2023 3D Printing Predictions: The Financial Landscape

All the speculation about a potential recession in the volatile market of 2022 led many investors to preserve their wealth against heightened inflation, rising interest rates, and receding economic growth. As a result, the last month of the year witnessed stock market indexes S&P 500, Dow Jones Industrial Average, and the Nasdaq Composite Index shed points, ending in red, as the challenges of 2022 show no signs of slowing down as we enter 2023.

Following a year of aggressive monetary tightening by the Federal Reserve, inflation in the US slowed down towards the end of 2022, falling for the fifth consecutive month to 7.1% in November, down from 7.7% in October. In response, the Central Bank has raised interest rates and has been forced to move forward with interest rate rises in 2023 to get closer to its anticipated target inflation of 2%.

Despite the Fed’s latest economic projections showing growth at a pace of 0.5% in 2023 and words from Chairman Jerome Powell firmly committing to “bringing inflation back down to our 2 percent goal” and assuring reporters during a press conference on December 13 that “it’s not knowable” that the US will have a recession, reports from major investment management companies and universities are inclining otherwise.

Namely, BlackRock said, “recession is foretold as central banks race to tame inflation.” Similarly, JP Morgan predicts a recession for 2023 even as inflation pressures ease at the end of 2022. Indiana University’s Kelley School of Business stated that concerns about a recession are real, with inflation at a 40-year high and an economy growing sluggishly. Outside of the US, the European Commission’s autumn economic forecast states the eurozone and most EU countries were already headed to an economic recession in the last quarter of 2022.

AM financials

Bryan Dow

Bryan DowWe talked to Bryan Dow and Stephen Butkow from Stifel, the seventh-largest investment firm in the US, to try to understand the financial landscape ahead and what it holds for the additive manufacturing industry in 2023.

According to Dow, 2022 has been a year of “high highs and low lows.” After several years of continual growth, he says the macro headwinds have proven challenging, pivoting CEOs and investors to focus on near-term profitability.

“While the long-term secular trend has been on-shoring, the manufacturing sector is focused on right sizing for the current economic environment. In the deal markets, the amount of private capital being deployed into Digital Manufacturing businesses was actually up 52% year-over-year, while both public equity issuance and M&A [mergers and acquisitions] volumes declined dramatically, down 85% and 65%, respectively,” pointed out Dow.

Butkow stressed that in 2023, he expects to see a continued tightening of central bank monetary policy resulting in even higher interest rates, plus the negative impacts of the war in Ukraine, which will all contribute to a slowing global economy. He advises that these macro factors will continue to cause headwinds on financial results and valuations across all sectors of the economy and stresses that there will continue to be volatility across all markets until there is a “clearer picture” of when central banks will taper their all-out offensive on eliminating persistent inflation.

The financial expert also highlighted that balance sheets across the digital manufacturing landscape are relatively healthy. However, as the more prolonged macro event-driven volatility persists, 2023 will likely be a year that is increasingly more focused on streamlining operations instead of growing them.

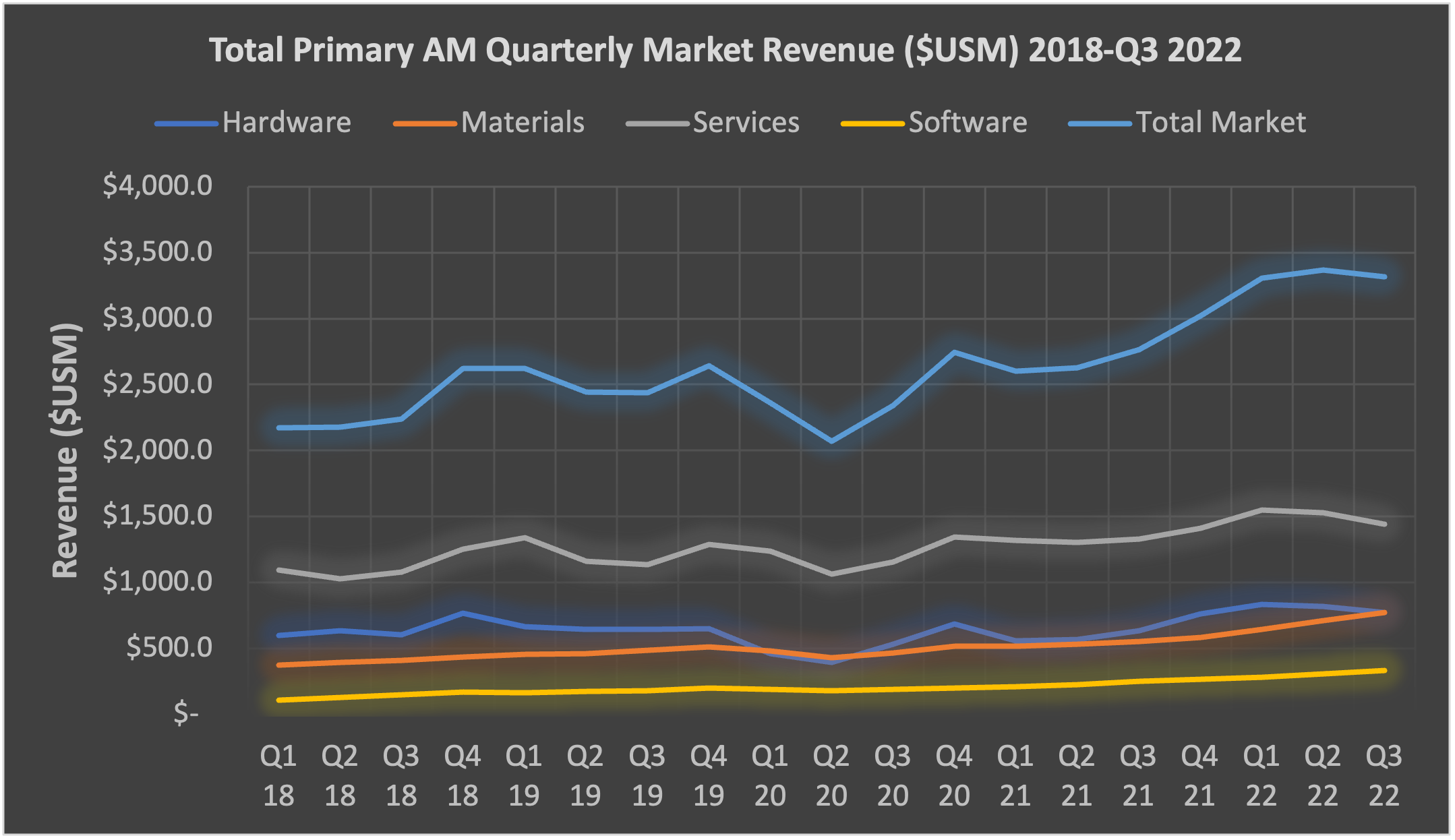

SmarTech Analysis also suggests that the AM industry’s current quarterly run rate of revenues is healthy. It anticipates that this tendency will be sustained throughout the following year. However, it also expects that the prior strong growth in the industry exiting the pandemic era and continuing to ride the “supply chain relief” wave may diminish in 2023.

As assessed by the market research firm, since the fourth quarter of 2021, the AM market has grown notably on a quarterly revenue basis, which has remained between $2.4 billion and $2.7 billion. Moreover, beginning in the fourth quarter of 2021 and throughout the third quarter of 2022, the market has consistently maintained quarterly revenues of between $3 billion and $3.3 billion, despite many providers indicating changes in customer order timing in the third quarter of 2022.

From the Q3 2022 Metal Market Data and Q3 2022 Polymer Market Data. Image courtesy of SmarTech Analysis.

From the Q3 2022 Metal Market Data and Q3 2022 Polymer Market Data. Image courtesy of SmarTech Analysis.Overall, the 3D printing industry analyst group says specific end markets will see a continued downturn, some of which will be materially impactful to the additive industry, particularly medical and general industries, with consumer goods and dentistry being close seconds. Meanwhile, automotive, energy, aerospace, and defense all appear likely to continue to thrive in the short term.

Additionally, SmarTech believes that since sentiment is already relatively high on AM from the past two years, there is likely to be a canceling effect between impacted end markets versus those poised to keep growing. Moreover, it estimates that those markets in the latter category have more than enough potential to sustain the current industry run rates. The coming quarters will see the strong growth trend continue.

Deals & more

As for the private equity outlook, 2022 wasn’t exactly a top year for initial public offerings (IPOs) in general; this effect has also trickled down to the AM industry. According to Stifel’s Equity Capital Markets team, after a robust 2021 of 19 public equity deals in the digital manufacturing sector, there hasn’t been a single traditional IPO and only a few converts, all of which happened in the first half of 2022. Following this trend, the team expects the IPO market will remain highly selective in the near term, with institutional investors tending to be largely risk-off and are more focused on positive earnings and cash generation top-line growth.

Also falling from the record 2021 period were US special acquisition deals (SPACs). In 2021, SPACs had raised capital in 613 IPOs in that year alone, but by November 2022, SPAC activity slowed down to just 129. The aggregate value of those deals was $8.02 billion, compared with $38.73 billion in the same period a year ago. This tendency could showcase what lies ahead for 2023 in terms of SPACs.

In the private markets, Dow says that while there remains significant dry powder at venture funds, with the recent mark-to-market of portfolios, valuations have been “squeezed in new rounds across the board,” and “the bar has risen dramatically in terms of quality requirements.” For example, in digital manufacturing, there was a 52% uptick in private capital raised year-over-year to over $1.5 billion.

“In 2022, VCs have taken a barbell approach to the market, focusing on early-stage and late-stage business. Of the 32 deals, half of the rounds were under $10 million, while six were over $100 million. We expect that to continue to be the investment policy in 2023, as well,” went on the executive.

Stephen Butkow

Stephen ButkowAccording to Stifel’s M&A team, significant capital remains on the sidelines that must be deployed, providing optimism for a constructive back half of 2023. However, for digital manufacturing alone, Butkow explains that the vast majority of M&A deals in 2022 involved profitable companies, a tendency Stifel doesn’t see changing in 2023.

“Private equity remains an important category of buyers in digital manufacturing as the sponsor community represented 44% of deals in 2022 compared to 25% in 2021,” explains Butkow. “In addition, with public valuations at current levels, we could see significant consolidation with a goal to achieve scale and realize synergies.”

Finally, SmarTech Analysis ends the year on a positive note, with solid optimism around future business and the long-term health of the 3D printing market, perceiving that there is no evidence, seen explicitly in financial communities, to suggest concretely that there will be a substantial downturn in AM.

Despite macroeconomic headwinds and the ripple effects of global bottlenecks like ongoing supply chain disruptions, experts believe there is still robust demand for AM, especially as the technology progresses and evolves in end-use part production, new materials, and workflow software.

To learn more about finance in 3D printing, register here for the Additive Manufacturing Strategies business summit in New York City, February 7-9, 2023, hosted by 3DPrint.com and SmarTech Analysis. Stifel’s Stephen Butkow and Bryan Dow will participate in special presentation panels. Register for the event here to learn from and network with the most exciting companies and individuals in AM.

Subscribe to Our Email Newsletter

Stay up-to-date on all the latest news from the 3D printing industry and receive information and offers from third party vendors.

Print Services

Upload your 3D Models and get them printed quickly and efficiently.

You May Also Like

3DPOD 302: Digital Inventory for AM with Mikhail Gladkikh, Würth Additive Group

Mikhail Gladkikh has worked in oil and gas for many years. With this background, we obviously talk about energy market turbulence and the adoption of AM in oil and gas....

Spectrum Filaments Gets Investment: How They Could Win in Filament

Spectrum Filaments is a long-time high-quality filament supplier based in Poland. With good tolerances, roundness, and consistency coupled with affordable pricing, the firm has been a mainstay for makers, industrial...

NX Atomics and Sciaky Collaborating to 3D Print Nuclear Components

For decades, the nuclear industry has quietly experimented with and implemented additive. Bouyed by the likes of ORNL, companies such as Westinghouse have 3D printed components serially. We have an...

Incodema3D Buys 14 Metal EOS Systems, Now One of the World’s Largest Metal 3D Printer Operators

Recently, a majority stake of 3D printing service bureau Incodema3D was purchased by AFM Capital. Under new ownership, the Freeville, New York company is now using its cash-rich parent for...