Will Nikon’s SLM Solutions Deal Go through?

When Japanese multinational Nikon (TYO: 7731) announced its intention to acquire SLM Solutions (ETR: AM3D) in September 2022, it seemed like a reasonable part of its digital manufacturing strategy, and there is certainly merit in acquiring an established player in the additive manufacturing (AM) space instead of building one from the ground-up.

What was jaw dropping to many people, however, was the price tag: A whopping €622 million or €20 per share, implying a 7.6X revenue multiplier (on €81.7 revenues in 2021), on a company that has suffered from negative EBITDA for the last few years. Even in “bubble terms,” many found this to be an inflated valuation. (For comparison, Stratasys (Nasdaq: SSYS) is traded at less than a 1X revenue multiplier, while 3D Systems (NYSE: DDD) and Desktop Metal (NYSE: DM) are hovering around 2X).

Nikon’s Morf3D with an SLM Solutions NXG XII metal 3D printer. Image courtesy of SLM Solutions.

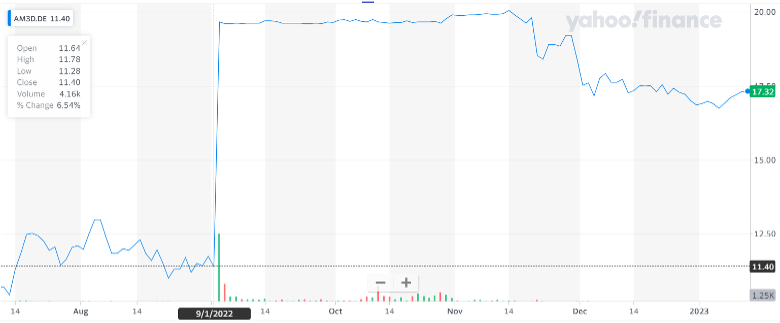

Nikon’s Morf3D with an SLM Solutions NXG XII metal 3D printer. Image courtesy of SLM Solutions.Assuming the deal closes as expected (as a reminder, the deal was announced in Sep-2022 with an expectation of closing in H1-2023), SLM shareholders will receive €20 per share in the next few months. So, with SLM trading now at €17.30 (dipping to €16.7 just a few days ago), is this an opportunity to make an “easy” 15.6% profit in just a couple of months?

Perhaps yes, and perhaps the market are telling us there is some risk to this deal. An average M&A arbitrage spread (the gap between the proposed share price and the current share price) is typically 5-10%. This reflects the fact that every deal, until it closes, has some risk (for example: regulatory approvals required for the deal not being received or force majeure events). The SLM spread seems to be reflecting a “higher than average” risk on the deal closing.

Could this spread mean investors are worried Nikon might be having second thoughts (either about the deal in general, or about the price tag)? We can’t say for sure, but it is this author’s view the risk can’t be *very* high or else we would have seen a bigger spread. On a standalone basis (that is, without the Nikon deal coming through), there is little doubt SLM’s stock will be trading at significantly lower than the current price (by benchmarking SLM vs. Stratasys, 3D Systems, Desktop Metal and other peers). Meaning, if there was a high risk to the deal coming through, we could expect an even higher spread.

And while it is safe to assume Nikon might be having second thoughts about the price tag, depending on the terms of the current bid, it might not be easy to “walk away” or re-negotiate terms (see the case of Elon Musk in his Twitter bid).

To summarize, every deal carries risk, especially in the current market conditions. That said, for the risk-loving investor, giving the SLM spread a deeper look, might be a worthwhile exercise.

Please note that the information provided in this article is for informational purposes only and should not be considered financial advice. The author is not a certified financial professional and does not hold any qualifications in this field. The author takes no responsibility for any investment decisions made by readers as a result of reading this article, and any losses incurred by readers as a result of following the information provided in this article are the responsibility of the reader. It is important to conduct your own research and consult with a qualified financial advisor before making any investment decisions.

Subscribe to Our Email Newsletter

Stay up-to-date on all the latest news from the 3D printing industry and receive information and offers from third party vendors.

Print Services

Upload your 3D Models and get them printed quickly and efficiently.

You May Also Like

Flashforge Bets on Meshy AI as Desktop 3D Printing Battle Intensifies

Competition in desktop 3D printing is brutal. Whereas before, firms competed through value engineering, Prusa clones now have an integrated hardware, sensor, and software setup that is making all the...

Ford Uses Binder Jet 3D Printing to Make Boat Propellers for Sharrow Marine

Ford’s Advanced Industrial Technology and Platforms (ATP) group has helped Sharrow Marine make a boat propeller in two weeks rather than 130 days. Thanks to the Michigan Central program, Ford...

Skuld to Work on DARPA’s Rubble to Rockets (R2R) Program

Skuld will work on the Defense Advanced Research Projects Agency’s (DARPA) Rubble to Rockets (R2R) Program, which turns scrap metal into missile components. Skuld will help with alloy design, characterization, and...

From “Magic” to Metal: How Intrepid Automation Wants to Make 3D Printing Matter at Scale

Ben Wynne still talks about 3D printing the way people do when they’ve felt that “wow” moment up close. Back in the early 2000s, he was working at HP’s advanced...