companies.

To achieve the “3x return on the fund” goal, VCs need at least two standout companies that deliver a 200% return. Each company must have the potential to deliver a return equal to 1x the fund (a so called “home run”), requiring an exit valuation where the VC’s 10% ownership aligns with this return. Therefore, startups should aim for an exit potential of 10x the fund size (e.g., EUR 1 billion for a EUR 100 million fund) to attract VC interest. This aligns with the power-law dynamics that drive venture capital success.

(Generalist) VCs Check Billion-Dollar Potential in “AM Companies”

With this simple yet often overlooked aspect of VC math, the key question for our industry is whether AM companies can be true venture case? Can AM companies demonstrate the scalability and market opportunity to align with the ambitious VC return thresholds?

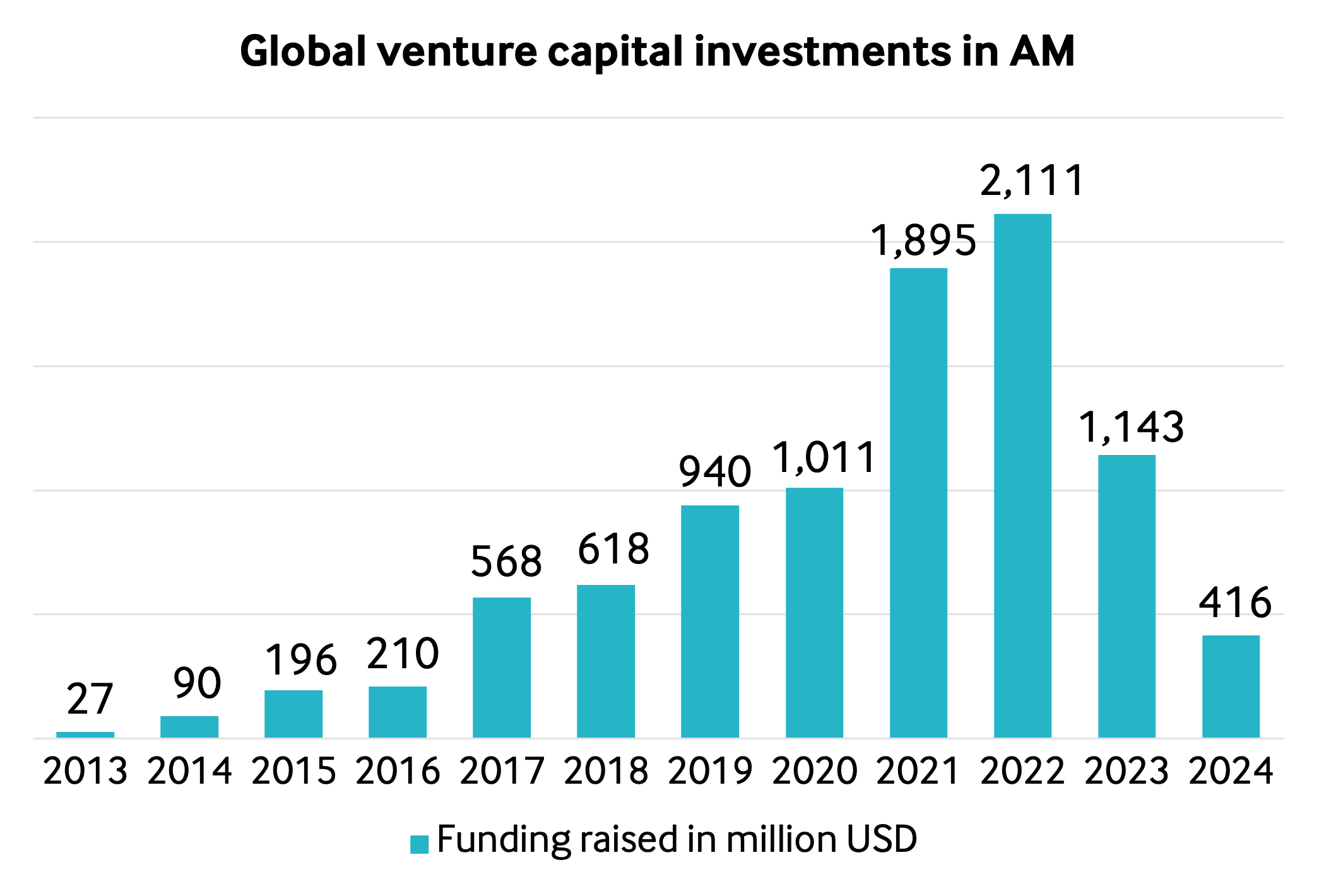

Recent market trends indicate a cooling investor sentiment towards AM. High-profile SPAC-backed companies have often failed to deliver on ambitious promises and projected business cases, leaving investors disappointed. Claims of “lights-out manufacturing at scale” for end-use parts have proven elusive, and as a result, investor appetite has notably diminished. This shift issue is underscored by the numbers. Last year, startup investments in the AM sector saw a significant decline, with only USD 416 m flowing into the industry.

Source: AM Ventures

At first glance, the “AM industry” may appear to lack standalone, billion-dollar “pure-play” companies. However, when examined through the lens of specific applications, a different narrative emerges. Companies focused on building value chains around one single application that occupy the niche and extract maximum margin are quietly thriving.

“Great technology looking for applications” or “Great applications looking for a technology”?

Historically, the “AM industry” has often found itself in the mantra: “Great technology looking for applications.” But a shift in perspective, where the focus is on “Great applications looking for a technology,” reveals a broader, more impactful story. In this framework, applications driven by real-world needs extend far beyond the additive process itself.

Consumers, patients, and industrial customers typically do not distinguish between AM and other production methods when purchasing products. This raises an important question: why do we continue to speak of an “AM industry” when advanced manufacturing requires a diverse mix of complementary technologies, materials, and processes to achieve optimal economic and technical outcomes? When end-users prioritize performance, cost, and reliability, why does the focus often remain on promoting the AM process itself, rather than the tangible outcomes it delivers or the problems it solves? The reality is that the concept of a singular “AM industry” does not fully capture the landscape. Industries such as those involved in producing aligners, heat exchangers, filtration membranes, electric motors, and medical braces are vertically integrated, with their markets triangulating in unique ways. For these sectors, AM is simply viewed as an enabling technology – nothing more, nothing less.

Whether you’re a founder, investor, or industry observer, the VC session on the first day of Additive Manufacturing Strategies (Feb 4-6, 2025 in New York City) will focus on the key developments needed in AM and offer insights into what VCs look for when deciding to invest – or hold off – for now. This is a unique opportunity to gain valuable knowledge from what we at AM Ventures have learned over the past 10 years.

Subscribe to Our Email Newsletter

Stay up-to-date on all the latest news from the 3D printing industry and receive information and offers from third party vendors.

Print Services

Upload your 3D Models and get them printed quickly and efficiently.

You May Also Like

3D Printing News Briefs, April 22, 2026: DINOs, Post-Processing, AM for Aerostructures, & More

We’ll start with event news in today’s 3D Printing News Briefs, as AMUG presented its DINO Award to six members at this year’s conference, and Axtra3D celebrated its five-year anniversary...

ExOne + voxeljet Are Trying to Do the One Thing Customers Need Right Now: Keep Machines Running, and Rebuild Confidence

For years, ExOne and voxeljet were two of the best-known names in binder jet 3D printing, especially in sand printing for foundries. But in recent years, ExOne “got buried” inside...

What the 2026 Post-Processing Survey Reveals About the Future of AM

As additive manufacturing (AM) continues its transition from prototyping to production, industry attention is shifting toward one of the most demanding but often overlooked parts of the workflow: post-processing. The...

New Shades for 3D Systems NextDent Denture Jetting

3D Systems NextDent is expanding its denture jetting portfolio. The company is adding three new shades of gum tones. That will let the solution look more natural on more patients....