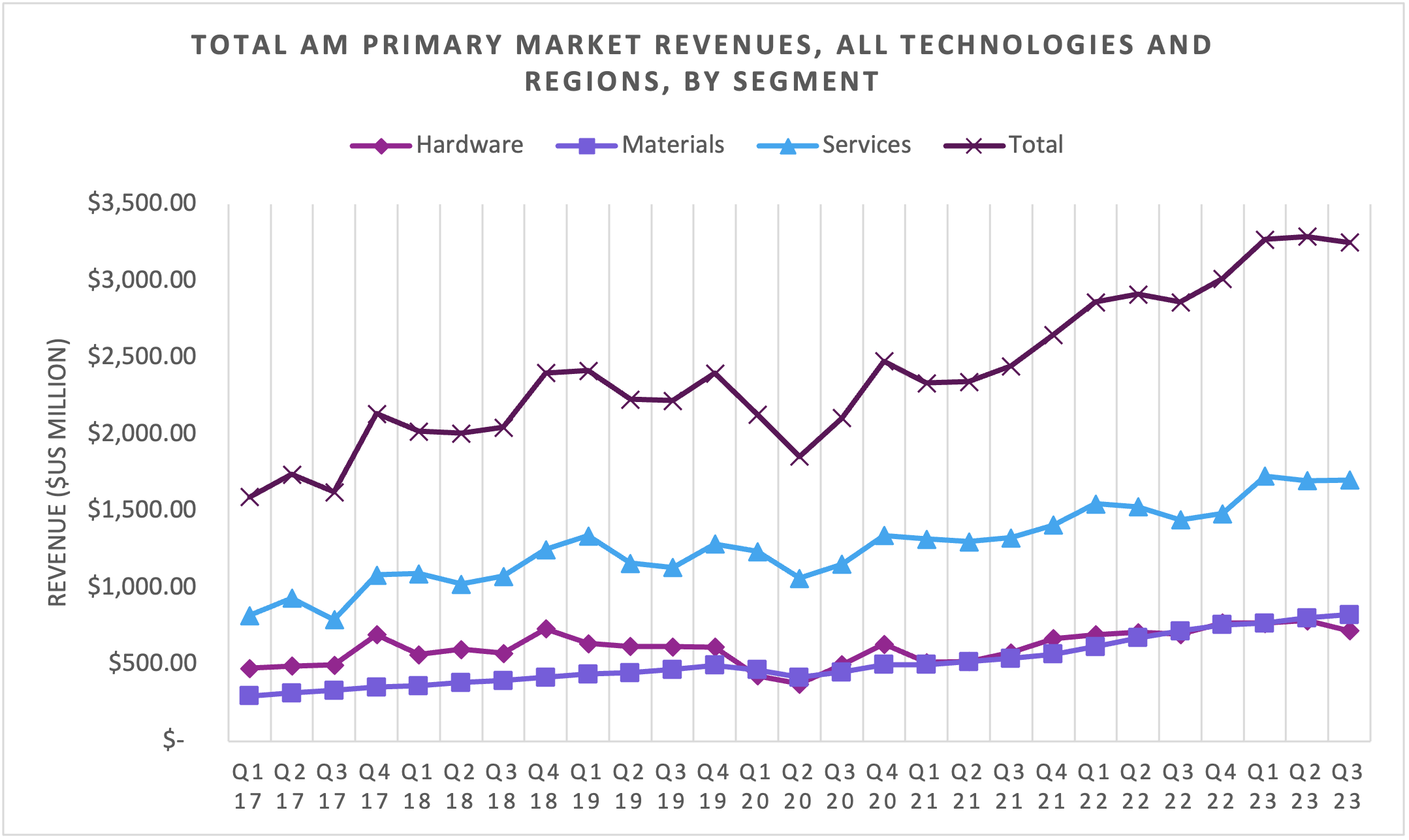

The additive manufacturing (AM) market has hit a plateau in Q3 2023, with a 1% estimated sequential decline from Q2 2023, according to the latest report from Additive Manufacturing Research (AMR). Despite the quarter-over-quarter dip, the sector has still achieved a 13% growth compared to the same quarter last year. This assessment covers all segments of the market, including hardware, materials, and services for both polymer and metal AM.

For nearly ten years, AMR has been the authoritative source for quarterly 3D printing market data, providing detailed industry insights. The recent figures reflect broader economic challenges, such as rising capital costs, which have particularly affected hardware sales. In contrast, material sales have fared better, showing continued health in this segment.

Scott Dunham, Executive Vice President of AMR, commented, “The impacts of the macro environment and higher costs of capital are being seen in AM market numbers, mainly in hardware sales, while materials sales remain healthy. Demand for print services in the quarter were mixed, as companies still struggle to deal with supply chain problems, but shorter backlogs have reduced the opportunity costs of not acting to put in place new solutions such as AM. Additionally, product development spending appears to be down, which impacts AM services. We expect some market softness to continue through 2024 due to interest rates, and growth in AM during this time to be driven by existing influential users who continue to scale up their activities.”

The report includes comprehensive data from leading companies in the AM space, such as 3D Systems (NYSE: DDD), Stratasys (Nasdaq: SSYS), HP (NYSE: HPQ), Markforged (NYSE: MKFG), Desktop Metal (NYSE: DM), Velo3D (NYSE: VLD), Nikon SLM Solutions, EOS, GE Additive, Trumpf, Farsoon, BLT, HBD, Eplus, Optomec, Formlabs, Prodways, DWS, and Carbon. These firms, among others, contribute to the robust tracking data in AMR’s Core Metals and Core Polymers reports, which provide a decade of historical data and ten-year forecasts.

Key findings from the report indicate that metal AM hardware sales saw an 8% decrease compared to the previous quarter—the first such decline in a Q3 period since AMR began its tracking. Year-over-year, however, there is a nearly 7% growth. Polymer AM hardware sales also dropped by 8% from Q2, with only a 1% year-over-year increase. Nonetheless, the polymer AM materials segment has helped keep the overall polymer market stable. The report suggests a cautious optimism for Q4 2023, with the potential for slight improvements. These trends underscore the current climate of innovation tempered by economic restraint, where the AM industry continues to adapt and push forward.

For further insights and detailed forecasts, AMR’s market data products are available for purchase, providing invaluable analysis for stakeholders in the additive manufacturing sector. Interested parties can obtain more information on these reports and subscription services at the AMR website.