The Stifel North Atlantic AM-Forward Fund, initiated as a part of the AM Forward program established under the Biden Administration, has announced that it has poured $10 million into Florida-based service provider Sintavia. The money “will be used to refinance existing equipment loans and provide general working capital for the business” and continue Sintavia´s $25 million expansion.

“We are honored and humbled to be the launch investment out of the new Stifel North Atlantic AM-Forward Fund. It is great to see Stifel’s strong commitment to funding profitable, high-growth users of additive technology, and this new fund will certainly have a positive impact across the industry,” said Sintavia CEO Brian R. Neff.

“Sintavia is a fantastic fit for the mission of our Fund and Brian has proven to be a visionary leader for Sintavia, and the additive manufacturing sector more broadly. The entire Sintavia team has done a terrific job since 2015 in building a vertically integrated, all-digital aerospace component supplier that leverages the positive benefits of additive technology, and we look forward to working with Brian in the coming years as a partner,” said Mark Morrissette, Managing Director of Stifel Subsidiary North Atlantic Capital.

Sintatvia has been involved in additive manufacturing (AM) since 2012. The NADCAP- and ISO 9100-accredited, ITAR-registered firm initially served defense and aerospace clients. Now, it specializes in heat exchange and pump systems for aerospace primes and defense firms. The company operates SLM and EOS 3D printers, has in-house HIP, CNC, and EDM capabilities, and focuses on the most demanding parts for the toughest applications. Alongside ADDMAN, Burloak, i3D MFG, Mimo Technik, Incodema, and a select few others, Sintavia is among the firms capable of producing parts for Boeing, Lockheed, Northrop, the satellite industry, new space firms, and submarines.

Given the expected growth in these segments, this is a strong position to be in at the moment. It’s also quite defensible, as manufacturing the toughest parts is inherently challenging. Significant capital investment is required to reach and maintain the cutting edge. ADDMAN, for instance, benefits from the backing of private equity giant American Industrial Partners (AIP). Burloak is owned by Samuel, a metal parts conglomerate with over $1.5 billion in revenue. i3D is part of BTX Precision, a company founded by L Squared Capital to consolidate the fragmented precision manufacturing market in the U.S.—a strategy similar to what AIP and CORE Industrial Partners are pursuing. For those without deep capital reserves, the past year may have been a cause for concern.

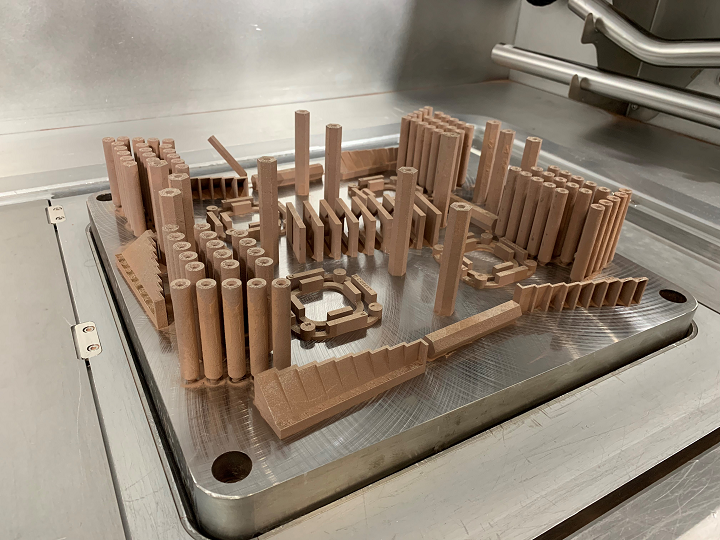

Copper parts 3D printed by Sintavia.

SPAC-backed firms have melted like ice cubes, stock performance has been generally poor, and VCs are busy reading Artificial Intelligence for Dummies to lose someone else’s shirt all over again. Enter the Stifel North Atlantic AM-Forward Fund. This fund was established to provide capital to Tier 2 through 4 defense and aerospace suppliers while supporting their expansion. By increasing their work with Primes—Tier 1 suppliers like Lockheed that design and assemble components from Tier 2 into finished vehicles—these companies can help sustain a competitive, thriving industrial base capable of supporting the U.S. military through future challenges. At the same time, they can drive high-tolerance manufacturing into emerging industries such as energy and, perhaps, jetpacks.

It’s a highly logical move, aligning with the strategies pursued by other private equity firms. The fund combines Stifel’s deal-making and financial expertise with the U.S. government’s SBIC CT program (SBA and DOD critical technology), along with investors and Astro America. Astro, of course, is the relentless advocate for hypersonics, Guam, and jointless hulls, positioning itself as the connective tissue for the deals on the horizon.

If you were at Additive Manufacturing Strategies, all of these key players were represented—underscoring just how crucial this kind of capital gathering is for our industry and for the U.S. Across America, people founded complex, high-precision businesses decades ago. These firms, built on long-term contracts and deep relationships, are dwindling in number despite many continuing to thrive in any business climate. Unlike hipster hamburgers or bubble tea, very few people possess the skills to do what they do, making them natural targets for private equity firms.

At the same time, what other options do these companies have? Who could facilitate management buyouts? What firms are out there for them to join? Now, introduce a breakthrough technology—3D printing—that offers increased automation and higher-performance parts, and everything starts to fall into place.

Mark Morrissette will join Sintavia’s board, making this a solid investment for the company. While it may introduce some oversight, Sintavia retains its independence. Brian isn’t looking to retire on a beach—he wants to keep making waves with his firm. A former private equity investor himself, he used his fund, Neff Capital Management, to acquire engine MRO firm CTS Engines before selling it and spinning out Sintavia.

This is also a net positive for the industry, as it highlights an alternative to selling a firm outright. The fund’s capital comes from investors and Tier 1 firms, and with Lockheed having already invested in Sintavia in mid-2023, this serves as another strong vote of confidence. The mention of refinancing equipment and working capital as destinations for the funds is slightly concerning, but rather than seeing this as a lifeline, it’s better viewed as a jump rope—fueling momentum rather than survival.

Sintavia is positioned to secure major opportunities in high-value parts, systems, and programs, potentially driving significant growth. At the same time, it remains a highly attractive takeover target for private equity firms, while expanding its reach into part numbers that smaller shops simply cannot accommodate. A solid move.

The fund is sure to find other opportunities to support and grow many industrial base firms. Its work could prove both highly lucrative and strategically important for the U.S. The country’s industrial base has been in decline for decades, weakened by waves of outsourcing, a shift toward service businesses, and later, a fixation on software—all contributing to the erosion of U.S. manufacturing. It used to be barbarians at the gate—now, the Romans are lightweight.