Are 3D Printing Stocks Finally Cheap?

First off I’d like to start by saying I have been an investor within the 3D printing sector for a few years now. I’ve held the majority of my shares from before the boom of 2013/14 throughout the bust, and continue to hold and add to various positions. I’m a long-term investor and seldom flip a stock as I just don’t have the time to worry about the ups and downs. Recently I began adding to my positions as I believe that some stocks within the 3D printing space are now ‘cheap.’ Below I’ll take a quick look at some of the more popular stocks within the industry and just where those companies may be headed. I own shares in a majority of the companies listed here, whether directly or within a fund.

3D Systems (NYSE:DDD) – Share Price $18.95

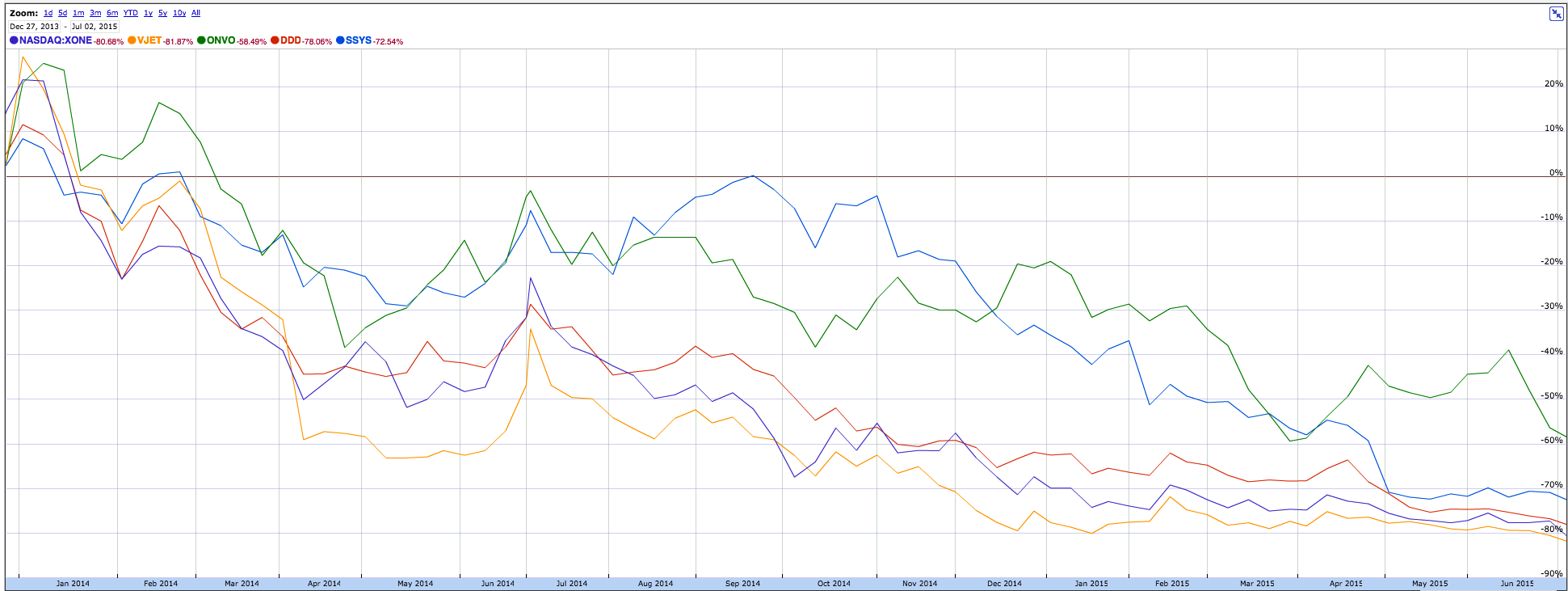

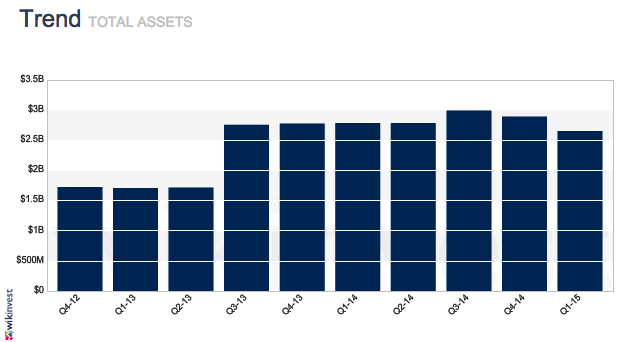

This is one of the market’s least favorite 3D printing stocks right now. With shares trading lower than they have in over two years, and off of their highs seen at the end of 2013 by over 80%, saying that this stock has been beaten down is an understatement. With a market cap just barely over $2 billion and with assets over $1.5 billion and total liabilities under $259 million as of last quarter, one certainly has to ask if shares are finally reaching a bottom.

With analysts, on average, expecting an EPS of around $0.88 in 2016 and $1.11 in 2017, future PE ratios seem to be incredibly low for a company that has the potential of growing quite rapidly over the next five years. There’s little doubt that 3D Systems has been impacted by multiple negative events. The entire 3D printing sector is down considerably, as new companies enter the market, such as HP, whose entrance is planned for the latter part of 2016. Additionally, the strength of the US dollar has caused non-US sales to drop considerably, leading to a net loss last quarter. With the company realizing revenues approaching $200 million each quarter, a $2 billion market cap seems rather cheap, especially when analysts expect profits to be realized from this quarter forward.

As the industry grows by double digits each of the next 5 years, so too should 3D Systems’ earnings. Yes, HP is a threat, but not for another 12-18 months. This has, and will continue to give 3D Systems more than enough time to develop new technologies and processes to compete with HP’s forthcoming Multi Jet Fusion technology.

Overall the company’s balance sheet is healthy, profits should begin streaming in this year, and the growth of the industry in general should equate to annual double-digital percentage profit growth over the next 5-6 years. Yes competition is a major risk; however, 3D Systems has spread their wings considerably over the last two years, meaning that if HP takes market share within one area, 3D Systems will still have growth opportunities in other areas. For now HP’s technology concentrates on polymer-based 3D printing, not metal, not food, not medical modeling, all of which 3D Systems continues to push into the market.

Stratasys (NASDAQ:SSYS) – Share Price $34.56

When looking at both DDD and SSYS it’s difficult to say which stock has been beaten down more. Stratasys, which was trading at over $136 at the end of 2013, has plummeted close to 75% since then. Trading at a market cap of $1.8 billion, which is even less than 3D Systems, Stratasys certainly seems to be cheap as well. Despite their meager market cap, as of the first quarter of 2015 the company has reported total assets of over $2.6 billion, while total liabilities are only at around $339 million. Even if Stratasys was losing money, the fact that they are a pillar within the rapidly growing 3D printing industry should equate to a market cap that’s at least equal to their total equity.

The main issue in investors’ eyes likely stems from the fact that the company saw a decrease in their EPS recently, as well as a significant drop in revenue last quarter when compared with the two prior quarters. With this said, analysts are expecting an EPS approaching $1.84 for 2016, and $2.75 by 2018. Just like with 3D Systems, however, there are market uncertainties, and while Stratasys may not be as diversified as 3D Systems, they seem to have an even stronger balance sheet, as well as a major opening to the rapidly growing consumer space with their MakerBot division.

While there have been rumors swirling that General Electric may be looking into acquiring 3D Systems, Stsratasys might make a better fit as the company is more consolidated around specific technologies rather than spread thin over numerous areas within the space. Certainly at these depressed valuations, both Stsratasys and 3D Systems could very well be acquisition targets for larger firms looking to enter the market. One has to wonder whether if these stocks were trading this low two years ago if an HP would have come in and swooped a company like Stratasys up.

Acquisition or not, Stratasys can flourish without a larger parent company. With a strong balance sheet and double-digit growth prospects for the next several years, the company is set up for long-term success. Yes, HP is a threat but just like I mentioned with 3D Systems, the company has had, and will continue to have, significant time to prepare for HP’s market entrance.

Organovo (NYSEMKT:ONVO) – Share Price $3.75

If you thought that the ride for investors of 3D Systems and Stratasys was rough, Organovo makes those stock swings appear calm. The company, which is ultimately trying to 3D print human organs, has seen its stock rise and fall quicker that SpaceX’s recent Falcon 9 cargo mission. The chaotic trading activity is nothing new to the company. Back in June of 2012 we saw shares trade at over $9.30 only to drop to a meager $1.56 a month later. In late 2013, shares rose once again to a new high of $12.50, before sliding all the way back to under $4 today.

The recent slide over the last few weeks has been spawned from the company’s latest secondary offering in which they raised an additional $40 million at a $4.25 share price. This struck a nerve with investors and provided yet another opportunity to rake in the profits. While the market didn’t love this news, in my opinion, as well as that of the company, this was a move to insure that Organovo remains a market leader within the bioprinting space. With around $90 million in cash on hand and no debt, Organovo now has a balance sheet which would make any biotech company envious.

While analysts don’t expect the company to realize a profit until sometime in 2019, the magnitude of what Organovo is trying to do certainly makes their market cap of $345 million seem appealing, especially when the company recently estimated their current planned areas of research could lead to $400+ in annual revenue in the long run.

Nothing is a certainly, especially in the biotech industry, much less the 3D printed biotech industry, but Organovo has a significant lead on the competition and has built a strong foundation for future success with partnerships with companies like L’Oréal and Merck. Any hint at a wildly successful product, either through these partnerships or their own R&D, could lead to a $1 billion+ buyout offer in the long run even if the company is not yet profitable.

Personally I have significantly added to my position in this stock over the last couple of weeks as I see this company emerging as the leader within the promising bioprinting market.

Others:

Whether it’s voxeljet, Materialise, ExOne, or the numerous other companies within the sector, they’ve all seen significant drops in their share prices. Nothing has changed within the industry over the last year. Growth projections continue to rise, with recent research indicating an expected 48.64% CAGC each year until 2019. Even if competition heats up and HP or other large corporations enter the market with a bang, the growth projections are staggering. Those  companies which have established a foothold early will benefit from their patent portfolios, management experience, and branding.

companies which have established a foothold early will benefit from their patent portfolios, management experience, and branding.

I personally believe that we have hit a bottom in most of these stocks, or are at least very close to that bottom. Of course I’m not a financial advisor or even a stock analyst, but the value inherent in many of these companies should begin to shine through over the next 12-18 months as revenues begin to rebound across the board.

Let’s hear your thoughts on the 3D printing space in general. Which stocks are you buying or selling? Discuss in the 3D Printing Stock forum thread on 3DPB.com.

Subscribe to Our Email Newsletter

Stay up-to-date on all the latest news from the 3D printing industry and receive information and offers from third party vendors.

Print Services

Upload your 3D Models and get them printed quickly and efficiently.

You May Also Like

3D Printing News Briefs, April 8, 2026: LiDAR Scanning, Vapor Smoothing, FDM Optimization, & More

We’ll kick off today’s 3D Printing News Briefs with some 3D scanning news from Artec 3D, and then move on to new America Makes Project Calls. Then, Raise3D and AMT...

3D Printing News Briefs, March 26, 2026: AMUK, IP Dispute, Asbestos, & More

We’re kicking off today’s 3D Printing News Briefs with an America Makes Project Call, and then moving on to additive manufacturing in the UK. Then we’ve got some legal news...

Everything is Connected: Cisco’s Samuel Pasquier Explains the Relevance of the IIoT Revolution to AM’s Growth Trajectory

On its own, additive manufacturing (AM) may not need a new round of record-setting investment in order to move to new heights of scalability (whether or not any investors would...

Getting Down to Business at AMS 2026: Desktop Revolution, Dental Market & More

At the recent Additive Manufacturing Strategies (AMS) 2026 in blizzard-stricken New York City, those who were able to make it through the wind and snow got right down to business....