New SmarTech Report: AM Service Bureaus to Support Reshoring and Supply Chain Recovery

SmarTech Analysis has published a new report on the state of metal 3D printing service bureaus dubbed “The Market for Metal Additive Manufacturing Services: 2020-2029.” The report illustrates the current picture of the metal additive manufacturing (AM) service market and projects the future revenue opportunities that will emerge by relying on a robust set of quantitative data. Though the report provides a comprehensive look at the industry, it is being framed as particularly valuable given the major disruptions that the COVID-19 outbreak has had on the global supply chain.

Nearly all products are made in a centralized manner, with individual components made in one set of factories and shipped to others to be assembled. As nations have shut down their borders in order to limit the spread of the highly contagious coronavirus, starting with China, the globalized economy was quickly disrupted. 94 percent Fortune 1000 companies were reported as seeing their supply chains impacted in response to the pandemic, just as it was reaching its peak impact in China.

At the same time, the need to ramp up production of medical supplies to meet the needs of hospitals on the front lines has seen AM companies and individual hobbyists lend their rapid manufacturing expertise and hardware to provide the necessary items, particularly face shields, but also nasal swabs, ventilator parts and face masks. Though these are stopgap measures as companies ramp up traditional mass manufacturing of needed medical goods, the current situation demonstrates the value of AM to overcome supply chain disruptions.

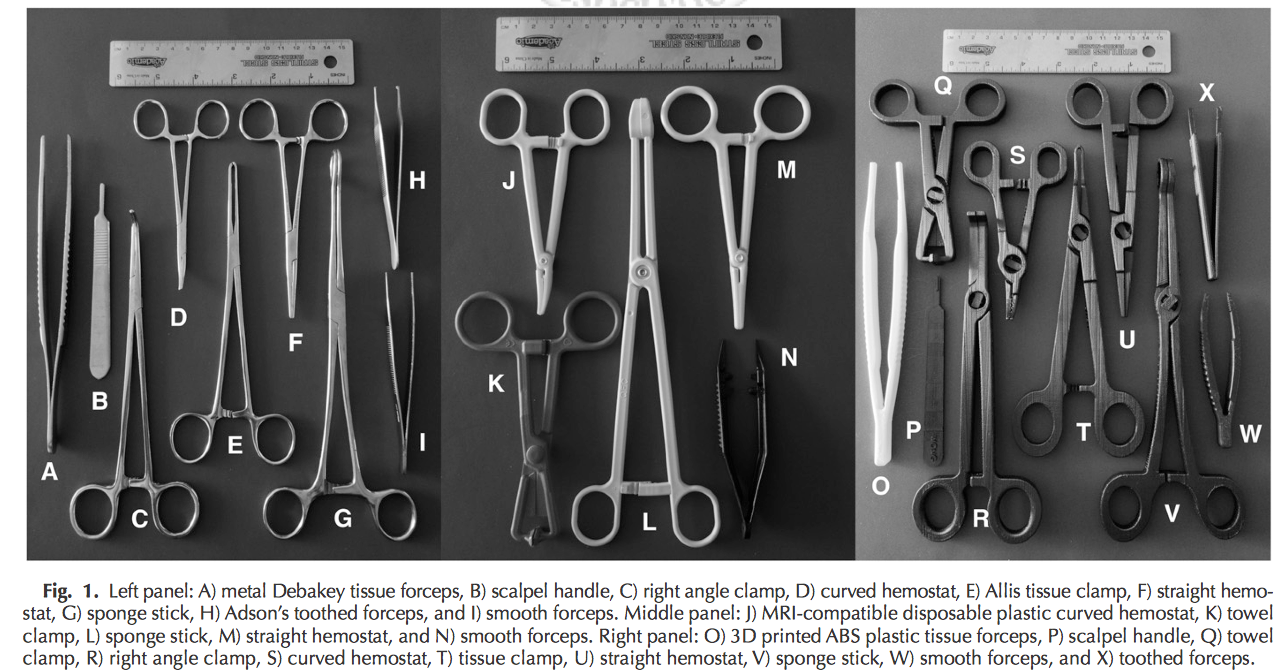

An exhibit from a study looking at the viability of 3D-printed metal medical tools. Image courtesy of the journal Aviation, Space, and Environmental Medicine.

Metal AM service bureaus may be among the best primed to take advantage of such situations, given the fact that they produce a wide variety of parts for a variety of applications around the world. SmarTech suggests that these bureaus will solve short-term disruptions during the pandemic and will also become possible solutions for re-shoring production away from distant sources of cheap labor, such as Asia.

The company is modifying its projections for this report, due to the impact that the virus has had on the global economy, as well as the larger manufacturing and AM industries. Customers who purchase the report will receive updated forecasting issued in June 2020 that take these disruptions into account.

Before the pandemic, however, the AM market analysis firm projected that the metal service bureau segment was on course to purchase almost 500 metal 3D printers in 2020 and double that number by 2023. Though the numbers are expected to change to some degree, SmarTech believes that materials demand within the service bureau segment will continue to remain strong. An important factor to take into account, particularly given the nature of the current disruption, is the fact that the medical sector is the fastest growing market for metal AM service bureaus. Despite the attention that industrial applications receive, the medical sector was projected to account for $1.5 billion in AM services by 2025.

Metal 3D printed parts with automated support structure generation from Materialise. Image courtesy of Materialise.

The report is a follow-on to the company’s 2019 analysis of the sector and includes a larger number of services and provides profiles of leading AM metal service companies. These firms don’t represent only an expansion of the market, but also differentiation within metal AM services (e.g., copper-specific 3D printing providers versus directed energy deposition, etc.). Firms discussed in the report include: 3D Systems, BeamIT, Burloak Technologies, Carpenter, DM3D, ExOne, FIT, GE Additive, Henkel, Hoganas, HP, i3DMFG, Metal Point Advanced Manufacturing, Materialise, MTI, Oerlikon, Protolabs, Renishaw, Sculpteo, Shining3D, Sintavia, Siemens, Solid Concepts, Stratasys, Thyssenkrupp, voestalpine, Wipro 3D, 3D Hubs, Hitch3DPrint and Xometry.

In addition to ten-year forecasts of the industry and its various sub-sectors, the report also includes a new end-user industry, consumer products, in its analysis and five additional service provider company profiles. It also examines the impact of service bureaus on AM’s shift into an industrial manufacturing technology. The report and a table of contents can be found at the SmarTech website here.

Subscribe to Our Email Newsletter

Stay up-to-date on all the latest news from the 3D printing industry and receive information and offers from third party vendors.

Print Services

Upload your 3D Models and get them printed quickly and efficiently.

You May Also Like

Australia’s AMCRC Funds Titanium 3D Printing R&D

In terms of the global economy’s presently existing state, there is no realistic path to economic resilience that doesn’t start with critical minerals security. This is a problem for pretty...

3DPOD 305: Automating AM with Grenzebach’s Oliver Elbert

Oliver Elbert‘s over ten years in additive manufacturing have been spent automating LPBF. For large, high-volume, or critical parts, Grenzebach has provided custom automation solutions. Depowdering, powder handling, sieving, heat...

AMPulse Asia: Chinese IPOs, Defense Deals, and Dental 3D Printing Lead APAC Roundup

The second half of June brought a wave of additive manufacturing activity across China, Japan, South Korea, India, and Australia. From Chinese IPOs and funding rounds to defense, aerospace, construction,...

Austal, Curtin University and AMCRC Work on R&D Together

Australia’s Additive Manufacturing Cooperative Research Centre (AMCRC) works with 70 industry partners to deliver collaborative R&D projects. They also work on workforce development and technology transfer. It’s kind of analogous...