Those of us following additive manufacturing (AM) news have little doubt that the technology is growing rapidly, but the latest report from SmarTech Analysis can anchor that confidence in hard data. According to the leading industry analysis and market forecasting provider, the polymer 3D printing industry will generate $11.7 billion in revenues in 2020. The company further projects that the sector will reach $24 billion in 2024 and as much as $55 billion by the end of the decade.

The data is included in SmarTech’s fourth annual market study on Polymer Additive Manufacturing Markets, which analyzes the dynamics of the polymer AM sector during the period from 2020 to 2029. It also includes, for the first time, an extensive analysis of revenues associated with 3D-printed parts.

A review of the report’s table of contents suggests broad coverage of the industry, as it includes established and emerging polymer AM technologies, companies, and materials across a variety of verticals. For instance, the entire gamut of powder bed fusion (PBF) technologies is discussed, from low-cost to high-throughput technologies and even novel vat polymerization processes, such as volumetric 3D printing, are analyzed. And that’s just within the hardware chapter of the report.

The other four chapters explore opportunities related to polymer materials, such as amorphous and semicrystalline thermoplastics, as well as the dynamics of industrial sectors (including aerospace, healthcare, consumer goods and automotive) and the types of parts that are now being produced serially.

According to SmarTech, some of the trends that are driving the evolution of polymer AM are the automation and optimization of the polymer 3D printing workflow, in addition to the improvement of materials for AM technology. We are certainly seeing companies like Carbon and 3D Systems attempt to deploy automation techniques for vat photopolymerization, with those same layerless digital light processing technologies utilizing new material chemistries to introduce new physical properties to the AM market. Meanwhile, startups like Origin are attempting to improve upon these processes by opening up an even greater array of materials.

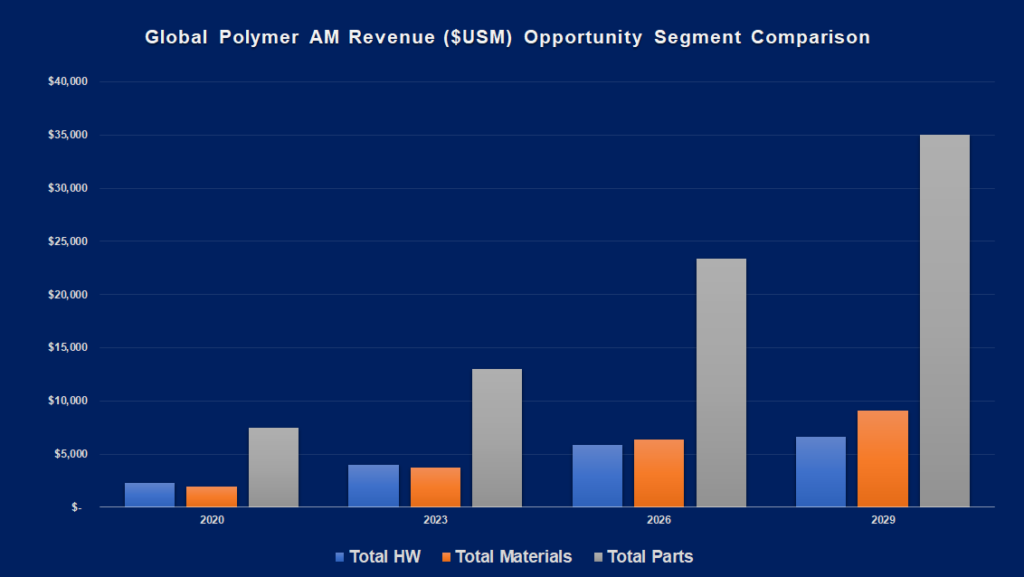

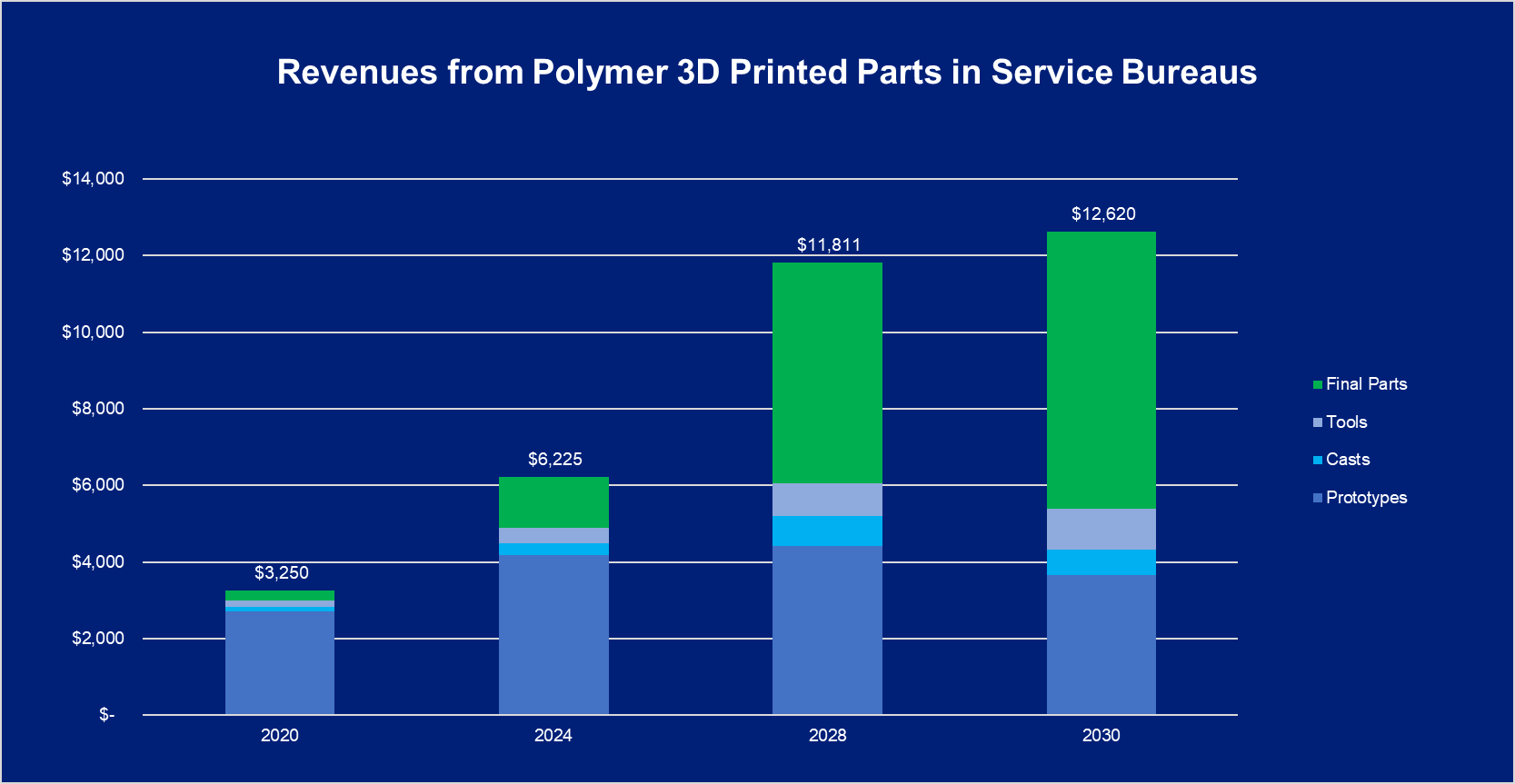

This report utilizes a new model developed by SmarTech in which multiple variables, such as average part weight and cost, and data collected via research from additional reports on vertical segments (e.g., automotive, aerospace, etc.) are combined to determine the revenues of 3D-printed parts. This includes everything from prototypes to molds/casts, tools and end parts. As SmarTech puts it in a press release on the subject, “[p]arts are calculated as a complex function of material consumption and are subdivided into vertical adoption segments.” With this new model, the company was able to anticipate the overall revenue to be generated from 3D-printed polymer parts, projecting a $40 billion opportunity by 2030.

According to the market research firm, the aerospace and automotive industries are the two most relevant segments for long-term polymer 3D printing and, by 2030, significant part production will occur in these two segments. The transition to the direct 3D printing of consumer products will take more time, but SmarTech projects that it will represent a large segment. For jewelry, this will mainly mean continued use of polymer AM for printing molds and patterns.

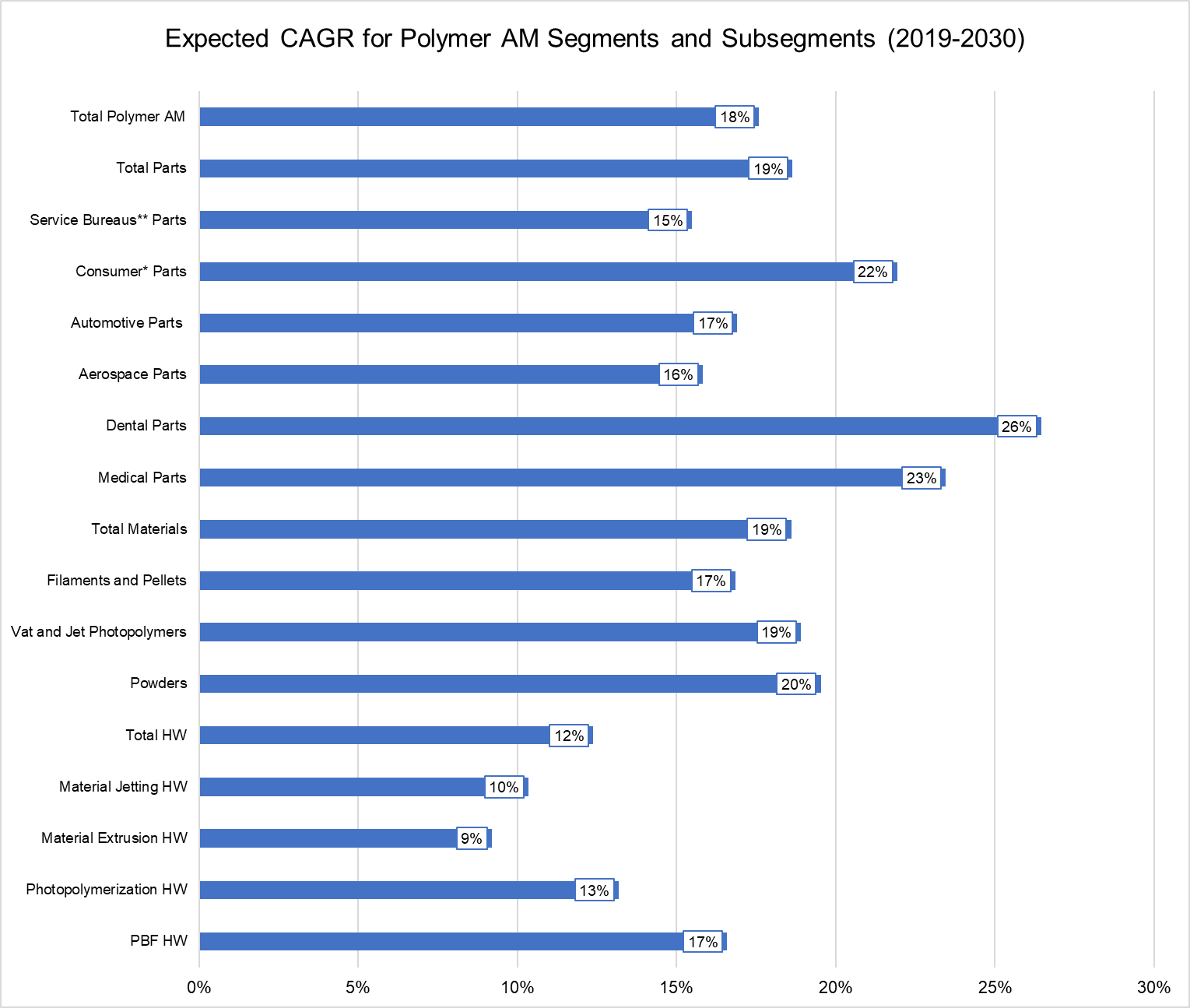

On the report page, SmarTech lists a handful of figures and insights from the report. Though stereolithography followed by material extrusion were the primary polymer technologies in previous editions of this report, polymer PBF is now emerging as the reference polymer process for its high throughput and the mechanical properties of parts made by PBF.

Similarly, thermoplastic PBF processes are now being considered the main segment for material consumption, due to their ability to perform large batch production. In turn, powder material, especially nylon 12, are the largest material segment. There’s no doubt that the rapid spread of HP’s Multi Jet Fusion is a key factor in this development, but laser-based systems account for this dynamic as well.

SmarTech determined that material extrusion generated the highest revenue globally for polymer AM in 2019 by a large degree, but projects that the industrialization of vat photopolymerization and PBF will cause material extrusion to be surpassed by these two latter technologies in terms of revenue generation by the end of the forecast period.

The market analysis firm has now determined that indirect and direct part manufacturing represents the best value proposition for the sector, signifying a real shift in AM overall compared to earlier days of rapid prototyping. To read more about the report, visit the SmarTech Analysis website.

3DPrint.com has an equity stake in SmarTech.