Though it doesn’t make it into the top 10 institutional investors backing 3D printing stocks, Goldman Sachs may still be an influential force in the burgeoning additive manufacturing (AM) industry. At the moment the historically powerful bank is serving as the financial advisor to the sector’s oldest firm, 3D Systems (NYSE: DDD), as it attempts to purchase its long-time competitor, Stratasys (Nasdaq: SSYS). This raises the question of what other role the company plays in 3D printing at large.

3D Printing Stock Coverage

Goldman Sachs has been reporting on 3D printing stocks dating back to at least 2014, right at the peak of the sector’s bubble. In April 2014, its analyst Samuel Eisner recommended a buy of Stratasys with a price target of $146, several months after the stock’s historical high of $136.46 in January 2014. Whereas it was neutral toward 3D Systems at $63, which hit its high of $96.04 that past January. The Stratasys guidance would have been a risky bet, given the general consensus that AM companies were considered extremely overvalued at that time, with very high P/E ratios.

3D Printing Stock Ownership

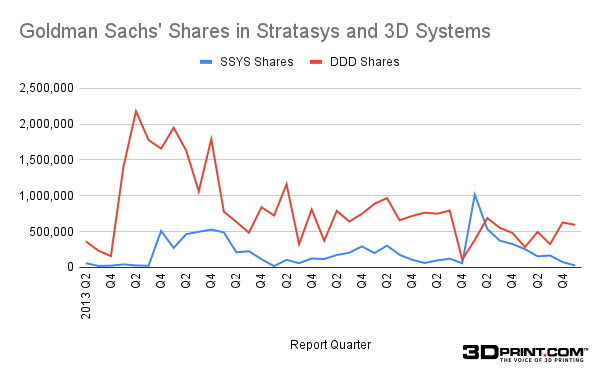

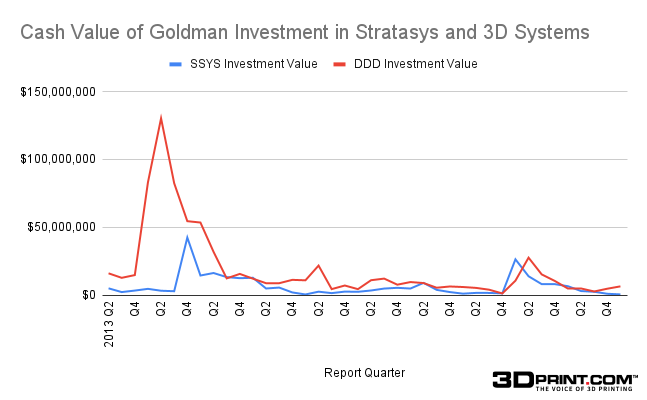

While it initiated coverage in Q2 2014, the bank began purchasing 3D printing stocks and options at least as far back as Q2 2013, when it began acquiring interest in 3D Systems and Stratasys. The bank’s investment in Stratasys began to drop beginning around March 2021, while its stock in 3D Systems has remained below 1 million shares since about Q3 2017. Goldman’s interest in companies like these has, at times, represented hundreds of millions of dollars in a year, yet they still only represent a blip in its overall portfolio at less than one-tenth of a percent. Below are two charts depicting the bank’s investment into those two firms represented in terms of shares and cash value.

3D Systems’ Financial Advisor

When the last big consolidation trend occurred in the AM industry in 2015, as GE acquired Concept Laser and Arcam, it was rumored that 3D Systems had taken on Goldman Sachs as an advisor in a possible bid to be purchased by the manufacturing giant.

Now, mergers are heating up again and, this time, Goldman Sachs is officially serving as a financial advisor for 3D Systems in its bid to acquire Stratasys. Because the merger has far-reaching implications for the 3D printing industry and the manufacturing sector beyond, this is no small role for the bank to take. One of the world’s most historically important financial institutions is assisting the industry’s oldest AM firm in what is a crucial merger for the future of digital production.

Interestingly, according to an article by 3D Printing Industry (3DPI), Goldman Sachs may have reached out to a new institutional investor of Stratasys, the Donerail Group, for a private meeting. As we reported, Donerail issued a complaint against Stratasys, The 3DPI story notes:

According to a person familiar with the parties involved, Donerail was invited to meet with Goldman Sachs, the 3D Systems advisor. This meeting request is considered unusual, as it happens only once a year or two. According to the source, this signifies an interest in stirring things up. Donerail, a self-described “value-oriented, activist” investor, had previously taken a position in Turtle Beach, a gaming accessory manufacturer.

The article doesn’t go into further detail about that position in Turtle Beach, but as our coverage notes, it was an activist role that saw much of the Board replaced. The company’s CEO has also just stepped down, while Donerail’s own Chief Investment Officer, William Wyatt, has joined the Board. Though Donerail has not been involved in much else publicly aside from the Turtle Beach takeover, Wyatt actually got his start as an analyst and associate in investment banking at Goldman Sachs.

Backing Fast Radius

When 3D printing service bureau Fast Radius became publicly listed through a merger with a special purpose acquisition company, Goldman Sachs was a part of a $25 million purchase commitment alongside UPS and Palantir. When the company went bankrupt less than a year later, a New York-based private equity firm run by a former Goldman Sachs partner, Barry Volpert, purchased Fast Radius and as a part of a digital manufacturing provider roll-up.

Somewhat parallel to that, there is American Industrial Partners (AIP), another private equity company that is engaged in a service bureau roll up, headed by General Partner Kim Marvin, who served in the Mergers and Acquisitions and Financial Institutions Groups at Goldman Sachs.

Divergent Board

Though people like William Wyatt, Barry Volpert and Kim Marvin may not be formally connected to their legacy firms, they may still be connected through informal social networks. That would bear some significance on the fact that John L. Thornton, former president of Goldman Sachs, joined the Board of Directors at Divergent in 2022. It may have been that Divergent’s CEO, Kevin Czinger, knew Thornton from his days as executive director and head of the media-banking group at Goldman Sachs International in the early 1990s.

Macro Take

All of the individual details coalesce to emphasize a simple and powerful lesson that is currently revealing itself to the AM sector at-large: relationships with financial institutions matter. This will be important to keep in mind as opportunities for government contracts become both evermore plentiful and evermore complex/confusing. It is difficult to envision a company having the confidence to go all in on trying to get CHIPS money, for instance, without that effort being backed by a hefty consulting budget.

Of course, though, as all of the preceding facts make clear, shepherding by financial institutions is currently most significant in the context of corporate consolidation. Along those lines, it is obvious why the consolidation process should, at least initially, be most beneficial to the companies that already dominate the share of AM investment dollars.

It is more interesting to consider why an institution like Goldman Sachs would have an interest in the sector’s consolidation. While very few entities at present seem to have a stellar publicly verifiable track record in terms of predicting the trajectory of macroeconomic conditions, one would still have to admit that Goldman Sachs is what’s known as “smart money.” If Goldman is attaching itself publicly to AM mergers and acquisitions this early on in the process, then it is not just trying to help one company solve a problem. It is trying to send a message to the market.

In fact, one can read multiple, related messages into Goldman’s actions: (1) AM is not only “real,” it’s real right now. In turn, (2) the AM market is consolidating in order to scale up, which could also simultaneously mean that (3) a bottom in the AM market has been or is about to be reached. More bluntly, the overarching message is, “We, a powerful and influential institution, take seriously that there is an immediately realistic business case for this assortment of overlapping emerging technologies.” In this case, it might be fruitful to consider what legacy sectors Goldman has the most exposure to, in order to help gauge the markets that AM has the most long-term potential in.