The 3D Printing Industry is Here to Stay – A Look at Investment Activity and M&A

As investment bankers who have worked within the industrial technology sector for over 20 years, we wanted to address what we are seeing in the 3D printing value chain of machines, digital manufacturers, materials providers, resellers, and software providers, or more simply, the 3D Printing Industry. Throughout our time working in this space, the 3D Printing Industry has continually evolved, attracted significant investment activity, and is showing signs of some early consolidation.

The 3D Printing Industry has been funded predominantly by the private capital markets as opposed to public markets. Since 2015, there have been nearly 80 private funding rounds per year. In 2019 the sector continued to witness robust venture capital activity, especially in digital manufacturing. Four leading digital manufacturers (3DHubs, Fast Radius, Fictiv, and Xometry) raised nearly $150 million, by far the most venture interest in this business model. 3D printer Original Equipment Manufacturers (OEMs) continue to dominate the venture capital inflow with the $1 billion plus valuation “unicorns” (Carbon, Desktop Metal, and Formlabs) each tapping the private markets in 2019. There continues to be a strong constituency of venture capital firms that have an executable investment thesis in the sector, but, at Stifel, we are seeing a dramatic increase in corporate venture capital pouring into the sector. Materials companies (Arkema, BASF, DSM, and Henkel) have been the most active group investing in six companies, but other interesting strategics such as Koch (in Desktop Metal), UPS (in Fast Radius), Intel (in Fictiv), Bosch (in Xometry) have made significant investments. This phenomenon is playing out across the ecosystem and we expect this trend to continue.

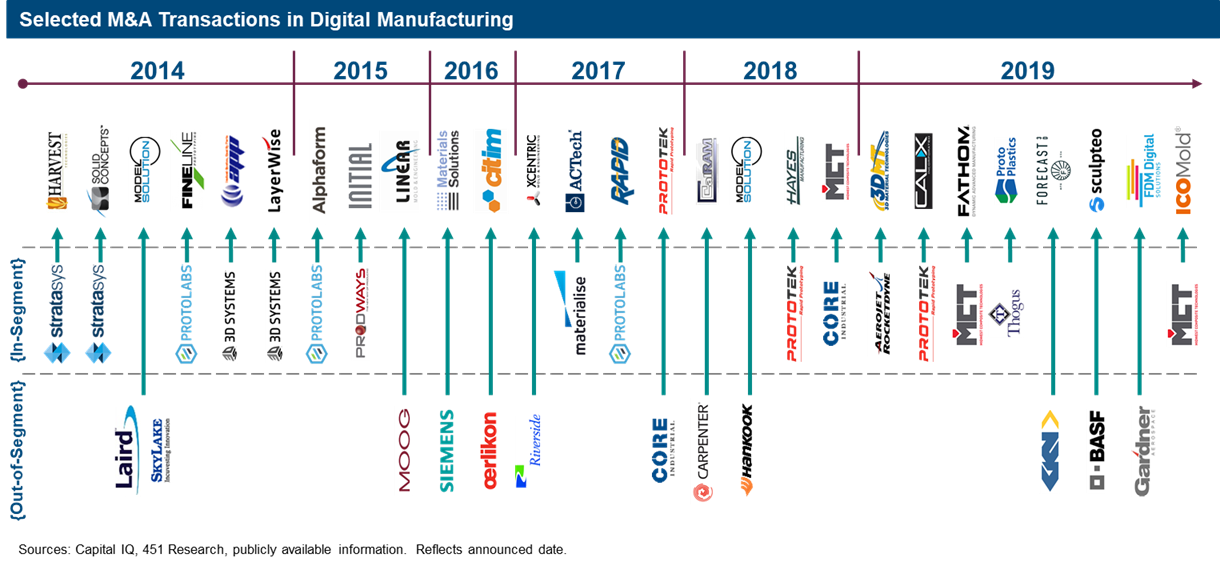

Historically, M&A activity within the sector has averaged roughly 25 to 30 transactions per year and has been spread across the value chain from materials, machines, digital manufacturers, and resellers. Activity within the 3D Printing Industry has been driven by a variety of factors, including continuing maturity in the sector, advent of new technologies, robust economic environment and increasing sophistication, and appetite from the strategic and financial community. M&A activity in 2019 remained strong across the board with digital manufacturers and Solidworks resellers leading the charge.

In digital manufacturing, M&A activity over the past five years has ebbed and flowed, culminating to a record level in 2019. At Stifel we advised on three of these recent transactions (FATHOM, FORECAST 3D, and ICOMold) as private equity (CORE Industrial Partners with FATHOM and ICOMold) continues to show interest in the business models and profitability profiles. The trend continues with “out-of-segment” strategic companies, defined as those that are acquiring entry into the sector, looking to build out and expand their presence as part of their broader industrial capabilities (GKN acquiring FORECAST 3D, and BASF acquiring Sculpteo).

The other major area of activity in this space is consolidation. The SOLIDWORKS reseller channel is now dominated by four major players (Computer Aided Technology, GoEngineer, Hawk Ridge, and Trimech), three of which have private equity ownership. At Stifel, we advised The Riverside Company on its sale of Fisher Unitech to Computer Aided Technology, which was previously acquired by CIVC Partners. Shortly after this, Trimech was acquired by The Halifax Group. Over the next few years we expect to see not only the continued consolidation of smaller regional channel partners, but also expansion into new product categories and service offerings by the larger players.

The COVID-19 pandemic has slowed down deal activity in the first half of 2020; however, capital raising and M&A activity has shown some resilience. Velo3D raised $40 million in a Series D, Nano Dimension raised almost $50 million in two transactions, DSM is acquiring Clariant’s 3D printing business, and Made in Space was acquired by Redwire, a platform funded by Private Equity firm, AE Industrial Partners.

As the pandemic lags on, the 3D Printing Industry has demonstrated the value and need for solutions to provide supply-chain flexibility and nimbleness. The digital manufacturing segment highlighted this need by providing Personal Protective Equipment (PPE) with on-demand manufacturing, which solved material challenges with the traditional healthcare supply-chain. We expect the industry landscape to continue to be dynamic as the impacts of COVID-19 become more tangible. We expect the industry landscape to continue to be dynamic as new leadership at many of the leading 3D printing companies (3D Systems, GE Additive, HP, and Stratasys) put forth their vision for the future and the impacts of COVID-19 become more tangible.

It has been exciting to be a part of the sector helping founders, executives, and shareholders execute their strategic objectives and capital needs over the past decade. Stifel looks forward to continuing our lead as the provider of investment banking services to the 3D Printing Industry.

For additional information, you can also check out our recently published market monitor on the sector here.

Bryan Dow and Stephen Butkow are Managing Directors at Stifel, a leading, full-service investment banking and wealth management firm providing investment banking, brokerage, trading, investment advisory, and related services to individual investors, institutions, corporations, and municipalities. .

Subscribe to Our Email Newsletter

Stay up-to-date on all the latest news from the 3D printing industry and receive information and offers from third party vendors.

Print Services

Upload your 3D Models and get them printed quickly and efficiently.

You May Also Like

RAPID 2026 in Pictures: The Coolest & Craziest Things on the Show Floor

Last week, North America’s premier 3D printing trade show, RAPID+TCT 2026, came to Boston. I spent two days trekking the show floor, trying to see as much as I could,...

ExOne Cuts Costs for U.S. Customers as Printhead Production Moves to Detroit

ExOne Global Holdings, created through the 2025 integration of ExOne and voxeljet, is making changes across its U.S. operations. These include starting printhead manufacturing in the Detroit area and lowering...

Euler Viewer for Metal LPBF 3D Printing Released

Icelandic software startup Euler has released Euler Viewer, a real time build viewer for metal LPBF. The product does not need to be installed, and doesn’t require hardware to be...

3D Printing News Briefs, April 11, 2026: Energy Targets, DoW Contracts, Nike Air Max, & More

We’re starting with 3D printing for energy applications in this weekend’s 3D Printing News Briefs, and then moving on to military and defense 3D printing. Finally, Nike Sportswear is focusing...