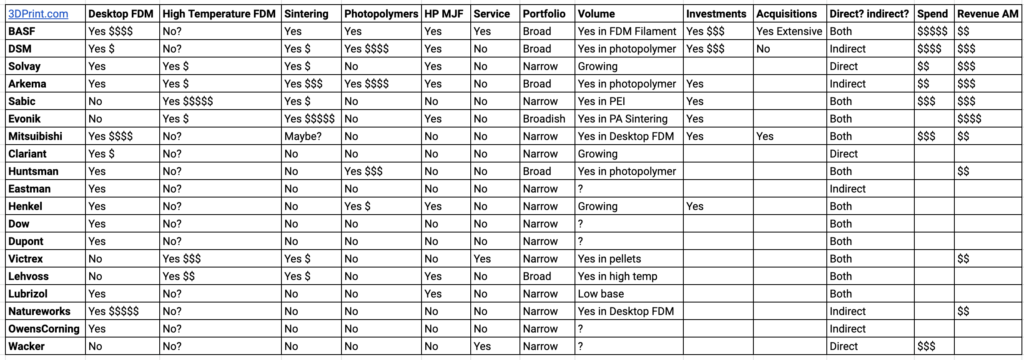

Romulus & Remus: Which Polymer Multinationals will Win in 3D Printing?

I was trying to for myself make sense of the 3D printing materials landscape, specifically what the overall positions of the large polymer companies that have entered the 3D printing market amount to. What was meant to be a succinct set of notes for myself morphed into an extended, stream of consciousness overview of the polymer giants and how they are competing with each other in 3D printing. The resulting article is more difficult to read than we’d like to use on the site and will not appeal to many people. I wanted to share it however should it be valuable to some. In a nutshell, this is the current state of the positioning of the large polymer companies duking it out to win in the 3D printing space.

The Actors

- BASF sells direct, also does a lot indirect and now also makes parts. It has photopolymers as well as FDM and focuses on the bulk side of things with some innovative applications such as metal filament. It doesn’t have PEEK but does have PPA’s.

- DSM has the full portfolio also, doesn’t sell anything directly and has no wish to make parts. Has PPA’s and no PEEK.

- Solvay sells desktop and high-temperature FDM materials directly and indirect. With PPSU, PEEK, PVDF and Carbon PEEK as its main materials.

A PEKK part being printed on a Minifactory Ultra.

- Arkema has a lot of sintering and photopolymers and high-performance PEKK. Sell indirectly through Kimya and others.

- Sabic sells direct and indirect has high-performance PEI, Extem and other high-temperature materials mainly for FDM, but does not have a broad portfolio.

- Evonik has mainly sintering materials with a leading volume in that market. It also some FDM and sells indirectly (OEM), mostly with a limited portfolio.

- Mitsubishi has a lot of bulk desktop FDM which it sells direct and indirect, mainly through retail and OEMs.

- Clariant sells directly fr and other additives enhanced materials for desktop FDM.

- Hunstman now has FDM as well as photopolymers.

- Eastman has bulk and premium desktop FDM materials but no high temperature.

- Henkel has photopolymers some other materials as well and things like post-processing which it is selling directly and through OEMs.

- Dow and DuPont have a limited number of materials and no volume.

- Victrex is only PEEK (and other PAEK family) and does direct and parts and through select OEMs but is fat and happy.

- Lehvoss has shown a capacity to innovate and punch above its weight in sintering and FDM, the same goes for Kimya.

- Lubrizol needs its TPU to do well in footwear on the HP machines and perhaps on more platforms too.

- Natureworks has become the gold standard of PLA and so far have not been disrupted by other PLA producers or other producers of bioplastics.

- OwnensCorning entered the market with some GF loaded materials that were very exactly what the market wanted but seems to have little traction?

- Covestro has FDM materials but it is unclear what its commitment to the market is.

A nightmare to print with PEEK has desired properties.

Ther Positioning

- Victrex will move into medical device manufacturing in polymers and sell parts, becoming a niche high margin player? Meanwhile, will Aceo (Wacker) do the same play for silicone?

- Dow and DuPont will sit together eating popcorn while everyone else fights over this market? Dow needs the Viscotec (Ecco, German RepRap) implementation of silicone to work well for it to succeed. Chances of this seem slim at the moment. Lubrizol also needs a big win on much-expanded use of TPU to win although it has shown real innovation through Colorfabb Varioshore and other innovations. Without shoes on feet, it will have no volume, however. OwensCorning as well needs volume in order to play a role in 3D printing’s future.

- In terms of positioning and portfolio, Solvay is most like Sabic with their joint focus on high-temperature high-performance FDM through direct sales and sales through OEMs. At different points of the portfolio, one could pick a Solvay material over a Sabic one depending on chemical resistance to one material (eg jet fuel) another quality, requirement or price.

- Interestingly in my mind, they are both in one of the most profitable and potentially high growth segments of 3D printing at the moment along with GF and CF filled PA grades for FDM in manufacturing which many are doing already.

- In a bit, Solvay and Sabic will probably be joined by another complimentary offering from Arkema. Solvay and Sabic mirror each other often but Arkema is the one to watch given their new investments in PEKK and their volume in photopolymers and sintering. With more cash, Arkema could even take the crown from BASF or DSM.

- A newer entrant with less overall volume than Arkema and Sabic; Solvay needs to fight hard through new chemistry, product introductions or growth (albeit with less of an outlay and overhead).

- Sabic meanwhile has a long track record and has invested considerably in 3D printing but has a limited portfolio. It must maintain PEI’s dominance over aerospace, fend of PEEK’s popularity and win in large format which is a focus (alone with DSM!) If it does this it can gain in volume and see good irr’s on the money invested.

- Arkema has been around quite a while and needs to gain in brand, distribution, sintering and FDM volume while maintaining its photopolymers. By broadening its portfolio and perhaps doing FDM it could get broader volumes or it could opt for a specific high-profit approach or up its game and be a general player like DSM and BASF.

Good old PA2200

- Evonik has probably extracted more money from 3D printing materials than anyone while investing comparably little(except if you count Stratasys, EOS or 3D Systems). The company will need to defend its sintering bastion with new materials and expand in high-temperature FDM to keep this from eating its market. Since sintering PEEK doesn’t work at the moment (0% recycling rate), any gains in high-performance sintering materials may shore them up. Meanwhile, everyone is chipping away at Evonik PA in sintering. Unless Evonik has different accounting or optimism, it should have deep reservoirs of untapped money earmarked for 3D printing, perhaps to invest during the downturn? Should it lock itself in with EOS or does it more than others have more to gain from anyone but EOS winning in market share?

- Huntsman needs to move from an only photopolymer strategy (which it has started doing) and prove that it can keep up with the high-performance chops that others are showcasing in photopolymer (Sartomer, Somos and Henkel all seem innovative) and maintain in volume from renewed assaults from DSM and Arkema.

Parts printed by Orign’s technology using Henkel resin.

- Henkel has a bit of an esoteric market entry in that it is playing to its photo strengths but using a consumer brand to do so as well as releasing other products. Beneath the bodywarmers however, is fundamentally interesting work on the Carbon materials. Henkel can pick and choose its battles which is powerful, but it is insular compared to others.

- Mitsubishi has invested in buying volume in filaments but it is unclear what it wants to and can do now? It is interesting that Mitsubishi could form a formidable complementary alliance with either Arkema, Sabic or Solvay but that’s not very likely. The BFF scenario or we could call it the ABB scenario (Anyone But BASF). Arkema Mitsubishi, in particular, would be an especially powerful complementary tie-up with incredible reach and cross-sell potential.

- Eastman was way ahead of the pack, especially in desktop FDM, but has seemed disinterested in 3D printing of late.

- Speaking of disinterested, much desktop FDM volume is still Natureworks PLA and the firm has indeed made a few specific grades but seems either glacially patient or uninterested in upsetting the way of things.

- DSM has invested significant amounts of money in its own organizational capacity and in investments. The organization is the biggest at DSM and the company seems to want to be all things to all men. One-stop-shop could work especially if their industry-specific expert approach remains uncopied. It does tie them to high expectations at board level and an elevated cost structure when compared to other firms.

- BASF’s Ultrafuse 316L metal filament

- BASF has probably invested more than anyone in being all things to all polymers. Whereas DSM has more market knowledge, contact and application-specific materials; BASF seems to make its products in a closed lab with no contact with the world.

- If the Sculpteo move lets them enter the high growth spheres of parts manufacturing with their own materials and machines from companies that they’ve invested in, BASF could have an almost vertically integrated 3D printing offering. Will this alienate other players in the market or not? This we do not know yet. It could very well be punished for this by OEMs and other services. To me, it seems like BASF has focused its risks through the Sculpteo opportunity. Rather than diversifying and being more granular in its contact with the market (as DSM and Arkema are doing), it is centralizing its risk in fewer go to market routes that are in the hands of fewer people. On the one hand, the economics of making and selling parts are of course great; with a much higher margin than just selling resin or even filament. Crucially service businesses look amazing through the lens of net contribution margin but eat capital. If Sculpteo grows like gangbusters, BASF will do very well. Indeed the financial picture will almost ensure that a disproportionate amount of capital will be directed at Sculpteo out of all of the allocation choices BASF has at the moment. A small number of people at the Sculpteo unit could, therefore, determine the future of BASF’s effort in 3D. At the same time, OEM partnerships with GKN, Shapeways, Xometry by other materials companies have now become more likely; perhaps freezing out BASF from other paths to success. BASF may think that it has bought a path to market (or captive volume) but it has committed itself to this one highway and killed off other possible routes. Tactically I think that this is an error. Compare this to a more granular approach where Arkema could buy 10% of a half a dozen services, through this move obtain enough influence to promote its material and develop it with customers, while not being perceived as a threat. Strategically BASF’s move may pay off though if they execute perfectly, however. What were seeing here is that different accounting and internal KPI’s are really influencing how firms deploy their money in our market. Paradoxically KPI’s seem to trump strategy.

- A hyper-aggressive non-EOS non-3D Systems aligned polymer company with no sintering volume could through acquiring (or investing) in a sintering OEM and a 3D printing service, push ultra-low-cost sintering powder and parts that would displace EOS/3DSystems/Evonik/Arkema volume. Retail on sintering powders is $95 while for some high volume users one could be paying $25 a kilo depending on the grade. Limited cryogenic grinding expertise is holding back lowering prices even further but it could be an option for a company to go in even lower with powder pricing. Alternatively, a nonpowder or not as critical powder morphology technology could also be used to do this. This by far be the most destructive market dominance path I can fathom at the moment but for pennies on the pound, you could be pushing these guys out of the market. It is the strategy I would recommend. If this is what BASF will do with Sculpteo then they have a strong chance of dominating the 3D printing market. If not then it gives breathing room for everyone else.

- In photopolymers, a similar play by someone willing to sell at $30 a liter rather than $800 or $150 could also torpedo everyone else. It would be a smart move but its hard to see someone wipe the tears from their spreadsheets long enough to pull the trigger on this.

- If the above doesn’t occur then I would imagine BASF and DSM to become somewhat of a duopoly in 3D printing because of their extensive portfolios, customer and application overlap, and economies of scale. I’d expect DSM’s application and expertise on staff approach to extract more value in the long run and therefore would expect, all things staying equal, DSM ultimately to win.

- Another company that pulls either one of two hyper-aggressive stunts above could win as well. In that scenario, all other players would stay within their niches and be profitable as well but they would not be destined to become market dominant.

- There are a number of wildcards though. If Kimya, Lehvoss, and Clariant continue on their path of making application-specific materials to order; investments in sales could see these companies find and capture hugely profitable niches unknown to others. There could be millions of kilos of specific material needed in a niche construction application for example, that nonetheless would eclipse a lot of known value in the rest of the market. This could incubate growth later on.

- Sabic’s involvement with Thermwood, Cincinnati and others could see them develop a large volume and medium format lead that could see them do significantly more volume than others. One successful large-format implementation equals hundreds of thousands of desktop printers or dozens of SLS machines in materials volume.

- All in all, however, it looks as if we’ll have two dominant firms, BASF and DSM. Shall we call them Romulus and Remus? Then we have a trio of high-temperature and more players: SABIC, Arkema, and Solvay. The triplets. Then we have the specific materials companies: Clariant, Lehvoss, Kimya, and Lubrizol (the quartet) and the services Wacker and Victrex. Then there’s the specialists: Evonik, Natureworks, Huntsman, Mitsubishi and Henkel (quintet) and everyone else is fucked.

Subscribe to Our Email Newsletter

Stay up-to-date on all the latest news from the 3D printing industry and receive information and offers from third party vendors.

Print Services

Upload your 3D Models and get them printed quickly and efficiently.

You May Also Like

Does the Fed Rate Cut Mean Anything for Manufacturers?

About a year ago, the Federal Reserve issued the “jumbo” rate cut, reducing interest rates for the first time since hiking them to their highest levels in decades, a process...

MacLean-Fogg & Fraunhofer ILT Make 156 Kg 3D Printed Toyota Tooling Insert

Fastener & tooling firm MacLean-Fogg Company and Fraunhofer ILT have created a 156 kg conformally cooled die casting insert, made out of the firm’s own L-40 tool steel powder. This...

3DPOD 272: Kevin Kassekert, VulcanForms CEO

Kevin Kassekert has deep experience building factories for Tesla and has worked in the semiconductor industry. He now helms VulcanForms and is looking to scale their high-yield Laser Powder Bed...

3D Printing News Briefs, September 20, 2025: Standards, Floor Slabs, Wastewater Treatment, & More

In this weekend’s 3D Printing News Briefs, we’ll start with standards news from ASTM. Then, we’ll move on to a new 3D printable alloy from QuesTek Innovations, and Autodesk Research...