The additive manufacturing (AM) industry is on the cusp of some momentous merger activity coming to fruition. We do not know what will happen yet, but the consequences will be far-reaching. If the mergers do happen, we will either get a new owner for Stratasys in the form of the cash-rich but smaller Nano Dimension, see a behemoth tie-up of 3D Systems (NYSE: DDD) and Stratasys (Nasdaq: SSYS) or see Desktop Metal (NYSE: DM) join with Stratasys. If none of the proposed mergers or acquisitions go through, investors will redouble their scrutiny of the major 3D printing stocks. People will pay much closer attention to strategies, performance, assumptions and the path forward.

I interviewed consultant John Barnes, Founder and President of the Barnes Global Advisors, to find out more on his take on the M&A activity in our market. Barnes is focused on the human element of the sector.

“I think we should look at the humanity of the situation,” Barnes said. “When people talk about synergy, what they often mean is job loss. We have to consider this as well, we have to think about just how empty a term ‘synergy’ is. We have to keep AM human. And we are talking about integrating large companies. This integration process is always difficult. If cultures are too dissimilar then the integration will be terrible. Mergers often fail because of culture or if integration takes too long. Where is the customer value? So far, different people need different machines in different departments, so the one global partner argument may not actually be something people want. Goodwill will eventually need to be earned or accounted for, for that to work out properly the growth and value does have to be there.”

Right now, we have a duopoly buttressed by a much bigger share for smaller, privately held players, but if the merger takes place, we may end up with one giant firm that can muscle others aside. I have my misgivings about these mergers because I don´t believe that they will deliver value for shareholders or the industry as a whole. I don´t see how any of these moves will make 3D printers or the 3D printing experience better. Barnes has his own misgivings, as well.

“Where is the value being created or where can costs be lowered? Can we do things like better utilize equipment, get economies of scale, reduce equipment costs, consolidate assembly lines? Are the fundamental financials of these deals sound? People often overlook access to the market, the right to sell. There is also a fair amount of good will here. It also seems that Stratasys is betting on a lot of growth in binder jetting which eventually may hold true but this will take years to mature.”

Barnes reflected on other possibilities for a potential merger, as well, including options that would result in a more complex and nuanced business entity.

“On the more positive side it could create a much more visible AM company or could lead to creative destruction which after some pain would lead to growth,” Barnes said. “Also did anyone ask for a pure play 3D printing company that is made up of these firms? Wouldn’t a deal with a legacy manufacturer make more sense? A company like DMG, Haas, Mazak could create a lot of value here. They have long relationships with almost all of the clients the 3D printing firms would want to have. Get an UltiMaker with your Haas.”

Barnes and I agreed completely on that point. Imagine a deal where DMG Mori, Haas, or Mazak would buy Markforged, Formlabs and/or UltiMaker? It could easily place a 3D printer at thousands of customers for the production of tooling, manufacturing aids, and prototypes. Wouldn’t that product extension add much more value at less of an outlay, depending on the choice? For example, DMG has over 100,000 customers.

Barnes also asked “where is the growth?” This triggered me to reflect a lot on the topic. At Stratasys, the firm’s full-year revenue for 2022 was “651.5 million, 7.3% higher versus 2021 and up 11.4% at constant currency and adjusted for divestitures.” 3D Systems’ was 12% lower for 2022 than 2021. At both companies, revenue is currently about the same as it was in 2014. Desktop Metal’s revenue has increased significantly, by as much as 82% percent. However, the firm spent around $441 million of its cash to get it. It has around $134 million cash left and, last year, had a net loss of $312 million. Meanwhile, our market is growing by around 15% to 30% per year.

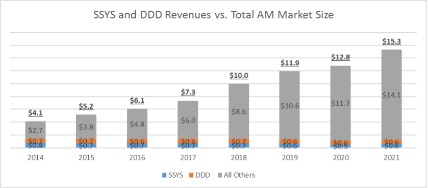

If we look at the publicly-traded firms, it’s almost as if there is a lost decade in 3D printing. However, over the same period (since 2014), our market has grown from around $3 billion in revenue to $13.5 billion. The pie is much larger, but the big public firms seem to capture a pie slice of about the same size. Amid growth, there is stasis, while other smaller firms are capturing and creating that expansion. This is well-illustrated by Tali Rosman in her report for SmarTech Analysis, titled “Emerging AM Technologies Analysis: 10 Companies to Watch.”

From the SmarTech Analysis report “Emerging AM Technologies Analysis: 10 Companies to Watch.”

If we only look at revenue and market growth, the large firms seem to be losing out on the big gains. That would spell worry for Barnes’s lament to keep AM human, because then it could mean that this merger talk is only about numbers, not people. It could mean that a desire for more revenues, rather than innovation and value, is driving this merger activity.